Human vs. Machine: The Next Frontier of Wealth Management

Since the introduction of index funds in the 1970s, the investment management industry has embraced the use of software to enhance its decision-making. With robo-advisors reaching further prominence, will machines replace humans in the world of wealth management?

Since the introduction of index funds in the 1970s, the investment management industry has embraced the use of software to enhance its decision-making. With robo-advisors reaching further prominence, will machines replace humans in the world of wealth management?

Ankur is an experienced financial modeler with deep expertise in the solar power, airline, and pharmaceutical industries.

Expertise

PREVIOUSLY AT

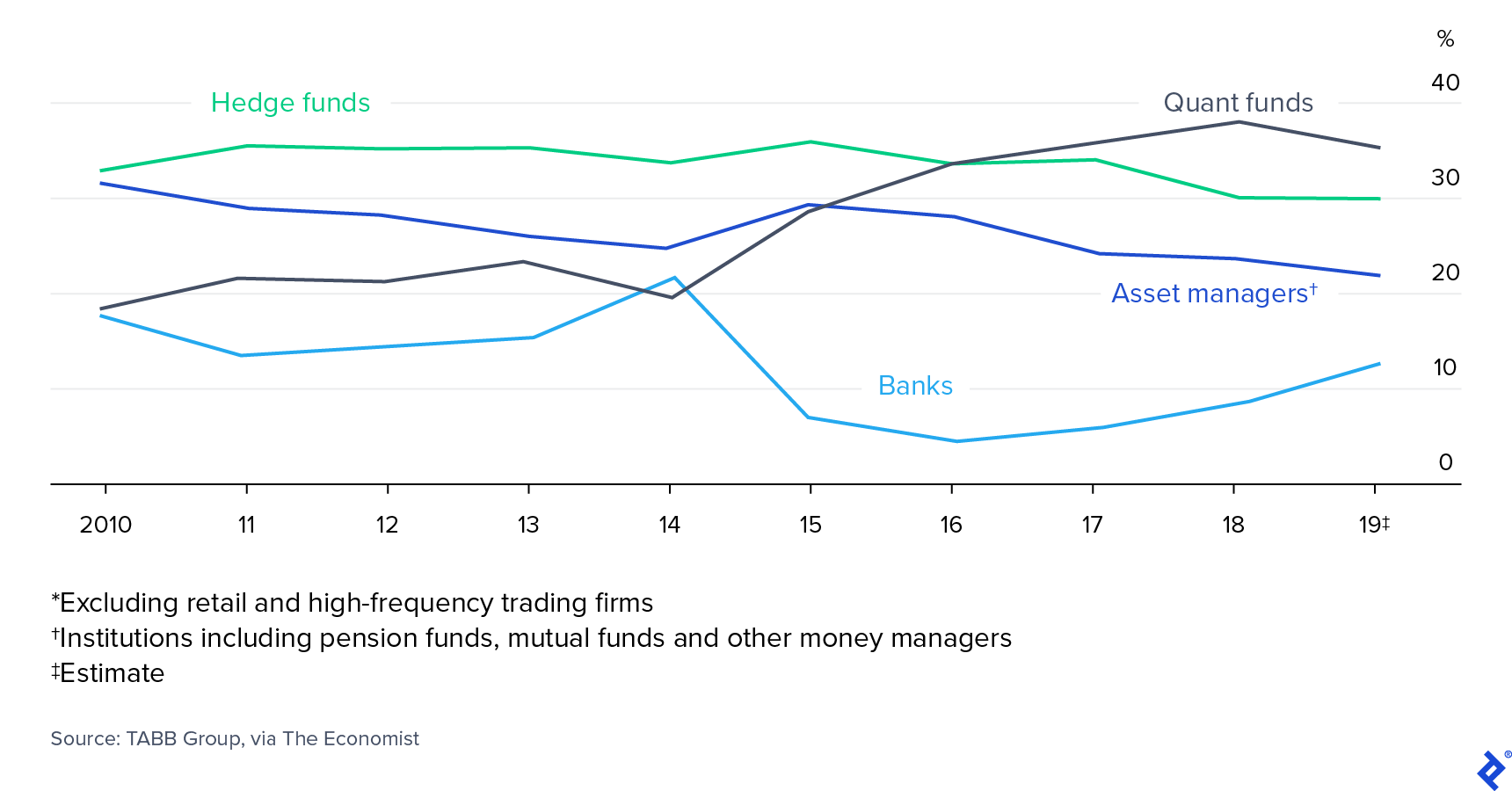

Robotic traders manage about $1 out of every $3. They are ubiquitous. You probably own a few index funds that are considered robotic or quantitative funds. They’re cheap and they provide access to the seemingly unstoppable stock market of late. But finally, the bubble may be bursting (at least for quant funds). Quant funds all over are shutting down (e.g., Columbia Threadneedle, Neuberger Berman). Trend-following quant funds saw some of the worst outflows in 13 years. So what are these quant funds exactly? Why did they come about? And is this dip a signal of an endemic problem with quants or simply a temporary reset?

