Crucial Considerations for Aspiring Fintech UX Designers

Designing fintech products requires more than great UX/UI skills—you need to understand finance too. Here’s what designers need to know to get started.

Designing fintech products requires more than great UX/UI skills—you need to understand finance too. Here’s what designers need to know to get started.

Gints is a fintech product designer with deep financial expertise and a decade of experience designing websites, trading platforms, dashboards, and mobile apps for fintech companies, banks, forex, and crypto trading companies around the world.

Expertise

Fintech is booming. Cryptocurrency has become an increasingly important part of the financial ecosystem, with the global crypto market reaching a record capitalization of nearly $4.3 trillion in late 2025. Digital banking adoption is also accelerating, with the number of customers estimated at 2.83 billion in 2026 and projected to reach 3.43 billion by 2030.

As fintech products grow in popularity, designers who understand finance and know how to protect users’ valuable assets will be in demand. Designers can’t stop people from making bad financial decisions, but when it comes to fintech products, designers can minimize usability issues and shield users from errors that may lead to financial harm.

For fintech, user research is essential: Nobody wants users to miss paying a bill or accidentally authorize a transaction because they are confused about what a button does. But for many fintech products, research alone is not enough to meet user and business needs. Finance is simply too complex to pick up through interviews and contextual inquiry—you must understand the mechanics in order to solve complex fintech design problems and partner effectively with your team.

Finance 101: Get Started

Fintech is an umbrella term for financial technology that encompasses consumer banking apps, complex back-end data analysis engines, and everything in between. For the purposes of this article, I’m going to focus on investing and three areas I’ve worked in myself: foreign exchange (forex), cryptocurrency, and neobanks.

If you don’t know where to start with these topics, Investopedia is a comprehensive clearinghouse of information on personal finance, cryptocurrency, and more. Additionally, many financial publications have free newsletters. The Wall Street Journal, The Economist, the Financial Times, Barron’s, Bloomberg, MarketWatch, CNBC, and Axios are popular in the English-speaking world.

However, to truly comprehend finance and fintech, you need to undertake further study. Here are my recommended starting points for common types of fintech and key financial topics:

Investing

Most online investment platforms are designed for buying and selling securities such as stocks and bonds through a broker on the stock market such as the New York Stock Exchange. Users of these platforms include those making occasional investments for college or retirement and day traders who make their living from it.

Learn more:

- Courses: Khan Academy’s free Finance and capital markets series

- Hands-on: Investopedia’s Stock Market Simulator and WallStreetSurvivor’s Stock Simulator

Forex

Forex involves buying and selling foreign currency to make a profit. The forex market is the biggest capital market in the world. There are no centralized markets for forex trading as there are for securities, so business hours do not matter.

Learn more:

- Courses: FX Academy

- Hands-on: Open a demo account with FxPro

Cryptocurrency

Cryptocurrency is a new type of asset that lives on the blockchain—a decentralized public ledger that is virtually impossible to forge or hack. There are thousands of cryptocurrencies available today, though the most popular ones are bitcoin and ethereum. Users buy and sell crypto on private exchanges and store it in digital “wallets.”

Learn more:

- Read online: Bitcoin and ethereum whitepapers (read bitcoin’s first), the Bitcoin Design Guide

- Hands-on: Axios’s crypto beginner’s guide (requires investment)

Neobanks

Neobanks, sometimes called challenger banks, are online-only. They typically offer a more limited range of services—such as basic checking, savings accounts, and ATM cards—and tend to have much lower fees than traditional banks, or none at all. Neobanks’ primary value proposition, after cost, is ease of use.

Learn more:

- Read online: These NerdWallet and Forbes articles, this Investopedia article on retail banking

Cross-border and Interbank Payments

Transferring funds between banks, particularly internationally, is a complex process that relies on an interbank transfer system to route the funds through intermediary banks to be processed. For international payments, there is an added layer of currency exchange. The most prominent such system is the global SWIFT system, but there are others, including the Eurozone’s SEPA. National interbank payment systems include US’s ACH, the UK’s Faster Payments, and Singapore’s FAST.

Learn more:

- Read online: The Bank of England’s overview of cross-border payments, the international payments chapter of Built for Mars’ Banking UX series

Financial Regulations

Any designer working on a fintech product should continually consult with legal counsel, but it’s still a good idea to have a grasp of common finance regulations. For example, understanding anti-money-laundering rules—which require certain fintech users to provide extensive documentation of their identity—will help you design user onboarding flows that fulfill legal requirements while minimizing user frustration. You should also understand your government’s deposit insurance program and relevant tax laws so you include appropriate warnings and disclosures.

Learn more: Every country has its own laws and rules. Government websites are the most authoritative, but not always the most user-friendly. If you need help finding a reputable resource, contact your local library.

Fintech UX/UI Project Needs

While every project is unique, fintech UX designers will encounter some common challenges.

