The State of Private Equity in 2020

The state of global private equity in 2020 is complex, mainly due to economic activity drastically contracting since the second quarter. Many businesses are on the brink of collapse. In these extraordinary times, what are the main challenges that private equity funds face?

The state of global private equity in 2020 is complex, mainly due to economic activity drastically contracting since the second quarter. Many businesses are on the brink of collapse. In these extraordinary times, what are the main challenges that private equity funds face?

Natasha transitioned to venture capital after a career in banking built in prestigious firms such as JPMorgan and ESM.

PREVIOUSLY AT

The state of global private equity in 2020 is complex, mainly due to economic activity drastically contracting since the second quarter. Experts anticipate a protracted recession that will see economies only rebounding sluggishly in 2021 and 2022. Consumer income has been deeply impacted, and many businesses are on the brink of collapse. In these extraordinary times, what are the main challenges that private equity funds face?

Private Equity Has Evolved Since the 2008 Financial Crisis

During the last recession following the financial crisis, private equity funds were unable to take advantage of buying opportunities as asset valuations lowered. The current situation is, however, fundamentally different. In 2007-09, the real economy suffered from a tightening in credit caused by excessive risk-taking in the financial sector. In 2020, however, consumer demand has dried up, leading to a demand-based shock to the economy. Private equity funds’ impact comes from their portfolios rather than from excessive leverage and the infamous “refi-cliff.”

Since the last crisis, the industry has evolved. Funds have expanded and have attracted new, more sophisticated investors who have increased their ability to withstand a downturn. At the same time, many years of expansionary monetary policy and the consequent search for yield have provided the sector with unprecedented amounts of available capital, the so-called “dry powder,” which in turn has pushed up demand for target companies. Increased competition for assets has pushed valuations to very high levels, increasing the need for effective portfolio management and efficiency both within the fund and in their portfolio companies. Finally, the entire sector has expanded and grown in sophistication, with the emergence of private credit funds, venture capital funds, and distressed funds that can support companies in different stages and different financial conditions. The increase in sophistication has pushed more traditional PE investors toward increased discipline, excellence, and sector specialization. In light of this profound industry evolution, increased regulation, macroeconomic uncertainty, and years of depressed interest rates and low yields, how is the private equity sector set to perform?

One thing is clear - funds that can exert operational and financial excellence and are set up for rapid transformation will not only be able to withstand headwinds but also swiftly take advantage of the opportunities that naturally arise from a crisis. Flexibility and rigor will be the critical determinants of success in the private equity industry. For this reason, we will look more at macro trends than a numerical analysis - forecasting from an outlier is not informative of future trends.

What Did the Industry Expect Before COVID-19?

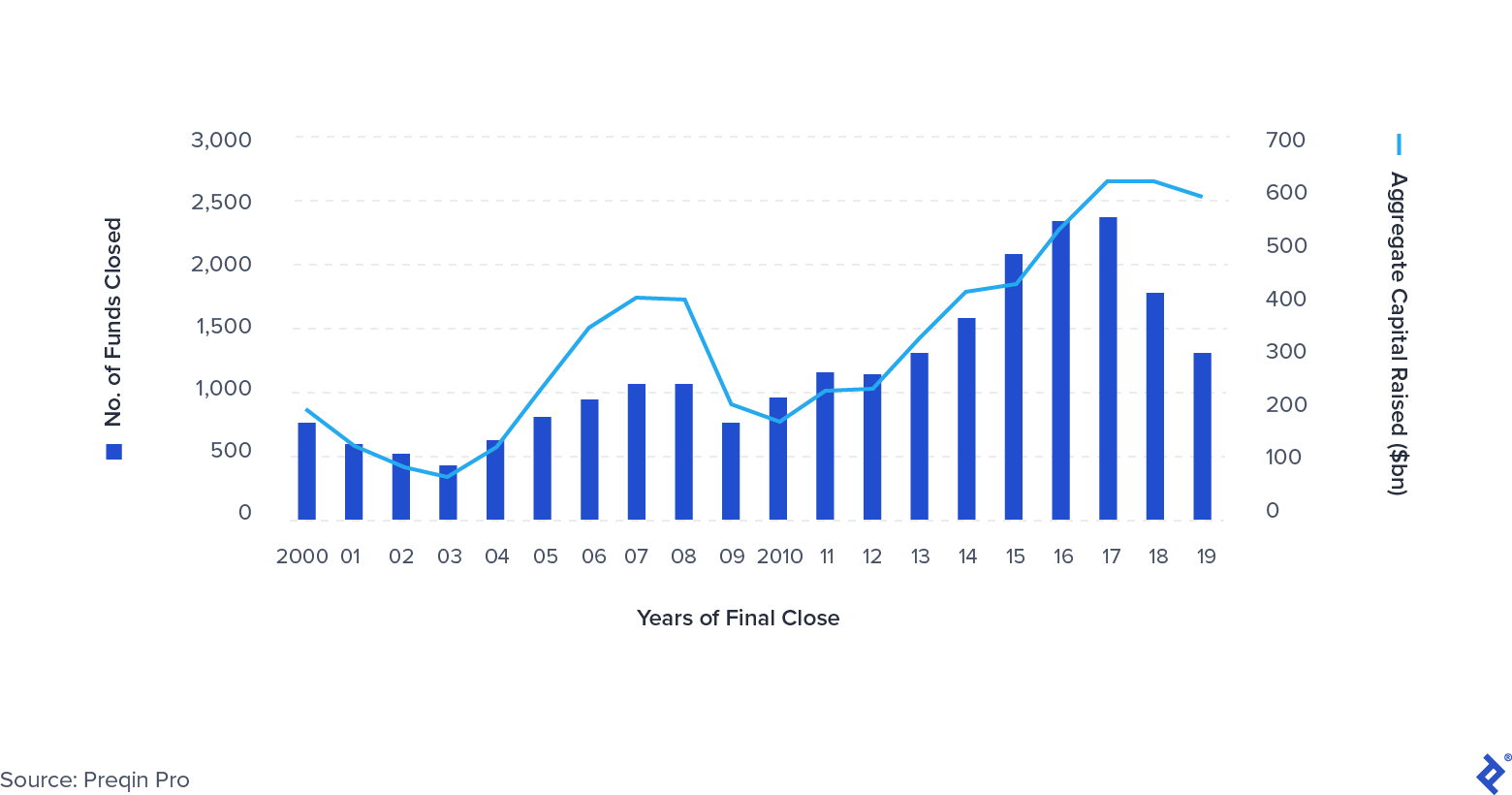

Before COVID-19, some clear trends were emerging in PE. Funds were becoming increasingly large, with the emergence of the so-called “mega-funds” - the average fund had surpassed $1 billion in size. The total number of exits declined, particularly those executed through IPOs and secondaries (sales from one private equity fund to another). Another clear trend is toward consolidation. Fewer firms attract an increasingly large share of the capital deployed by LPs - the winners here are firms like Apollo, KKR, Platinum Equity, and Warburg Pincus. The amount of money raised remained near all-time highs, increasing pressure on funds to deploy their dry powder effectively.

Global Private Equity Fundraising 2000-2019

A Recession Was Already in the Cards

As 2020 approached, many in the financial community were already bracing for a recession driven by global geopolitical tensions, the impact of Brexit, and the slowdown of Chinese growth. However, few were prepared for anything of the magnitude that COVID-19 brought. Private equity investors had begun to adapt their behavior accordingly, with the total number of deals decreasing in 2019. However, the slowdown was slightly countered by the increased pressure to invest, brought on by the substantial amounts of capital raised in prior years. All in all, these circumstances put pressure on performance, forcing funds to focus on financial and operational excellence to sustain returns.