Software’s Growing Influence on Investment Decisions

The wide field of finance, because of its access to capital, has long been the sector that tends to embrace technological innovations before other industries. So when software technology arrived in the 20th century, and algorithmic programs emerged, it was inevitable that the financial sector would be the first to harness the potential. John Bogle, the founder of Vanguard, launched the world’s first index funds in the 1970s, deploying software to track baskets of stocks and, thus, allow for a fund to deploy automatic reallocations in accordance with any changes in its underlying benchmark.

The advantage of using software to automate trading was profound, mostly in its effect on lowering operational costs. Index funds did not have to pay for the human resources that would have otherwise been harnessed to make selection and allocation decisions. The advent of the index fund was an important event in opening up the world of personal financial management to a mass market that would have been otherwise priced out of such a service.

Fast forward to the present day, and automated (quantitative) funds have, over the past decade, steadily moved upward to hold the highest share of volume by institutional trading on US stock exchanges.

ETFs: Index Funds Get Selective

Further developments in technology led to the introduction of quantitative Exchange Traded Funds (ETFs) toward the end of the 1980s. These instruments deployed software programs to make dynamic stock selection decisions based on certain factors. For example, an algorithm could be programmed to buy a stock when its market to book ratio falls below 1.0 and then to sell the same stock when the ratio rises above 1.5. As shown in this crude example, the software has been programmed to make systematic investment decisions based on fundamental analysis that would otherwise be done by human managers.

In the 30 years since the first ETF, the sophistication of automated trading has progressed to ever-advanced stages due to the rapid innovations in the field of artificial intelligence. Within the context of algorithmic software, the use of artificial intelligence implies that trading programs can learn and improve their effectiveness by their own volition. So, suppose that the software used in our ETF example above was deployed with an artificial intelligence module. Now, it may be able to continually analyze data on stock performance, allowing it to subsequently draw insight that a more profitable strategy would be to buy stocks only when their market to book ratio falls below 1.25 and sell them when the ratio rises to 1.8. The software will then start making decisions based on this learning, without the need for human intervention.