Please note: I’m sharing these insights to help you understand the issues that you’ll need to think through—not to tell you the best way to solve a particular design problem. Work with your team’s finance and legal experts to ensure that your designs comply with all laws and regulations.

Onboarding

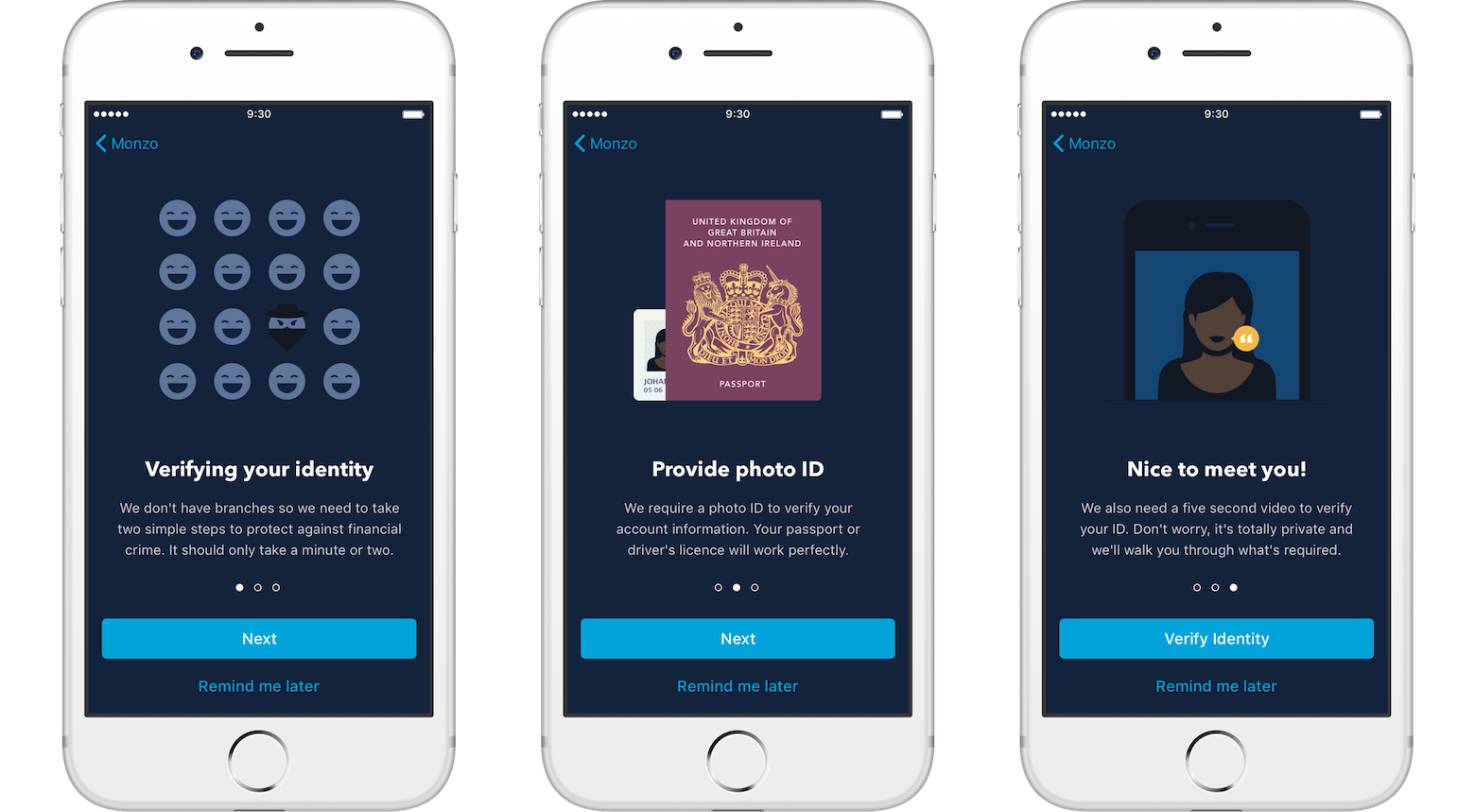

The law requires most financial services providers to verify users’ identities by having them fill out extensive know-your-customer forms. Doing so prevents identity theft, tax evasion, and money laundering. Some apps also make the user scan their official ID and take a video selfie while performing a specific task, such as turning their head or reciting a series of numbers, to prove that the photo in the ID belongs to the person opening the account. This verification is crucial in the age of photo editing and deepfakes.

To reduce the interaction cost of this process, particularly on mobile phones, it’s best to ask as few questions as possible. Work closely with your team’s legal counsel, as the legal requirements vary. For a crypto trading app, a user may be permitted to establish an account with minimal information (though they may be required to provide more information when they’re ready to start trading). For a neobank, however, the user may need to provide all their information upfront.