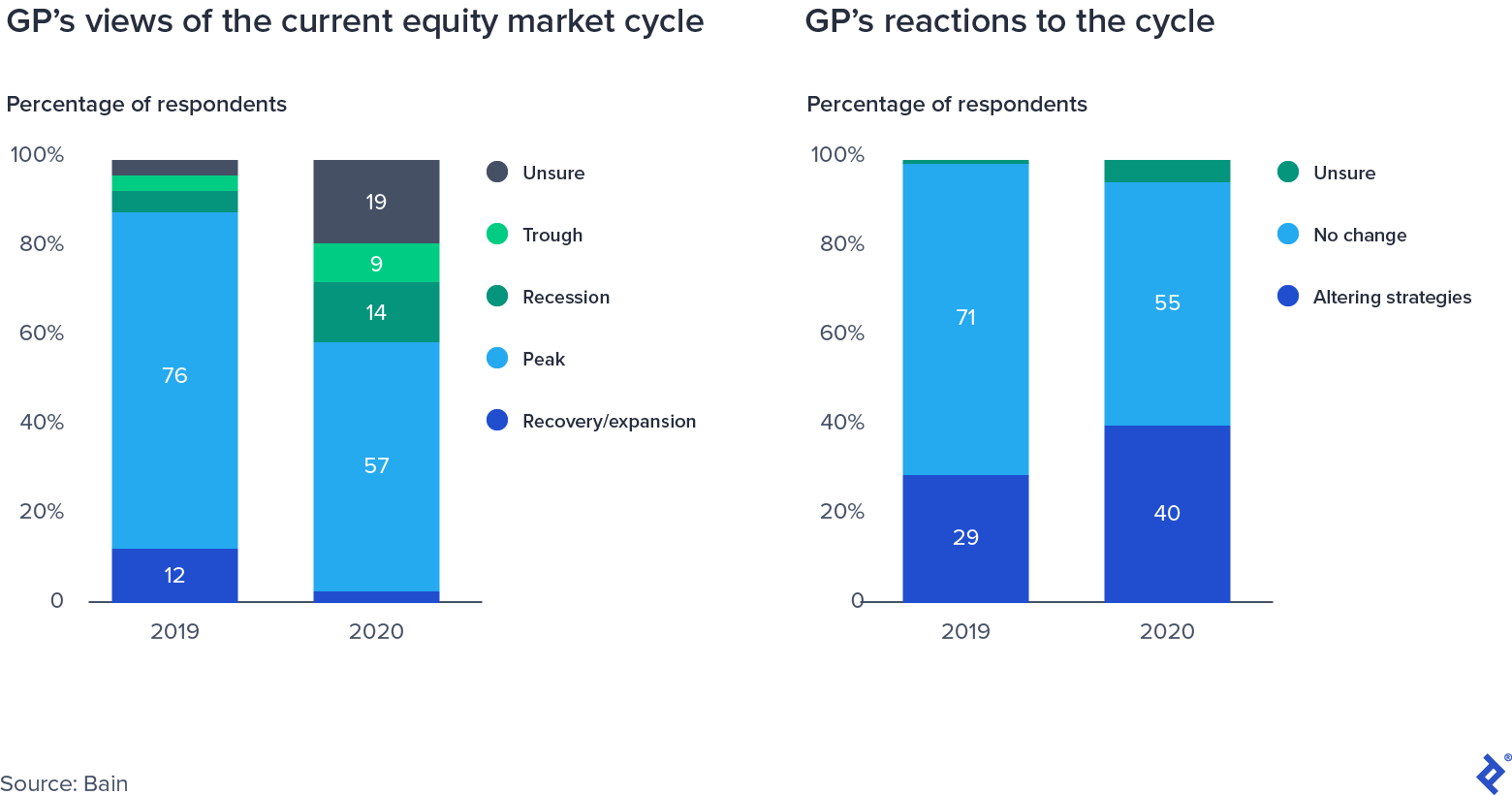

GP’s Survey Responses on Equity Market Cycle

Deal Multiples Kept Increasing and Were on Track for All-time Highs

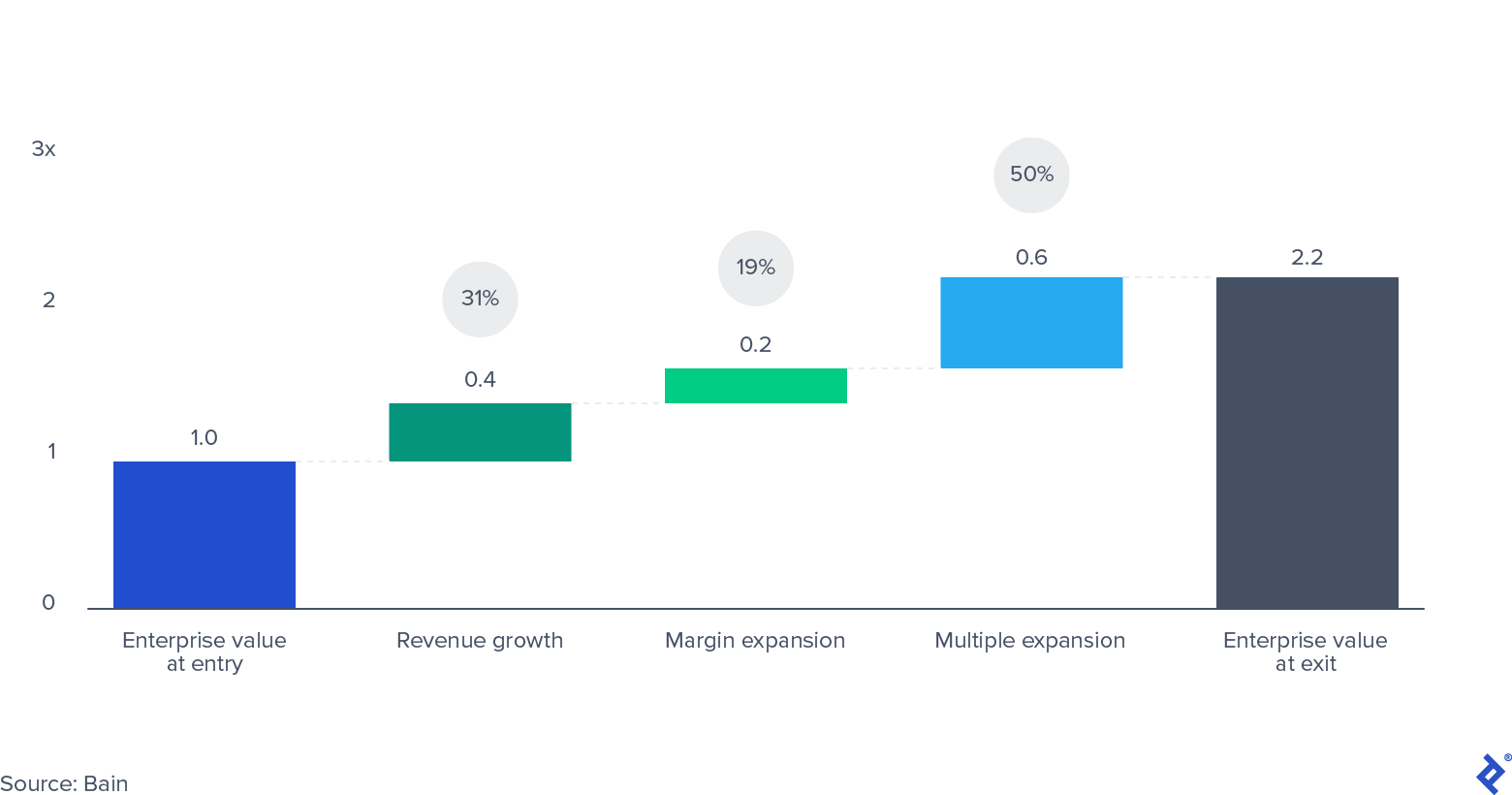

High deal-valuation multiples are a double-edged sword for private equity funds. On the positive side, they have a positive effect on the value of the companies already in the portfolio, sustaining mark-to-market valuations and creating a fertile environment for lucrative exits. As illustrated by data collected by Bain, multiple expansion accounted for half of all the value that private equity funds have created for their investors in the last 10 years.