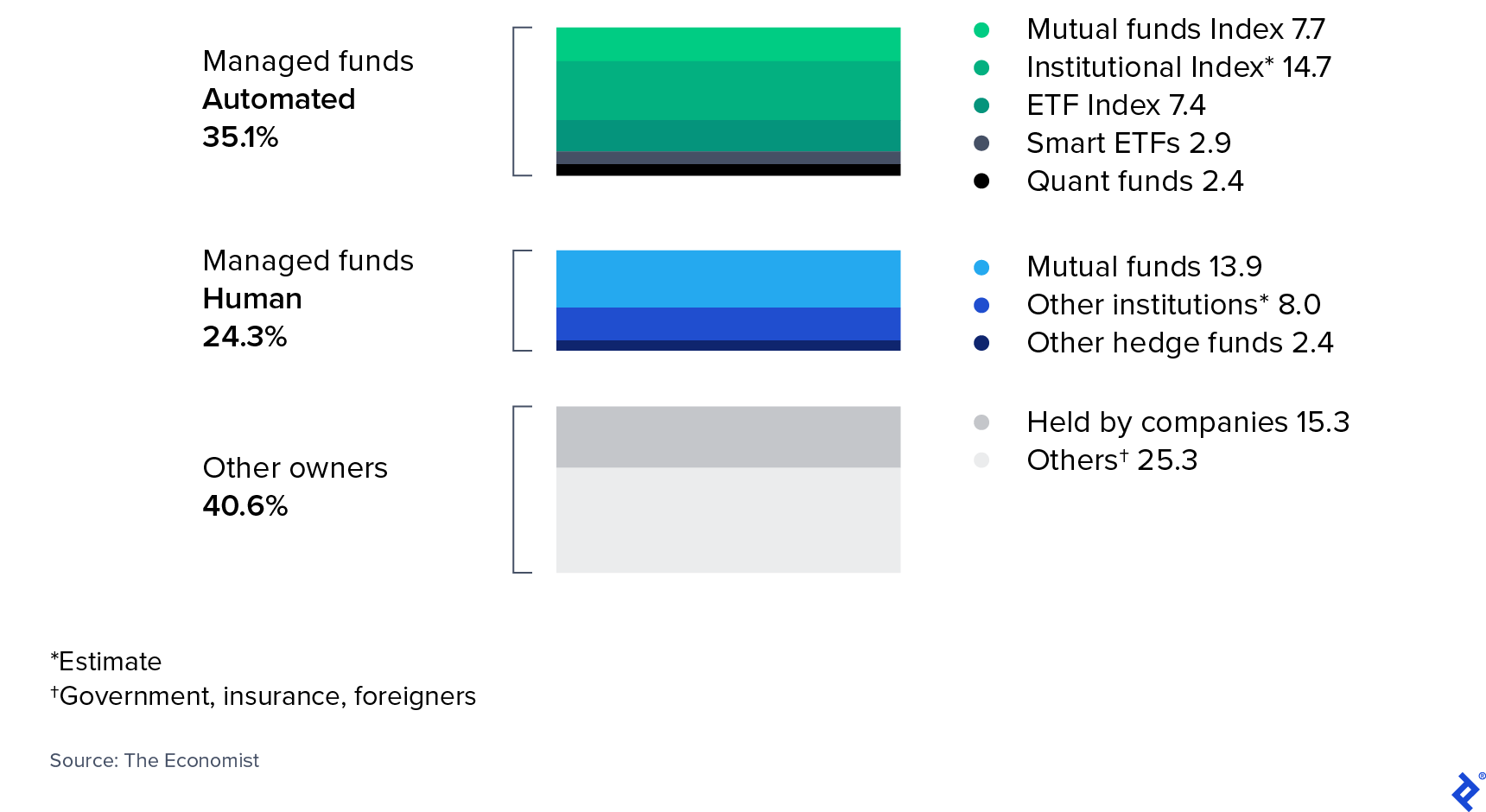

As of 2019, ETFs and index funds together manage more US equities than human-managed asset managers. Across the $31 trillion of US stock market value, quant funds now own 35.1% of market capitalization, compared to 24.3% of human-managed funds. This is a significant shift—but why does it matter?

Quants vs. Humans in Investment Management

Quant Pros

In what ways are quantitative funds a superior asset manager choice over their human counterparts? The most tangible way is through the low management fees afforded by quant funds, which cannot be matched by human-managed active funds. Efficiency on costs is one reason why we see Vanguard–the inventor of the index fund–ascend through the decades to reach the brink of being the world’s largest asset manager. Fees are essential in funds because, over time, they compound to be a significant cost burden for the investor and because—in the context of measuring performance—the higher the fees, the higher performance has to exceed the benchmark to justify them. Hedge funds, in particular, can encumber investors with fees of up to 20%, yet they underperformed over the past decade.

Another advantage of quant funds comes from their ability to draw insights by analyzing large amounts of data in real time. This might not necessarily be an advantage for future events, as noted by renowned fund manager Ray Dalio:

“If somebody discovers what you’ve discovered, not only is it worthless, but it becomes over-discounted, and it will produce losses. There is no guarantee that strategies that worked before will work again,” he says. A machine learning strategy that does not employ human logic is “bound to blow up eventually if it’s not accompanied by deep understanding.”

Quant funds can also make faster investment decisions than human managers. So they can place orders more quickly and exploit gains from narrow price differentials more effectively. They can be much more effective in implementing trading strategies than human managers due to their neutral bias and negated risk of fat-finger errors.

Quant Cons

And what are the drawbacks of quant funds? One negative is that with the increased usage of artificial intelligence, different quantitative funds may inevitably start making the same decisions in unison, which could bring about contagion issues for financial markets. One key advantage of human-driven fund management is the ability to detect idiosyncratic characteristics of a market and make decisions based on qualitative data. Quant funds cannot suck their thumbs, and as such, can contribute to increased volatility during periods of market stress.

How Are Quant Funds Measured Against Themselves?

The systematic objectivity of quantitative trading raises a question of how quant funds create differentiation from each other. How does a quant fund gain a competitive advantage over a rival? Human managers earn their stripes by demonstrating a better understanding of fundamentals, or through superior intuition, both factors developed through years of learning and proven objectively through bottom-line alpha.

