What Is a Down Round and How to Avoid One

Anyone vaguely familiar with the venture capital industry knows that down rounds are bad news. But what exactly are they, and why do they occur? What alternatives do founders have to avoid a down round?

Anyone vaguely familiar with the venture capital industry knows that down rounds are bad news. But what exactly are they, and why do they occur? What alternatives do founders have to avoid a down round?

Natasha transitioned to venture capital after a career in banking, built in prestigious firms such as JPMorgan and A&M.

PREVIOUSLY AT

Executive Summary

What are down rounds and why do they occur?

- A down round is when the pre-money valuation of a fundraising round is lower than the post-money valuation of the round previous.

- Down rounds for private companies occur for the same reasons they do for publicly traded companies, for example:

- Failure to meet investors' earnings targets

- Deteriorated competitive environment

- Tightening of general funding conditions

Implications of a down round:

- The main implication of a down round is the triggering of anti-dilution protection, which means that when shares get sold at a lower price than an investor had originally paid for them, the investor will be diluted less than the other parties.

- Other important secondary implications are negative signaling to the market and investors, a loss of trust and confidence in the company, lower motivation and control on behalf of the founders and management, and a negative hit to employee morale.

Alternatives to a down round:

- Cut costs and increase runway: This will postpone the need for an external fundraise, but may not be feasible for a very lean organization, or for one without significant revenues.

- Raise bridge financing: if the cash flow problem is just temporary, a bridge under the form of a convertible note can be an appropriate solution to get the company back on track.

- Renegotiate with investors: the terms of the round can be renegotiated, for instance by mitigating the anti-dilution protection, or by exchanging these rights for other investor perks, such as upside protection.

- Close up shop: if there are too many problems, employees are disgruntled and your investors will no longer back you, it may be better to cut your losses and start over.