Pooled Enterprise Value for US and Western European Buyouts 2010-2019

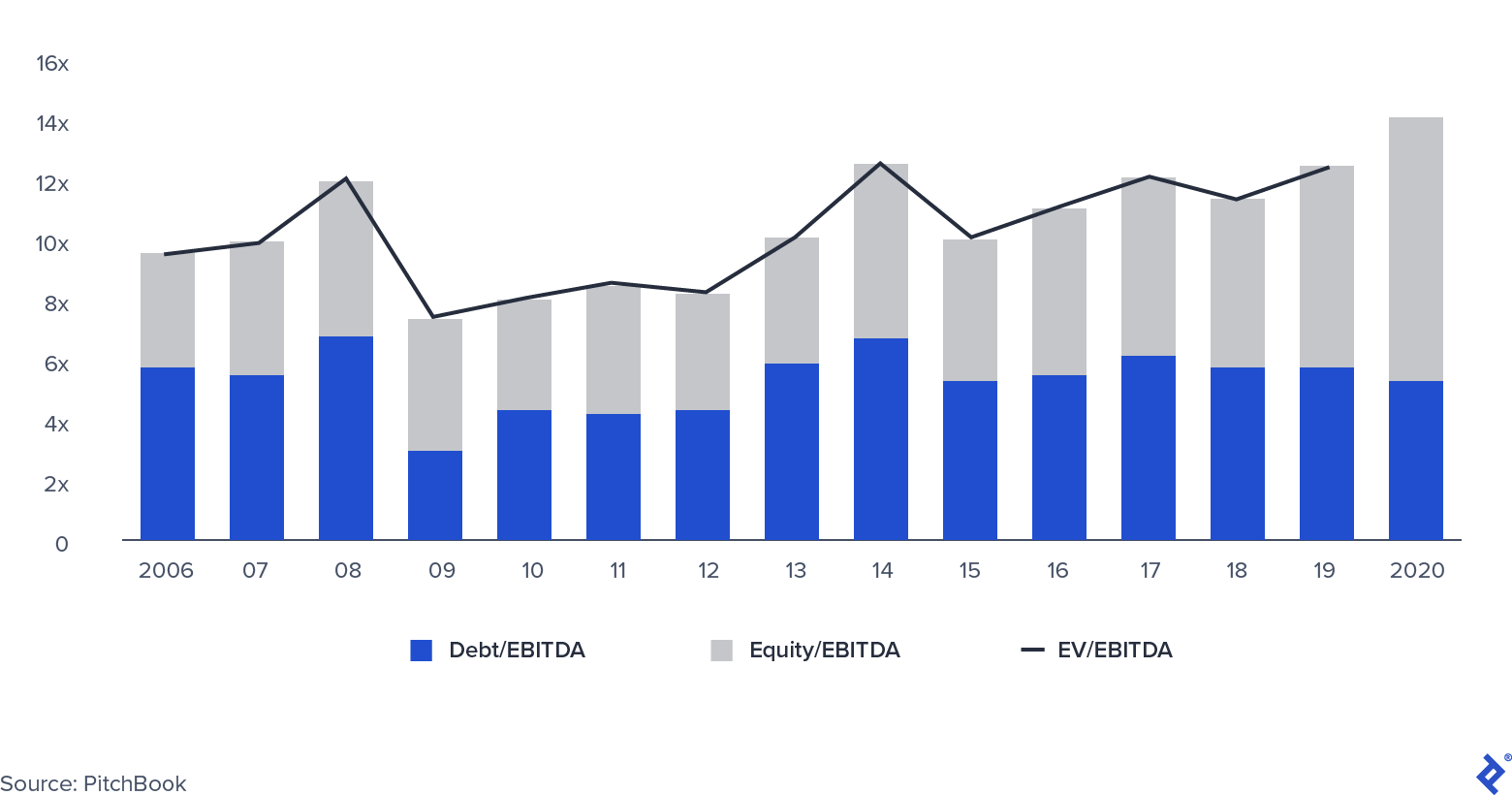

However, the flip side is that deals entered at higher valuations (and thus higher multiples) stand a substantially lower chance of ever appreciating on their initial mark. This leaves funds with two levers for returns: revenue growth and EBITDA margin expansion (in other words, increased operational efficiency and cost reduction). As recessions hamper revenue growth, margin expansion and increased efficiency move to the forefront of management teams’ focus. Deal multiples were poised to be at a post-crisis high as recently as the second quarter of 2020.

Median PE EV/EBITDA Multiples

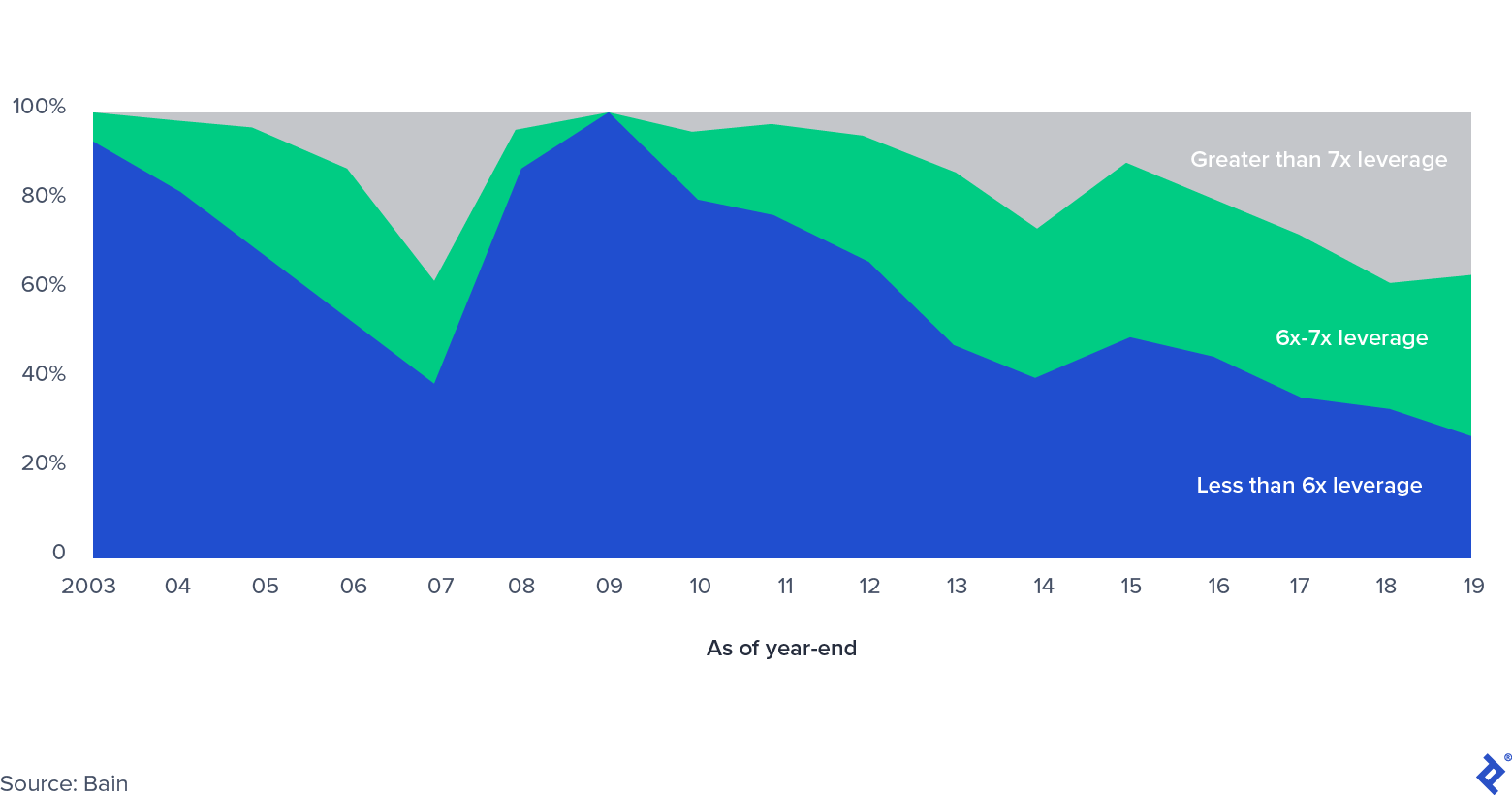

What About Leverage?