If the user must complete a long questionnaire, I keep it to about five questions per screen to ensure it feels manageable. I also try to minimize the amount of typing required by providing drop-downs for standardized responses. However, for legal reasons, it’s crucial not to push users to choose answers that are untrue or “close enough.” For example, if users are required to share their income, you will get more accurate results if you ask them to type in the exact number rather than choose from a list of ranges.

Test these flows rigorously to optimize them. If something goes wrong during onboarding, the user is likely to become frustrated or lose trust in the product and take their business elsewhere.

Deposits and Transfers

It’s difficult to design flows for online deposits and transfers without understanding how interbank transfers work. The user needs to collect and accurately input a lot of information, including account numbers, to ensure a successful transfer. Developing a user flow that minimizes mistakes is crucial. One way to protect the user from making an error is to require a “penny test” for the first deposit, which involves sending a very small amount of money to the recipient account to confirm that all the routing information is correct. Only then can the user send the full amount.

International transfers are even more complex. Depending on what country you’re in, you may not be allowed to send money to or receive money from certain countries. There may be limits on how much money you can transfer, and users in certain countries may not be allowed to make international transfers. All of these considerations must be built into your design so you don’t accidentally permit a user to do something illegal.

Trade Orders

Trading stocks, cryptocurrency, and foreign currency is drastically different than making an e-commerce purchase. The price of these assets fluctuates constantly during trading hours, so the price could change mid-transaction, leaving you with more or less than you intended to buy. Fees can also vary. Fintech companies account for this in different ways—some will freeze the cost for the user and then absorb the difference, while others don’t. In those cases, the user must be made aware that their purchase price is approximate.

AI-powered Features

Beyond these core flows, AI and machine learning are increasingly used throughout fintech products. Banking apps may automatically categorize transactions, generate predictive spending alerts, detect unusual account activity, or provide personalized financial insights. For designers, the challenge is communicating these recommendations clearly. Users need to understand why an alert or recommendation appeared and what to do about it.

Take a fraud alert as an example. If all a user sees is “Unusual activity detected,” they may not know how to respond. Designers should ensure notifications describe, in plain language, why something was flagged, such as an unfamiliar merchant or an amount outside the user’s typical spending range. That additional context helps users decide what to do next rather than simply reacting with confusion or alarm.

Whenever appropriate, give users a way to review, correct, or override AI-generated recommendations. Even when users can’t override a recommendation, they should understand the rationale behind it.

Overall Look and Feel

For fintech apps—especially for desktop products intended for prolonged use—a carefully considered dark mode palette doesn’t just look cool; it’s essential to well-being. A day trader could be looking at four monitors at once all day long, and most find dark mode is easier on the eyes. To design a great dark UI, you can’t just design in light mode first, then invert onto a dark gray background. For example, dark mode typically requires less-saturated versions of the colors you use in light mode.

While banking apps tend to have more traditional UIs, trading terminals have their own rules. For example, it’s not unusual to see dozens of columns of numbers rendered in eight-point fonts in order to pack as much detail onto the screen as possible. That’s not an accident—financial pros must pay attention to and react to an enormous amount of information that changes quickly, and the more that’s available in one glance, the better.

Keep in mind that it’s going to be difficult to find users who will test your product for a full, eight-hour workday, so be thoughtful and careful with these designs.

Ready to Start?

If you are ready to dive into the world of fintech, I recommend starting with a banking app because their transactions are more straightforward than crypto or forex trades. Plus, their UX will most likely be familiar to you, and their UI will follow best practices that are similar to e-commerce sites.

Once you’re committed to a career in fintech design, I recommend opening a real account or two and executing some trades of your own. This will put you in your user’s shoes better than anything else can. (Of course, only do this if you can afford to, and make sure you understand the risks and tax implications before you start.)

A critical piece of advice: Never take a fintech job that doesn’t have a lawyer or a financial expert on the team. Even if your contract protects you from legal liability, it’s still a terrible feeling to realize your work could have harmed someone.

The world of finance is fascinating, and so is the challenge of designing fintech UX. Gaining the competencies you need to do it well will take some effort, but if these concepts excite you, the results are worth it.

Understanding the basics

Good UX is often a defining feature of many fintech apps, particularly banking and investment apps, whose goal is to make finance less intimidating for non-experts.

Fintech is short for “financial technology,” and generally encompasses a vast suite of digital tools that facilitate financial analysis and transactions. When we say “fintech,” we usually mean online banking, investing, and trading assets like forex and cryptocurrency.

Fintech has helped democratize finance by putting once-exclusive tools into the hands of everyday users. Banking and investing are easier than ever, while forex and crypto trading would be impossible without these tools.

Barcelona, Spain

Member since February 24, 2020

About the author

Gints is a fintech product designer with deep financial expertise and a decade of experience designing websites, trading platforms, dashboards, and mobile apps for fintech companies, banks, forex, and crypto trading companies around the world.