Artificial intelligence-driven funds are premised on analyzing large amounts of data in real time and then deriving insights and subsequent investment decisions. This introduces new variables into ranking criteria, such as which fund has the fastest computing power, or petabytes of data access. The star coder may supersede the star trader as funds gain a competitive advantage from having a superior machine learning rule written by data scientists in the background.

The Need for Speed

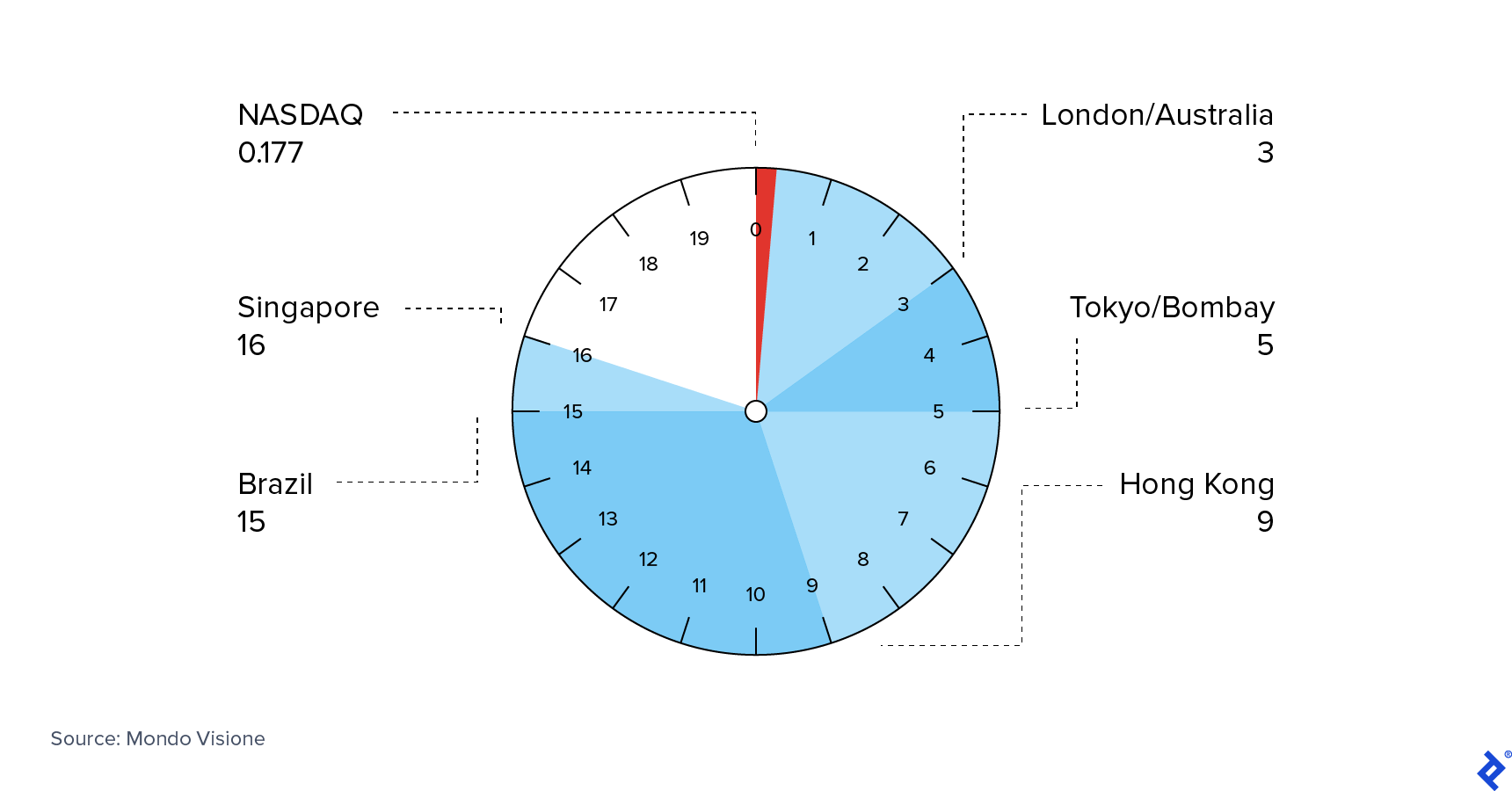

The quest among high-frequency trading (HFT) algorithmic funds to gain competitive advantage through faster trading has resulted in some of them creating their own private fiber optic or microwave networks to connect to stock exchanges. The theory being that laying the most perfect, straight line of cable will result in the most ultimate latent efficiency for sending orders to the exchange, putting the owner in a position of advantage compared to competitors using public utilities.