Share of US Leveraged Buyout Market, by Leverage Level

As deal multiples increased, so did leverage applied to each transaction, which has surpassed pre-financial crisis levels. At that time, there were fears of the so-called refi-cliff, the vast amount of leveraged buyout (LBO) debt coming to maturity as banks faced huge balance-sheet constraints as the syndicated loan market ground to a halt. A new development in private markets - the emergence of private debt funds - has alleviated pressure in this sector, offering LBO sponsors new avenues for obtaining credit. The private credit market came to prominence as banks were forced to de-risk their balance sheets, and private market investors stepped in with credit vehicles, often under the same umbrella as private equity funds. The market has enjoyed robust growth since reaching more than $800 billion in assets under management in 2019.

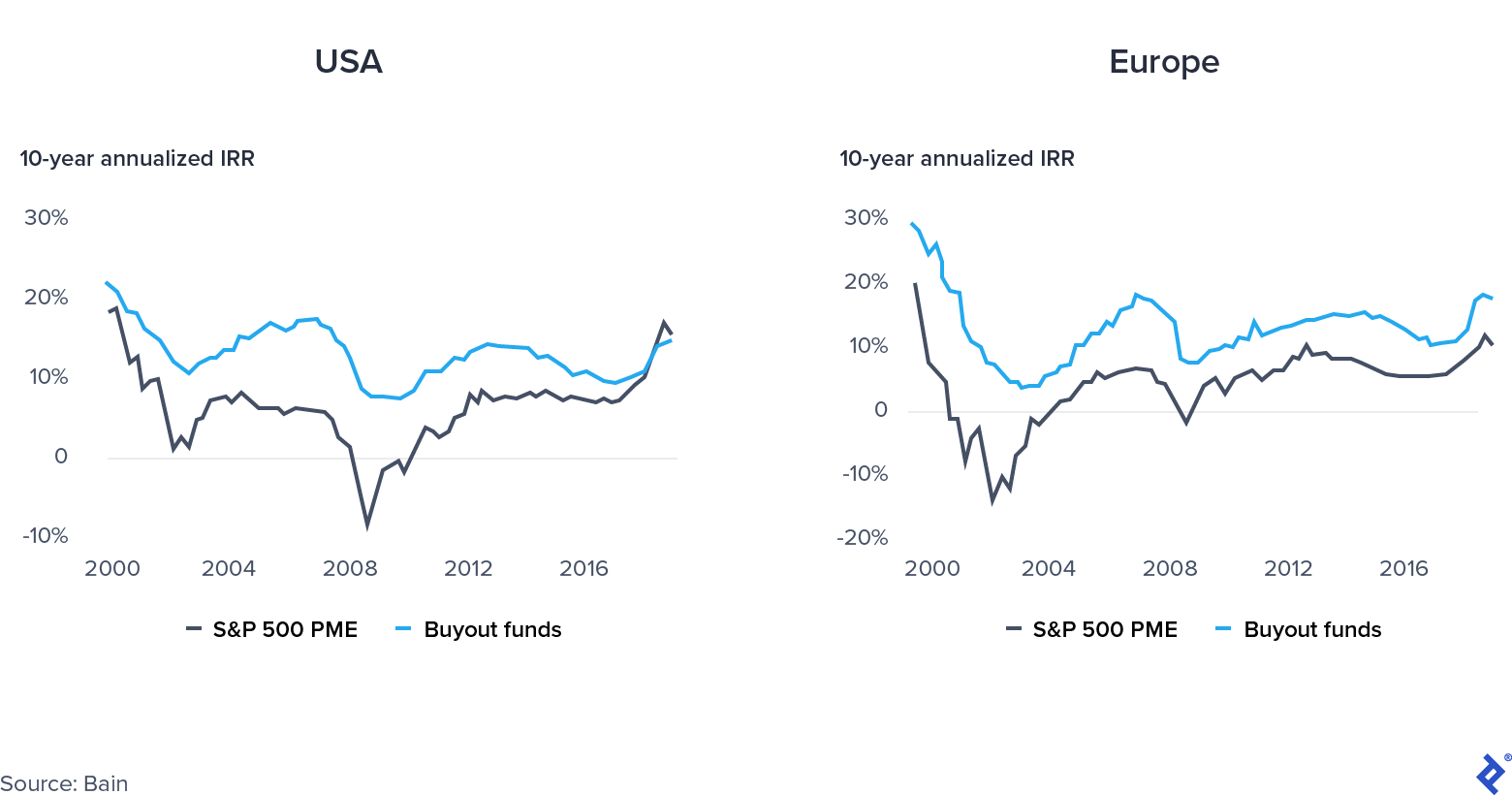

Public or Private Equity: Where to Invest?

Private equity returns in 2019 were largely the same as public market returns in the United States. The lack of performance put additional pressure on funds to perform.

Public vs. Private Market Convergence

What were the causes behind this trend?

- Flight to quality from long-only funds in European public markets, driven by political instability in the region.

- Excessive PE exposure to “old economy” sectors while the sustained rally in tech stocks bolstered the S&P 500.

- PE investments at high valuations made high IRR performance difficult to achieve.

What Happens Now for Private Equity?

Private equity funds that are ready to operate flexibly, effectively support their portfolio companies, strategically select sectors to invest in, and take advantage of monetary and fiscal easing and the drop in multiples will set themselves up for success, or at least increase their resilience.

Is the Pandemic a Supply or Demand Shock?

Demand and supply shocks are fundamentally different in nature. A supply shock is an unexpected event that affects the supply of a good or a commodity, in either direction, such as a disruption to a supply and distribution chain. On the other hand, a demand shock is a change to the demand side (a natural disaster or a terrorist attack are good examples).

COVID-19 is unique as it has created both a demand and a supply shock simultaneously. Movement restrictions to goods and factories operating at lower capacity have affected the supply side, while lockdowns and widespread unemployment have affected demand. According to economists David Baqaee of UCLA and Emmanuel Farhi of Harvard, “Both reductions in supply and demand lower real GDP. However, for policymakers, separating demand shortfalls from supply constraints is important because they require different remedies.”

The remedies for either side can potentially exacerbate problems on the other. For example, lowering interest rates to stimulate demand can lead to supply-side issues from shortages and inflation.

Does This Mean That There Are No Opportunities?

Despite the gloom, the current crisis also brings great opportunity. Governments are intervening heavily and supporting economies in different ways on both the supply and the demand side: for example, the European Union’s Recovery Fund, on the one side, and furloughs and stimulus packages on the other. The unique combination of fiscal and monetary easing, paradoxically, is creating an exciting window for investment opportunities and for supporting portfolio companies.