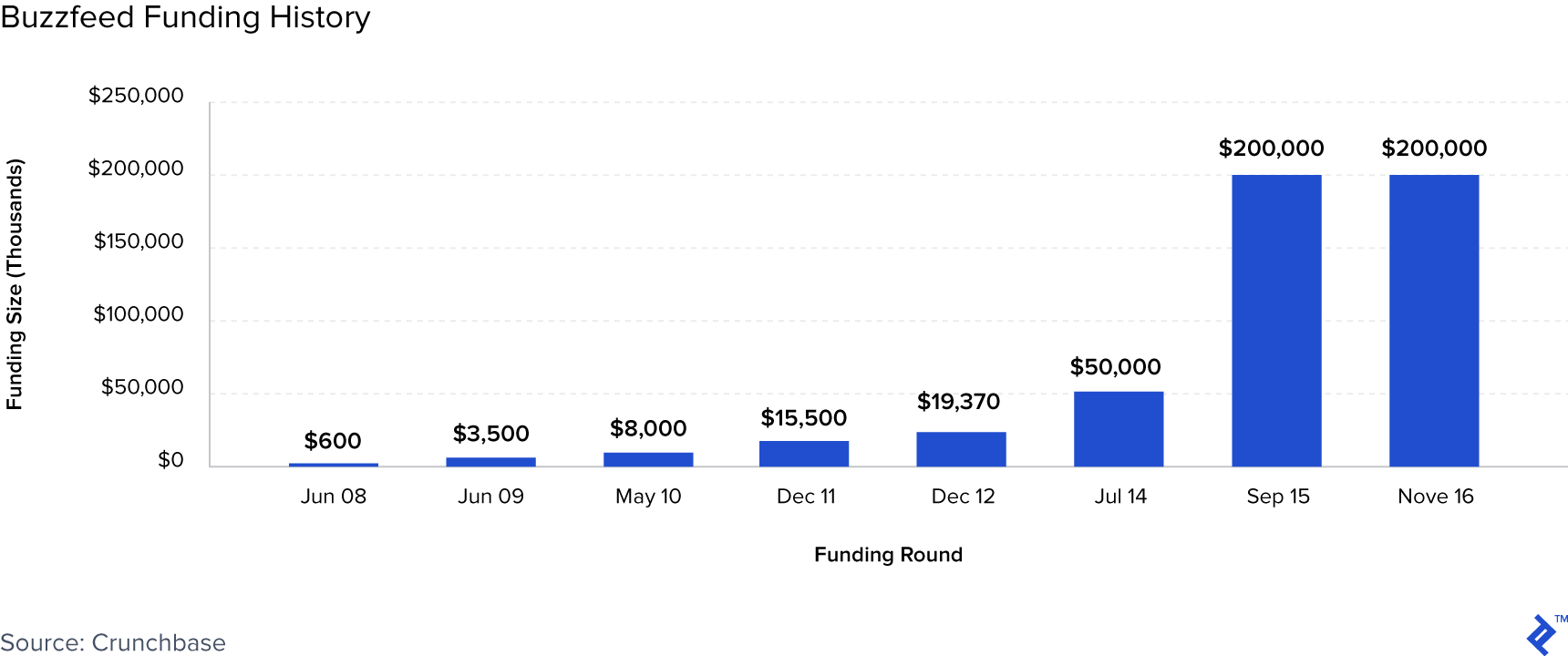

Arguably one of the most influential news companies to have emerged from the internet era, Buzzfeed is a global media powerhouse, racking up over six billion views per month, and generating nearly $300 million in revenue in 2017. All of this in just six years, a period in which it has raised nearly $500 million across eight funding rounds.

But whilst a few years ago Buzzfeed was one of the hottest venture-backed companies around, things have changed in the last couple of years. A few weeks ago, the company announced a 15% cut in its workforce, the third round of layoffs since 2017. These follow a 2016 Series G “flat” financing round, after having missed 2015 revenue targets.

The string of negative news may lead one to think that the company is in deep trouble. But in reality, topline grew by ~7% in 2017, and in a May 2018 interview, Buzzfeed CEO Jonah Peretti mentioned the company was posting “strong double-digit growth.” Why would a company growing so nicely announce such a steady stream of layoffs?

The answer is likely found in a note Peretti sent to employees following the latest round of cuts. The letter, titled Difficult Changes mentioned that “[u]nfortunately, revenue growth by itself isn’t enough to be successful in the long run. The restructuring we are undertaking will reduce our costs and improve our operating model so we can thrive and control our own destiny, without ever needing to raise funding again”. Paraphrasing, Buzzfeed needed to wean itself off its funding path, particularly in the short term if it wanted to avoid a down round.

Readers even vaguely familiar with the venture capital industry likely know that down rounds are considered a very negative thing. In a recent podcast, Motley Fool Money radio host Chris Hill sums it up nicely: “A down round is…such a catastrophic sign….it’s the worst possible thing that can happen outside of a tragic accident of some sort.” But what exactly are down rounds, and why are they so calamitous? Why do they occur and can they be avoided? In this article, I will cover the mechanics of funding rounds and potential tools from the points of view of both the entrepreneur and the investor, and then try to offer some (hopefully) helpful considerations.

What are Down Rounds?

Every time a company raises money, it needs to agree on a pre- and a post-money valuation with its investors. The pre-money valuation is the value of the company at the time of the investment, and it is a fundamental starting point of the process of fundraising. It will give investors an idea of the amount of ownership of the company, of the level of control of the founders, and the incentive alignment between them, their investors and their key employees.

During a capital raising transaction, the company issues a set number of new shares against a fixed amount of capital. Each share is then priced at a fraction of the new capital base in the company. We thus will have two resulting valuations, a pre and a post-money. We call a round a down round if the pre-money valuation of a subsequent round is lower than the post-money valuation of the round previous. The difference between the two is the amount of capital raised. We will go through a numerical example in the section below.