Just a couple of milliseconds can measure the advantage gained by owning a private fiber network. But these few milliseconds can result in differences of millions or billions of dollars in profits for HFT firms that are executing thousands of orders over a trading session. In his book Flash Boys, author Michael Lewis detailed the extent to which some traders went to realize the marginal gains of a private fiber optic line built between the Chicago and New York stock exchanges. The NASDAQ exchange in New York has the fastest execution time among the world’s major stock exchanges, which demonstrates the high stakes on offer for judicious traders looking to gain any advantage they can by being the first in line.

Yet, private fiber networks are costly to build. They require significant initial investment and can be hindered by physical barriers such as mountains. Microwave networks, however, serve the same purpose but with the advantage of higher speeds and fewer geographic hindrances due to their air-based transmission. In some markets, HFTs have already drawn battle lines in bids to own the most optimal microwave networks.

Some HFTs have even tried co-location, which refers to placing their trading software in systems located inside the stock exchanges they are trading on. This is, in some ways, the end game for the timing battle to get orders to an exchange. Many stock exchanges now offer co-location services, charging fees for providing space to traders to place their systems closer to the system of the exchange. But in the long term, the legality of these co-location services is likely to be challenged, raising ethical questions in a similar manner to the debate of net neutrality. Stock markets are, in their essence, market makers or marketplaces that bring buyers and sellers together without prejudice. A tiered system of beneficial access breaks down this relationship, which is a worrying predicament.

Even if an HFT has attempted to arm itself with all the advantages possible, there is no guarantee that it will always work. The case of Knight Capital will always serve as a reminder of this. Knight was one of the first HFTs to hit the market, but in 2012, its algorithmic software malfunctioned, and wrong trades to the tune of $7 billion were made over a period of just one hour. Correcting these erroneous trades cost the firm almost half a billion dollars and ultimately resulted in the fund having to liquidate and close down.

Will Robo-advisors Be the Revolutionary Application of AI in Finance?

That also brings us to the issue of personal wealth management. On a societal level, this could be the most significant area to look at, because a large part of the investments that go into equity funds are pooled capital investments of individual citizens (e.g., pensions).

Robo-advisors are software-driven investment advisors that direct clients based on algorithms. They have gradually come into prominence over the past decade. There is both promise and peril from removing human decision-making from financial advice. On the one hand, there is the chance to introduce vast swathes of the population to institutional concepts of financial planning and investment portfolio construction. Yet, on the other hand, some of the decision-making pillars of robo-advisory are quite arbitrary (i.e., own more bonds as you get older) and—while feasibly “correct” in a textbook sense—may fail to take into account the individual circumstances of the investor. The use of artificial intelligence will further empower robo-advisors as they begin to refine their allocation decisions based on their own learnings.

Is this an alarm bell for the human wealth manager? Will it significantly change the way wealth management is done in banks and other financial institutions providing wealth management services? When it comes to money and investments, leaving everything to software and technology is a risk that surely very few will take. At the end of the day, software, even if it has AI components, requires rules to function; and these rules can only be made by humans. Robo-advisors can make the wealth management process faster and more efficient. Still, perhaps the real winner in this battle will be the institution that manages to harness the advantages of both humans and machines working together.

Further Reading on the Toptal Blog:

- The Wealth of Nations: Investment Strategies of Sovereign Wealth Funds

- How to Understand and Appraise Private Real Estate Fund Investing

- Bridgewater's Ray Dalio: Quiet Pioneer of Big Data, Machine Learning, and Fintech

- All in the Family - A Guide to Family Offices

- Introduction to Deep Learning Trading in Hedge Funds

Understanding the basics

What is quantitative asset management?

Quantitative funds are investment management vehicles that employ software-driven decision-making as a core strategy. This can range from index funds tracking a benchmark to sophisticated algorithmic hedge funds.

Ankur Chandra

New Delhi, Delhi, India

Member since December 4, 2019

About the author

Ankur is an experienced financial modeler with deep expertise in the solar power, airline, and pharmaceutical industries.

Expertise

PREVIOUSLY AT