On the investment side, funds that have adequate deal-sourcing capacity and sufficient dry powder are able to acquire companies that have suddenly come into distress and are looking for capital injections, including public companies looking to go private or conglomerates looking for buyers for non-strategic business lines. Furthermore, private equity funds have resources to support portfolio companies in increasing operational efficiencies (private equity firms have enormously improved their operational abilities, increasing the number of operating partners by 30% in just five years). Other areas in which they can assist companies are:

- Navigating debt-restructuring processes when credit events have occurred

- Helping with government assistance scheme applications

- Through capital deployment when it is admissible under their limited partnership agreements

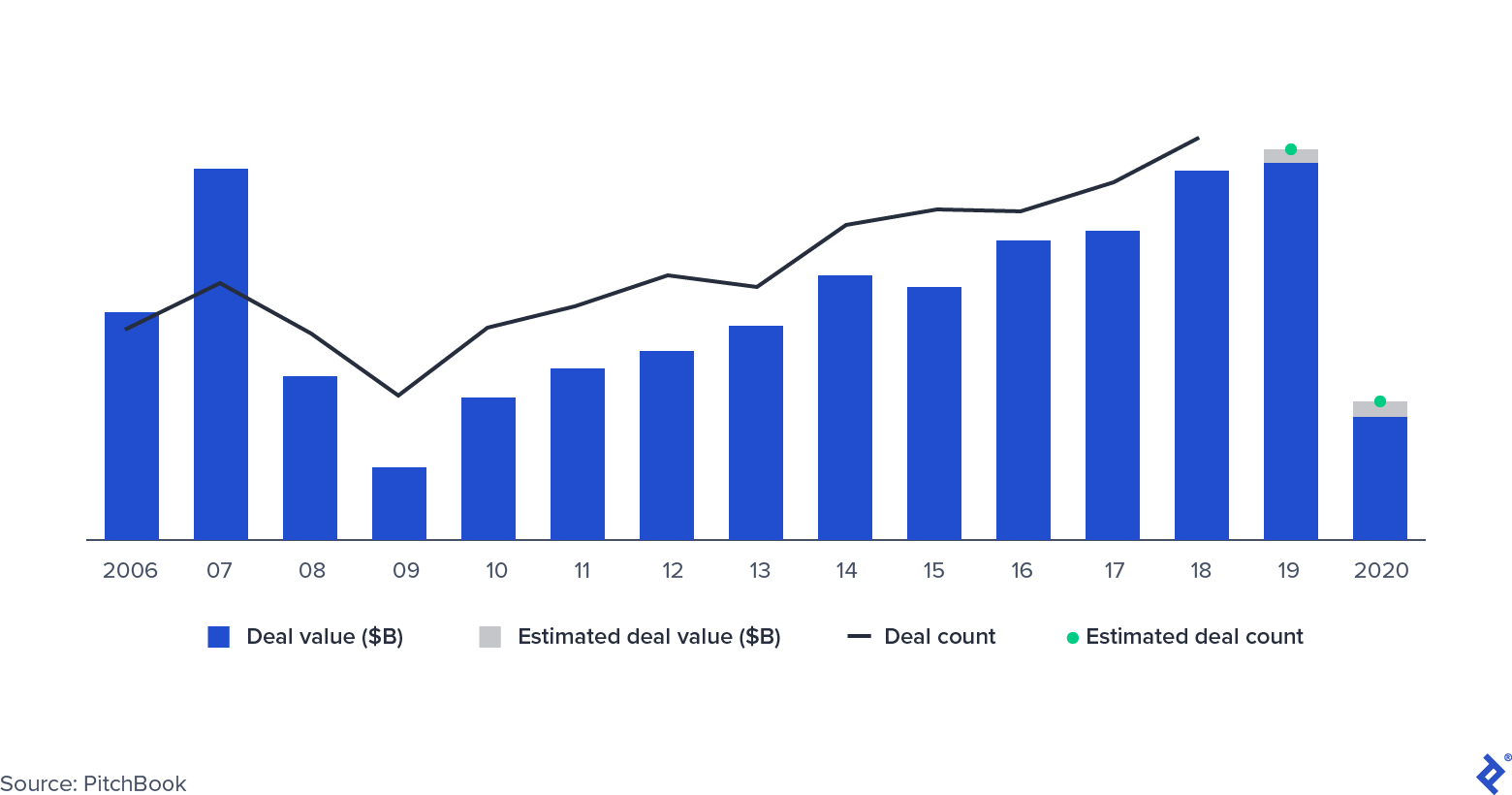

What Deals Still Happened?

PE Deal Activity

Deal activity sank by half during the global financial crisis and has followed a similar trajectory in the first half of 2020. Several factors could ease the fall this time around, even though many deals that had been negotiated before are currently on hold. Some PE managers in the United States have invoked MAC (materially adverse change) clauses, which are a standard feature of M&A contracts. MAC (or MAE, materially adverse effect) clauses protect buyers in the case of events that significantly reduce company valuations, allowing them to pull out of deals. Historically, courts in the United States have rarely sided with the buyers. Nonetheless, invoking the clause can delay the transaction. Two prominent examples are the acquisition of American Express Global Business Travel by Carlyle and GIC and the scrapped transaction between L Brands and Sycamore Partners over Victoria’s Secret.

Some deals were successfully executed, and many of them were private investments in public equity (PIPE) transactions: deals where PE funds acquire stakes in companies that are publicly listed, take board seats, and plan future strategy. Apollo and Silver Lake did this when they invested in Expedia in April with $3.2 billion, $2 billion of which in debt, and $1.2 billion in equity.

How Are Portfolio Companies Faring?

Not all sectors have felt the impact of COVID-19 disruptions in the same way. Software companies, for instance, have continued to boast large returns, while travel and hospitality, in particular, have felt the force of the crisis as consumers alter behaviors and stay at home.

Private equity funds have different strategies at their disposal to assist portfolio companies. They can pivot them toward growth, sustain them with capital in a period of slowed business, or assist through a restructuring process.

Strengthening growing business areas particularly suits companies that operate in sectors that are suffering and serve customers whose behavior has changed, perhaps permanently, because of the pandemic. For example, Deliveroo, a London-based unicorn specializing in restaurant food delivery, has invested heavily in ghost kitchens - remote locations that specialize in delivery-only - thus allowing the company to capitalize on the shift to eating at home.

Hibernation may be the best option for others, such as those in the hospitality (68% of hotels are currently utilizing less than 50% of their employees) and fitness industries. As private equity-owned companies are (mostly) not eligible for the Payroll Protection Program, firms can intervene by supporting companies with follow-on funds.

Finally, for some companies, particularly those in the retail sector, there may be no other viable options aside from restructuring. Often, companies will first file for Chapter 11 and then go through a renegotiation of their debt and a rationalization of their operations. Some recent, high-profile examples are Neiman Marcus and J.Crew.

Private equity firms have marked down portfolio valuations (not all to the same extent) and are more likely to hold onto assets for longer, eschewing forced exits. Once immediate issues such as liquidity and covenants were addressed, the attention of investors shifted toward addressing problems with supply management, their workforce, and long-term value creation.