Mechanics of Funding Rounds

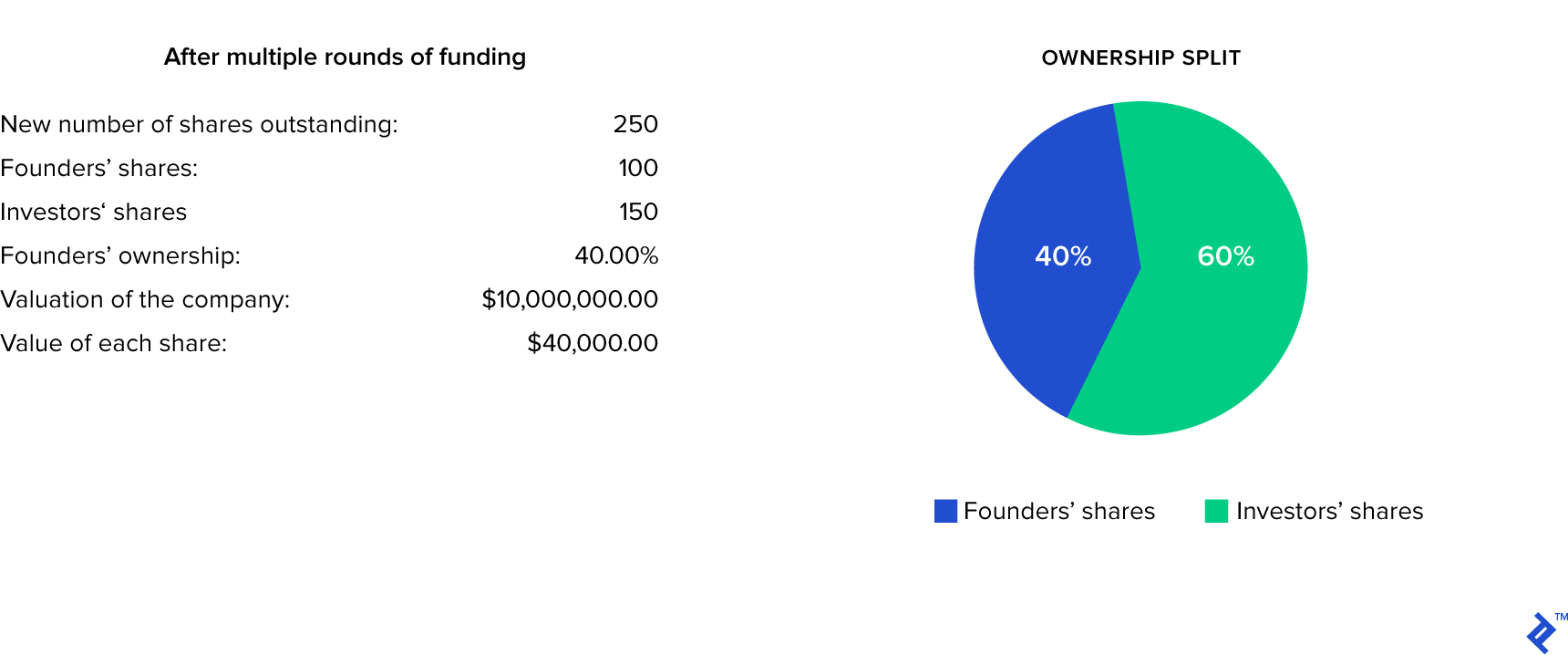

Let’s imagine a company that has raised one round of £150,000 from friends and family at a valuation of £1 million pre-money. The founders originally had 100 shares.

This is what happens to the company:

Let’s imagine that this company then grows and goes on to raise other rounds of funding until the shareholder split looks as follows:

Company valuation: £10,000,000

Founders ownership: 40%

Investor ownership: 60%

The founders still own 100 shares, so we can calculate the share price as follows:

40%*£10m=£4m

£4m/100 = £40,000

Investors now hold:

60%*£10m=£6m

£6m/£40k= 150 shares

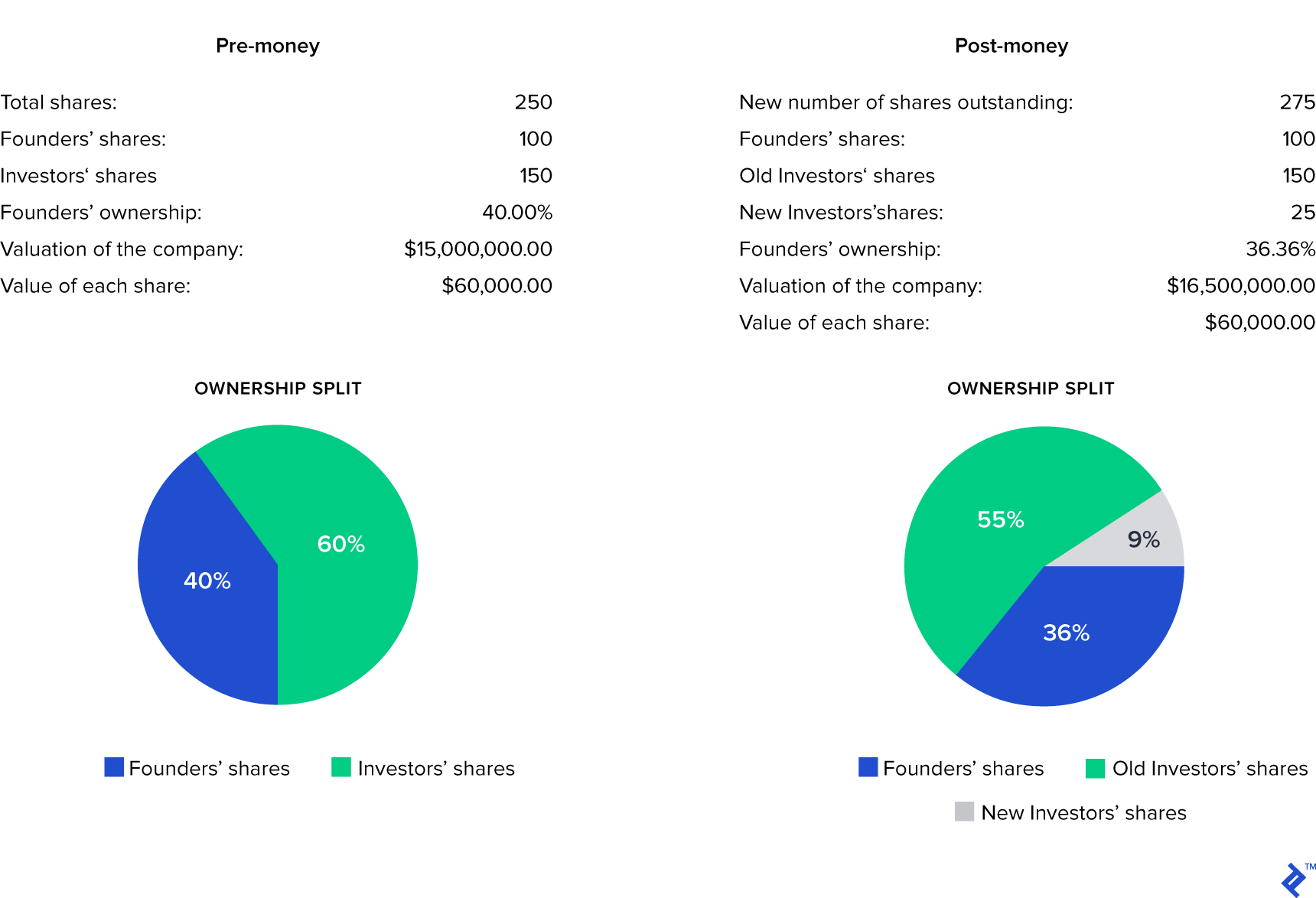

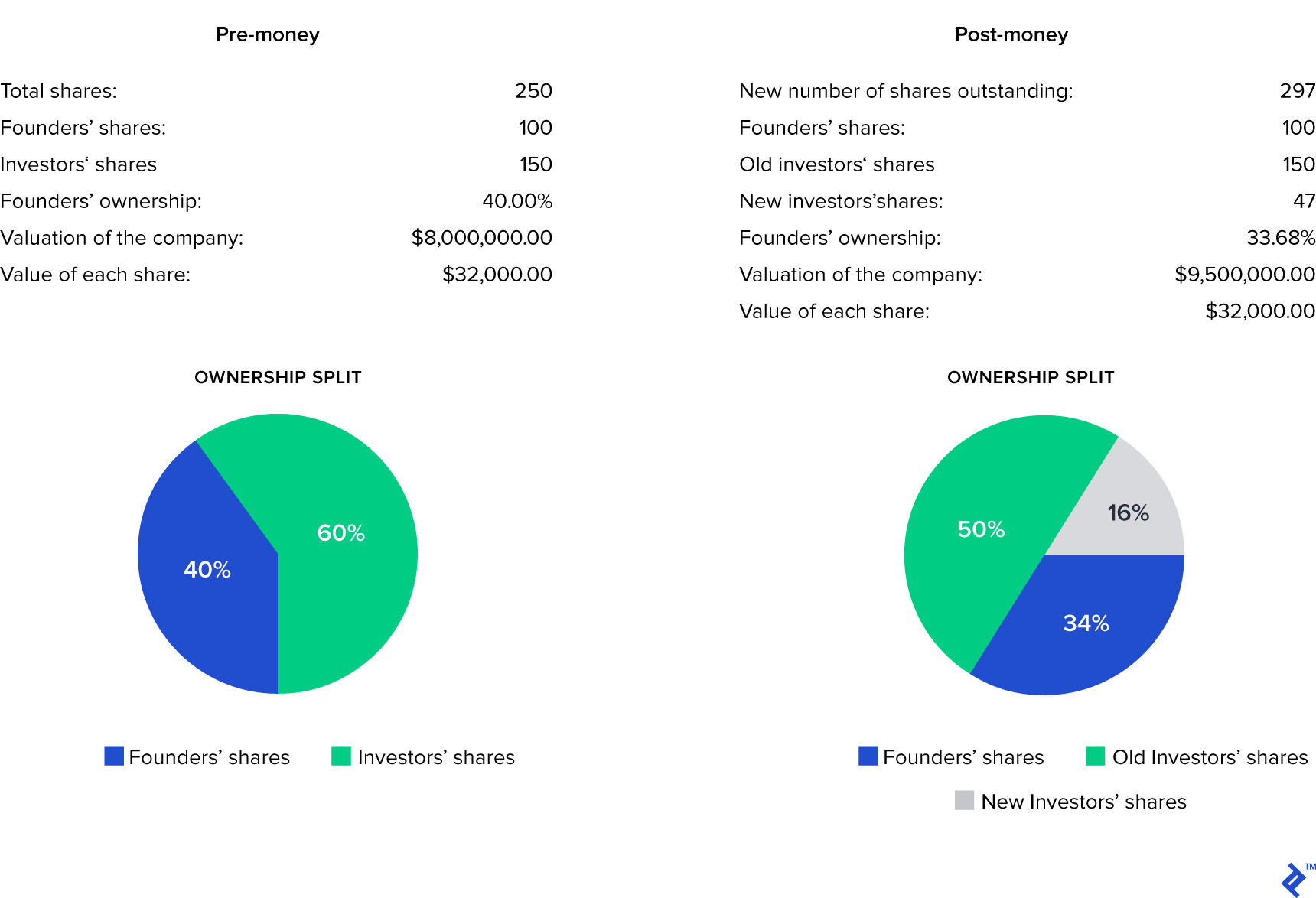

Let’s assume now that the company needs a £1.5 million investment. Below I run through the mechanics of an up round, a flat round and then finally a down round.

Up Round Example

So the founders and the original investors have been diluted and thus own less of the company, but at the same time, the increase in share price has more than compensated for the dilution.

Flat Round Example:

In this scenario, both the founders and the old investors have given up some of their control and of their upside in exchange for the new capital.