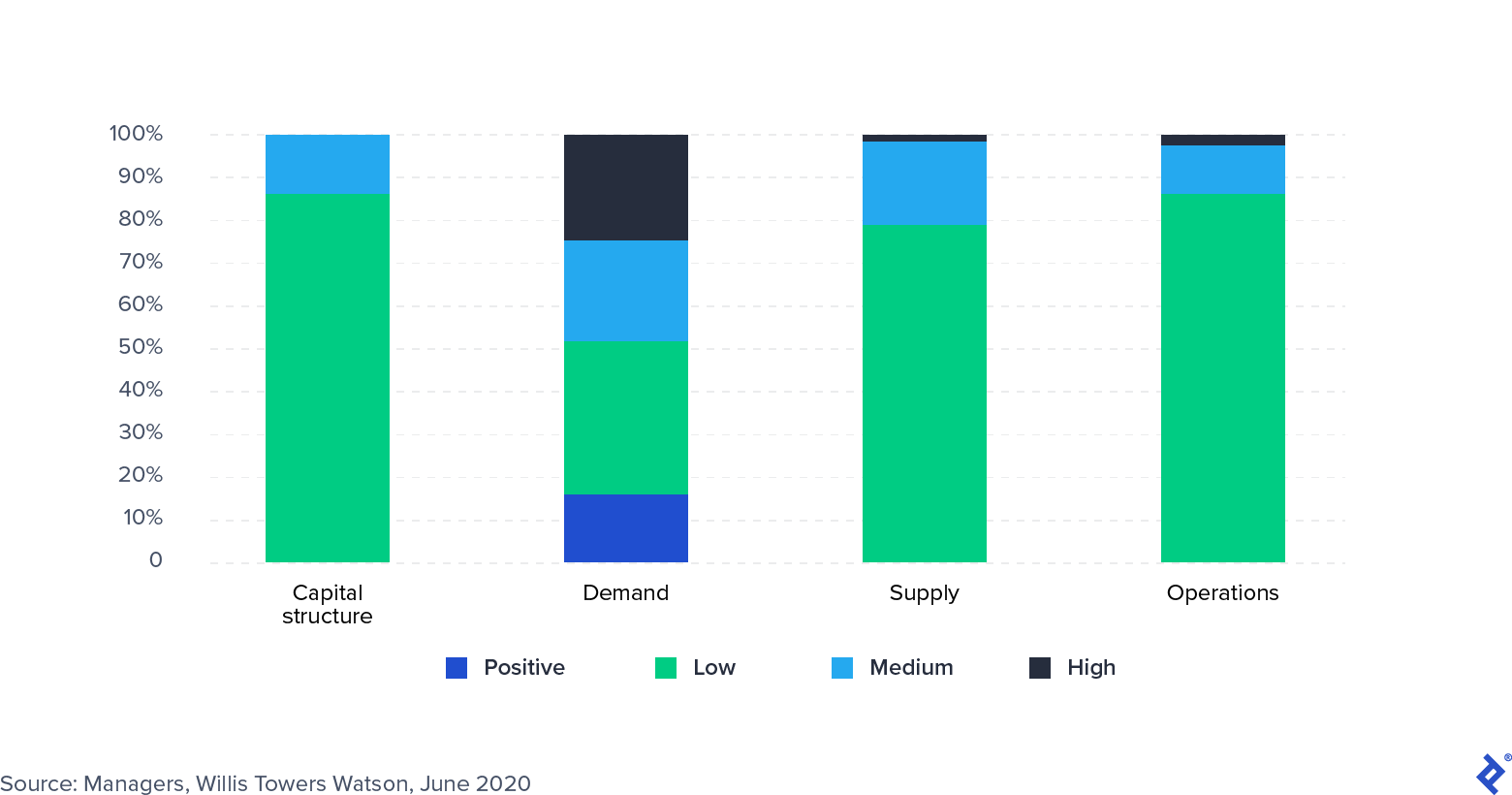

Survey: Impact of COVID-19 on Portfolio Companies

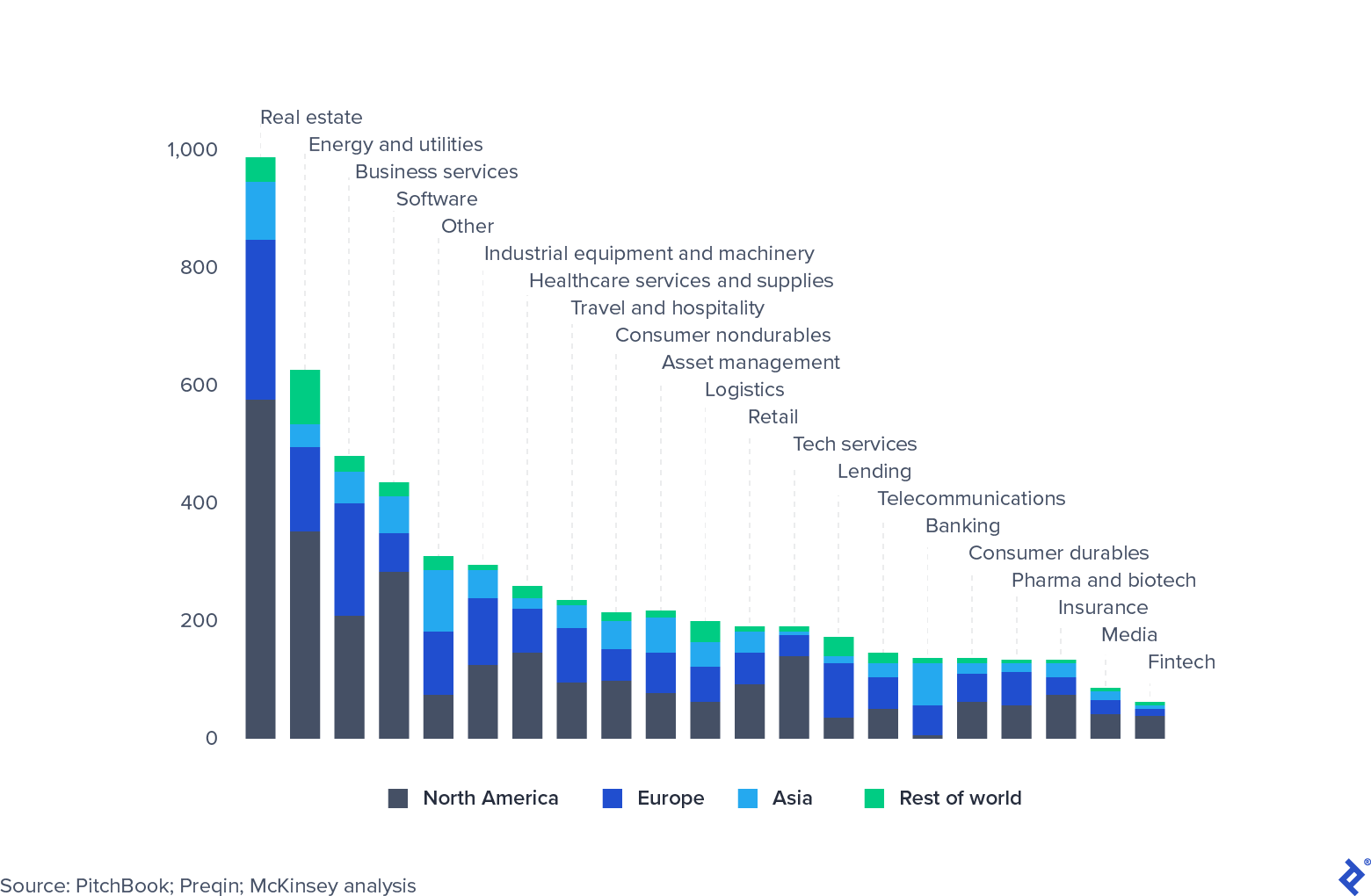

Private Equity Funds Have High Sector Concentration

Private equity funds have large sector exposures. By far, real estate is the most considerable exposure, as it has been heavily affected by the current downturn. However, not all sectors have suffered in the same way. Software and technology have held up incredibly well, particularly those companies that enable remote work and productivity management. Many private equity firms have started looking more closely at the sector and are increasing allocations. Alternatively, funds are looking for opportunities to purchase bargain assets in industries that have been badly affected, such as travel (Expedia’s refinancing is an excellent example).

Global Private Equity AUM, March 31, 2020, $billion

As Multiples Expect to Tumble, PE Can Catch Up with Public Markets

In 2019, private equity returns compressed and tracked those of public equity markets. Even though this did not prevent LPs, family offices, and sovereign wealth funds from allocating capital toward the sector, it did increase pressure on managers to justify their costly fee structure. What can private equity funds do to combat this return compression and convergence?

- Funds can retrench into local markets and take advantage of incentives from public policy to support the economy.

- Funds can increase sector specializations. This is a particularly appealing strategy for smaller funds, which struggle anyway to compete for deals with deeper-pocketed mega-funds. Becoming a niche specialist is likely to become a popular strategy pivot.

- Funds can play on the lever of EBITDA margin improvement within their portfolios. For new funds and those with large amounts of capital to deploy, the focus should be on building flexibility and using dry powder effectively when “good deals” come along, thus lowering the average entry margin of their portfolio.

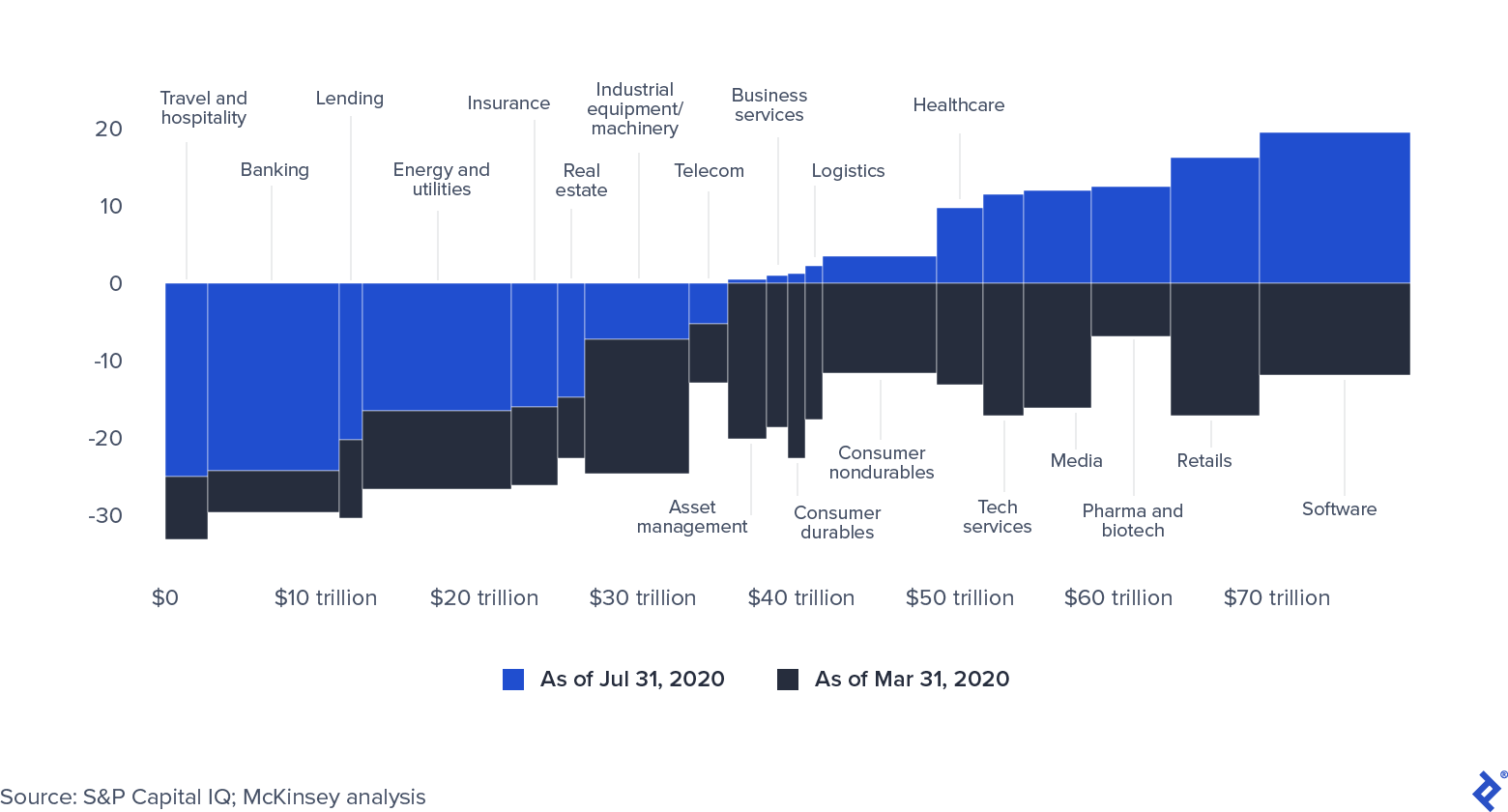

Public equity markets have recovered because of the immense amounts of money that central banks have injected, which stands at $9 trillion in October 2020 (the financial crisis figure was $2 trillion).

Global Market Capitalization by Sector (0= Dec 31, 2019)

Public equity prices are showing signs of being artificially inflated. If the COVID-19 crisis extends further, companies will struggle to maintain their market capitalization. Furthermore, all the abundant liquidity is eventually likely to find its way into the private equity sector, either through additional funds being raised or from attractively priced loan opportunities.