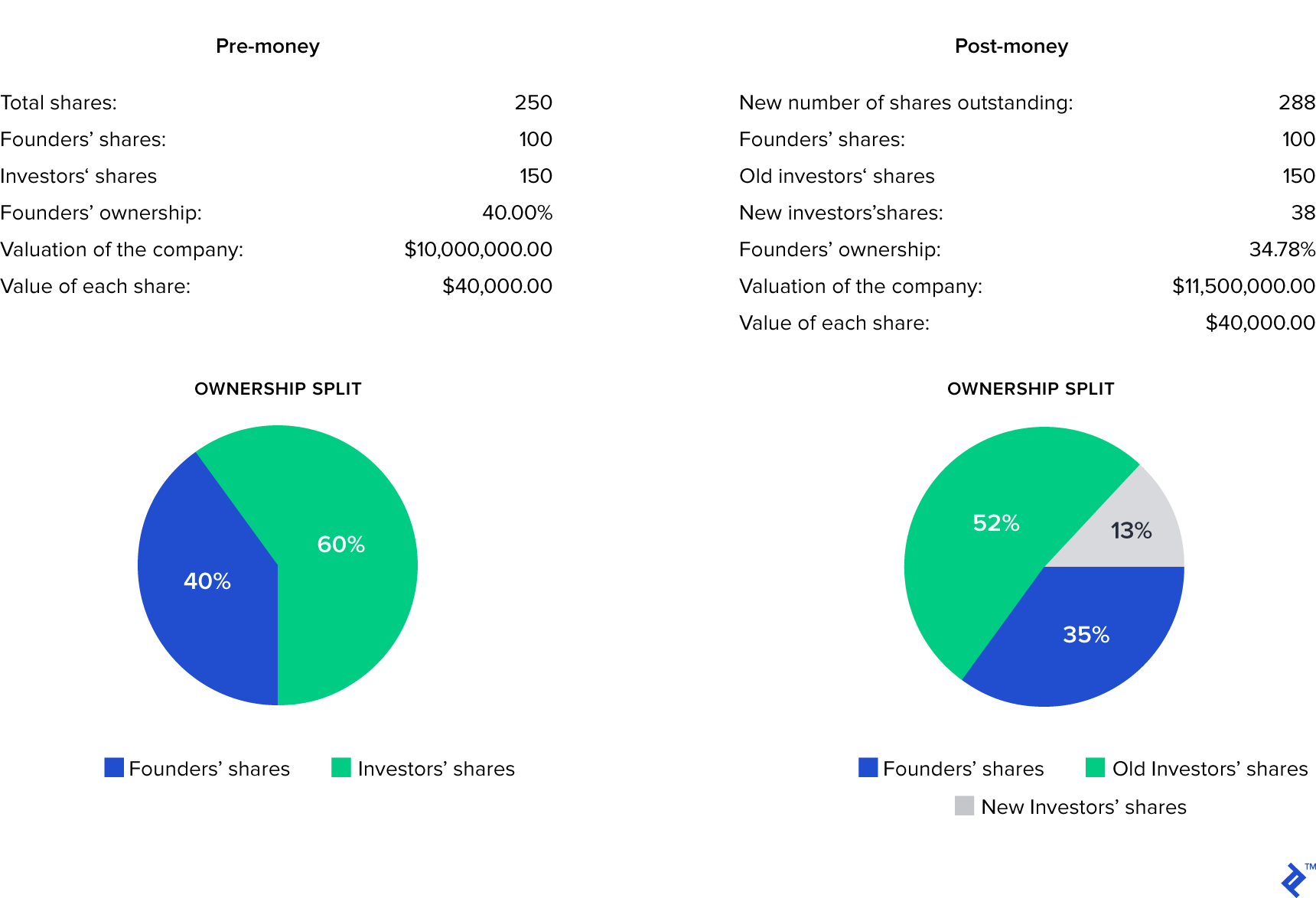

Down Round Example:

Clearly, in this case, the negative effect is even greater: not only are the shares worth less, but the dilution effect is even larger.

N.B. One important factor that we are ignoring in our calculations for simplicity is the employees stock option plan - employees are greatly affected by the fact that more shares need to be issued as well as the reduction in share price.

Why do Down Rounds Occur?

Down rounds basically occur for private companies for the same reasons they do for publicly traded companies:

- Failure to meet investors’ earnings targets: If a company fails to reach the necessary milestones, investors growth forecasts will have to be revised downwards, and with them the company’s valuation.

- Deteriorated competitive environment: If new competitors have emerged for a company, the expectations of its ability to grab market share will also weigh on valuation.

- Tightening of general funding conditions: This factor is sadly completely outside of a company’s control - lower investor appetite for private company equity will decrease valuations for everyone.

For a general discussion on how investors value private companies, please check these resources for startups and more generally for private companies.

Implications of a Down Round

Buzzfeed’s example illustrates the conundrum faced by a company seriously entertaining the prospect of a down round. Is there enough savings room in the cost base to avoid going to investors? Can we continue on the right growth trajectory (or perform the right adjustments if needed) with the current cash availability? What will affect employee morale less?

The main implication of a down round, however, is the triggering of anti-dilution protection. Typically, investors will hold a different class of shares from founders and employees. Amongst other different characteristics, the main difference between ordinary shares is anti-dilution protection. In practical terms, this means that when shares get sold at a lower price than the investor had originally paid for them, they will be diluted less than the other parties. This is usually done at the expense of the founders’ shareholding. The two main types of dilution are:

- full-ratchet: most advantageous for investors but potentially more damaging for the company. This heavily reduces the founders’ shareholding in the company and may make it difficult to raise money in the future.

- weighted average: more common - distributes the pain of the dilution of a down-round a bit more evenly. The average used for the calculation can be broad or narrow (including or excluding founders’ shares from the calculation.

Here is a useful illustration from a great post on the topic.

Types of Anti Dilution Mechanisms

Usually, as the terms in a financing round become more punitive the harder it is for the startup to raise funds.