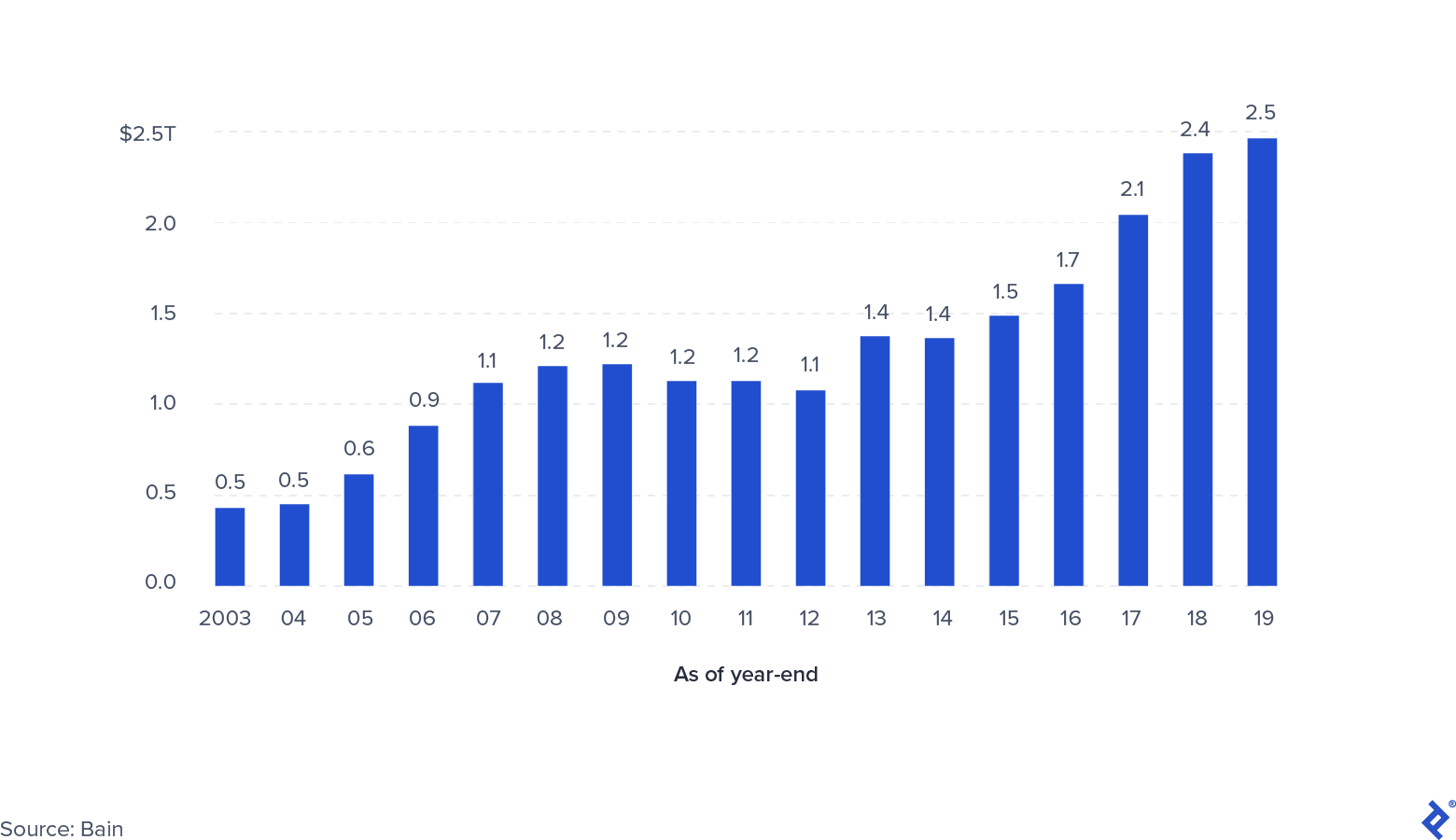

Dry Powder and Liquidity: Still Extremely Abundant

Global Private Uncalled Capital

The total amount of dry powder available to private funds (including credit, real estate, distressed, and venture capital) reached $2.5 trillion at the end of 2019. There are some concerns that this committed capital will not be called. High levels of uncertainty have slowed down deal activity, and it remains unclear when this will abate, which in turn may lengthen the life of existing funds. Those that are most focused on opportunistic buying will be more successful by taking advantage of low entry prices. The fund’s vintage will be a determining factor with those that were close to being fully invested and probably the most hampered in their operations.

On the other hand, it is unlikely that new fundraising activity will cease or slow down significantly. The large amount of liquidity in capital markets requires LPs and other institutional investors, such as pension funds, sovereign wealth funds, and family offices, to find high-yielding, medium-term allocations for their capital. Comparatively speaking, private equity still appears attractive compared to other asset classes, as it is less volatile, focused on medium-term value creation, and effectively aided by active management. The winners will be those funds that can sustain portfolio valuations by providing companies with operational support and potential targets to acquire as bolt-ons.

What Are the Scenarios for the Private Equity Industry Going Forward?

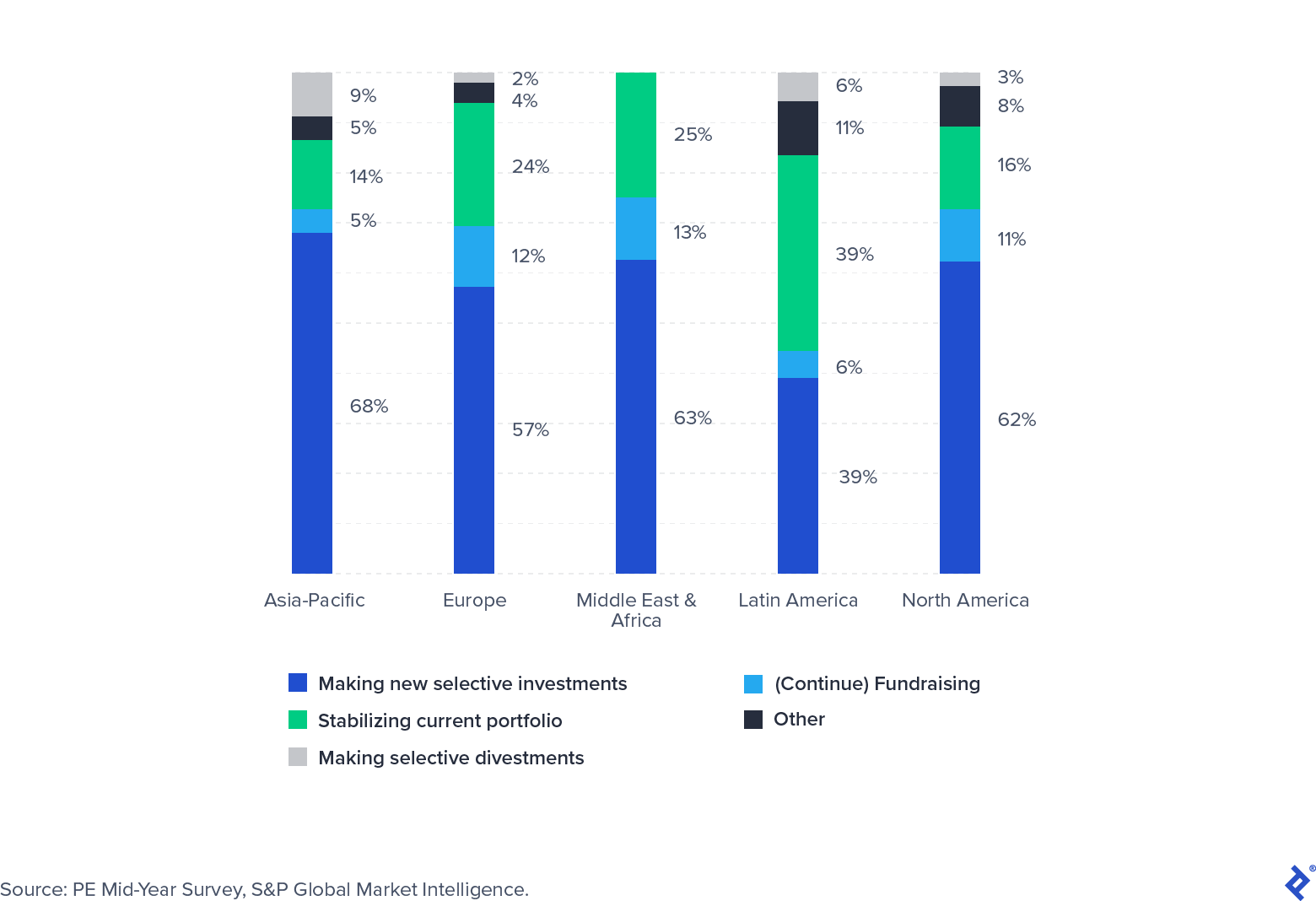

The search for a vaccine, the path of the pandemic, political uncertainty, and the profound change in individuals’ habits will all have a significant impact on the economy. S&P Global surveyed a panel of private equity investors in the summer of 2020 to gather their expectations for the near future. While most indicated that they had primarily spent the second quarter of the year actively stabilizing portfolios, more than half were gearing up to make new investments.

The focus for new investments will be on sectors that grew despite the pandemic (such as software and healthcare) or in which attractive deals have emerged because of temporary, pandemic-induced distress, such as travel.

Investor Focus Survey Q3 2020

COVID-19 has brought disruption to a private equity industry that was already preparing for challenging times. Funds will need to divide their time appropriately (and potentially supplement teams with external contributors) into more operationally focused groups dedicated to maintaining value in current portfolios and groups that can scout and close new deals as they emerge. Flexibility, focus, and a strong relationship with portfolio companies and LPs will be real indicators of success.

Understanding the basics

How big is the private equity industry?

Before COVID-19, funds were becoming increasingly large, with the emergence of the so-called “mega-funds” - the average fund had surpassed $1 billion in size. The amount of money raised remained near all-time highs, increasing pressure on funds to deploy their dry powder effectively.

Is private equity growing?

Since the last crisis, the industry has evolved. Funds have expanded and attracted new, more sophisticated investors. At the same time, many years of expansionary monetary policy and the consequent search for yield have provided the sector with unprecedented amounts of available capital.

How do private equity funds support portfolio companies?

Private equity funds support portfolio companies in: 1) Increasing operational efficiency; 2) Navigating debt-restructuring processes; 3) Helping with government assistance scheme applications; 4) Through capital deployment when it is admissible under their limited partnership agreements.

About the author

Natasha transitioned to venture capital after a career in banking built in prestigious firms such as JPMorgan and ESM.

PREVIOUSLY AT