Obviously, a punitive dilution has consequences for a startup:

- Signaling: it sends a signal to observers and employees that a company is strapped for cash and not doing as well as expected. This affects morale, can make larger partnership or client contracts more difficult, and makes raising future funds harder;

- Trust and Confidence: investors and the board may lose trust in the company and interfere with its operations in a way that becomes distracting and cumbersome;

- Motivation and Control: the founders may be so diluted that they no longer have a significant interest in the company and are not able to control it appropriately. There are many trade-offs to founder control and considerations that can be made, but generally, for an early stage startup, the founding team and the key employees are the most important asset they have. Losing them can be very disruptive;

- Employee Morale: finally, employee morale can be significantly affected. Employees usually hold options on common stock and are the ones that stand to lose the most if the company’s valuation is substantially lowered in time. Their options may be worth substantially less (or be underwater entirely) and they may have already incurred some tax losses.

Alternatives to a Down Round

So what are the alternatives for an entrepreneur faced with a potential down-round?

- One of the first and most obvious options is following Buzzfeed’s example and cutting costs to make the money in the bank last longer. This will postpone the need for an external fundraise, but may not be feasible for a very lean organization, or for one without significant revenues. Furthermore, start-up revenues can fluctuate a lot, particularly in difficult times;

- Raise bridge financing: if the cash flow problem is just temporary, a bridge under the form of a convertible note can be an appropriate solution to get the company back on track;

- Renegotiate with investors: the terms of the round can be renegotiated, for instance by mitigating the anti-dilution protection, or by exchanging these rights for other investor perks, such as upside protection. Investors that are close to you and believe in what you do want to see you succeed;

- Close up shop: if there are too many problems, employees are disgruntled and your investors will no longer back you, it may be better to cut your losses and start over. While this is undoubtedly painful, it may be better, in the long run, to start with a clean slate and without bad blood.

A Word of Caution

The outlook for the global economy is looking weaker and weaker. The IMF recently slashed its economic forecasts, and even Apple cited China’s economic slowdown in its revised earnings guidance. In this climate, entrepreneurs and investors in private companies should prepare themselves for the consequences of an inevitable tightening of funding conditions, especially the dreaded down round. As Fred Wilson points out in his outlook for 2019, even though the tech industry is somewhat immune to macro-economics swings he anticipates that “… a difficult macro business and political environment in the US will lead investors to take a more cautious stance in 2019. It would not surprise me to see total venture capital investments in 2019 decline from 2018. And I think we will see financings take longer, diligence on new investments actually occur, and valuations to come under pressure for even the most attractive opportunities.”

The best way to avoid down rounds is to be prudent and strategic when raising funds. As Y Combinator points out, the temptation to raise as much money as you can is very strong for startups, particularly as large valuations and capital raises are celebrated as markers of success. It is however more effective to raise the cash needed to achieve realistic growth objectives and not be constantly fundraising, which is distracting and stressful.

If, despite good management and good intentions, things do not go according to plan, the main questions to be answered are around what caused the problem: perhaps the valuation was just unrealistic? Is the company just experiencing temporary problems? Do the founders, employees, and investors believe in the company enough to want to tighten the belt and look for a solution? Is it salvageable? Down exits or rounds do not necessarily mean the end of a company but are indeed a great managerial challenge.

Further Reading on the Toptal Blog:

Understanding the basics

What does down round mean?

We call a financing round a “down” round if the pre-money valuation is lower than the post-money valuation of the round previous

What is a flat round in investing?

If the pre-money valuation of a financing round is the same as the post-money valuation of the previous financing round, this is called a “flat” round

How does anti-dilution work?

When shares get sold at a lower price than the investor had originally paid for them, they will be diluted less than the other parties holding different classes of shares

What is the difference between pre-money and post-money valuation?

A pre-money valuation is the valuation attributed to a company prior to a capital raise, whereas the post-money valuation is the valuation of the company after the capital raise. The difference is the amount of capital that has been raised

Why is pre-money valuation important?

A pre-money valuation is important for a variety of reasons. It obviously determines the price at which new investors will participate, it also determines the capital gains of previous investors. It also serves as a signaling effect to market participants as to the performance of a company

About the author

Natasha transitioned to venture capital after a career in banking, built in prestigious firms such as JPMorgan and A&M.

PREVIOUSLY AT