2017 Holiday Spending Forecast: Will Be Better Than Expected

Retail investors have had a rough year. The SPDR S&P Retail ETF has underperformed the S&P 500 by nearly 30 percentage points. From eCommerce shifts to higher gas prices, there are plenty of arguments to be made against retail. Yet, there are a couple reasons to be jolly heading into the holiday season that few are talking about.

In this article, Elizabeth Hanano, CFA suggests that low expectations combined with lesser-known tailwinds indicate it may be time to dip a toe back into the retail pond.

Retail investors have had a rough year. The SPDR S&P Retail ETF has underperformed the S&P 500 by nearly 30 percentage points. From eCommerce shifts to higher gas prices, there are plenty of arguments to be made against retail. Yet, there are a couple reasons to be jolly heading into the holiday season that few are talking about.

In this article, Elizabeth Hanano, CFA suggests that low expectations combined with lesser-known tailwinds indicate it may be time to dip a toe back into the retail pond.

Elizabeth began her career as an equity analyst and brings a deep understanding of how to unlock value within companies, big and small.

Previously At

Executive Summary

Retail investors have had a tough year.

- The S&P Retail ETF (exchange-traded fund) has declined nearly 10% in the past twelve months versus the S&P 500 up 19%. That’s nearly 30 percentage points of underperformance.

- It’s fair to say that investor hatred of retail has gone to a dark place when once-loved stocks like Macy’s are trading at less than half that of the S&P 500 (7x next twelve months earnings versus the S&P 500 at 18x).

Why has retail been so bad and why do people expect a weak holiday?

- Of course, the big driver is Amazon and the push towards eCommerce. Amazon has their hands in everything and they don’t care about near-term profitability.

- There are many other reasons to be negative on retail: higher gas prices, iPhone X super cycle, rising shipping costs, the millennial-driven shift from buying "stuff" to buying experiences (vacations, fine dining), and more.

- The Wall Street Journal recently wrote, "It’s understandable that investors think this holiday season, when November and December count for about a quarter of department stores’ annual sales, will be another miserable one."

Why might retail be better than expected?

- While there is no doubt that the changing paradigm brought on largely by the shift to eCommerce is real, retailers are not going out of existence tomorrow and there are some mitigating factors.

- There are a few positive factors that should benefit retailers this holiday season that aren’t getting a lot of attention. These include: recently positive chatter from retailers, cooler weather, low inventories, favorable calendar elements, a positive macro backdrop, upbeat surveys, and easy comparisons.

Who survives?

- The retail landscape will continue to be difficult for those who fail to move with the times.

- However, the retailers who have (1) a desirable product/defensive brand, (2) a solid omnichannel strategy, and (3) well-controlled inventories should fare pretty well this season in light of an overall favorable background. As always, it’s a matter of bifurcating the winners and losers - not all retail will succeed.

Last year’s holiday season left retailer investors with not much more than coal in their stockings. Even after the holidays and throughout the year, Santa seemed to forgo his hibernation period, dropping leftover bits of coal in retail investors’ stockings. No specific retail sector has been safe. Previously defensive stocks like Walgreens and CVS have been thrown to the wolves (Walgreens -14% and CVS -10% year-to-date). Grocers like Kroger (down nearly 40% YTD) and meal kit services like once-splashy IPO Blue Apron (down nearly 70% YTD), are crying “uncle.” Of course, traditional retailers like Macy’s (-44%), Dick’s (-49%) and J.C. Penney (-62%) haven’t escaped the pain either. Year-to-date, auto parts retailers like Advance Auto Parts and Auto Zone have declined 52% and 24%, respectively. Even life sciences companies like Thermo Fisher Scientific are not immune as Amazon looks to enter the lab supplies business (-8% since the rumors started).

The S&P Retail ETF (ticker: XRT) has declined nearly 10% in the past twelve months versus the S&P 500 (up 19%). That’s nearly 30 percentage points of underperformance. Few sectors have seen a chart so ugly:

So what’s been the cause and why are investors still positioned so negatively heading into the holiday shopping season? There are so many things going against retail’s favor. Here’s a quick, fun list:

- The shift to online hurts traditional retailers as shoppers can easily compare prices of branded goods. Shoppers can also shop whenever they want, with no sense of urgency from previous surge days like Black Friday.

- eCommerce is not only cannibalizing store traffic and four-wall margins but also forcing retailers to invest in omnichannel capabilities—a double hit to profitability.

- The largest competitor, Amazon, has an unparalleled and convenient distribution chain and doesn’t care about making a near-term profit.

- Year-to-date, gas prices are up 13% y/y, possibly limiting discretionary spending.

- The iPhone X super cycle may take wallet share.

- Shipping costs are rising.

- The shift from buying “stuff” to buying experiences (vacations, fine dining).

It’s fair to say that investor hatred of retail has gone to a dark place when once-loved stocks like Macy’s are trading at less than half that of the S&P 500 (7x next twelve months earnings versus the S&P 500 at 18x). The Wall Street Journal recently wrote, “It’s understandable that investors think this holiday season, when November and December count for about a quarter of department stores’ annual sales, will be another miserable one.”

Of course, the big driver is Amazon and the push towards eCommerce. Amazon has their grubby hands in everything (even pharma and groceries now) and they don’t care about near-term profitability. Nevertheless, while there is no doubt that this is a serious concern, non-Amazon retailers are not going out of existence tomorrow. People still want to shop somewhere that has a brick-and-mortar store. Even Amazon is joining the brick-and-mortar party.

Additionally, there are a few positive factors that should benefit retailers’ holiday sales 2017 that aren’t getting a lot of attention. These include:

- Recently positive chatter from retailers

- Cooler weather

- Low inventories

- Favorable calendar elements

- Positive macro backdrop

- Upbeat surveys

- Easy comparisons

So the retailers who have (1) desirable product, (2) a solid omnichannel strategy, and (3) well-controlled inventories should fare pretty well this season in light of an overall favorable background. As always, it’s a matter of bifurcating the winners and losers—not all retail will succeed.

Given the wild exogenous events that seem almost more predictable than not these days (hurricanes, wildfires, political landscapes on par with Game of Thrones), retail forecasting can be tough to do with much certainty. But let’s take a look at the information we do have today and see what we should expect.

Why We’re in for a (Somewhat) Jolly Christmas

1. Recently Positive Commentary

Before trend changes manifest themselves in numbers, they happen at the ground floor—at a level where people are just beginning to talk.

A handful of retailers reported third-quarter earnings in early to mid-November with surprisingly positive commentary. Department stores have been some of the hardest-hit retailers from Amazon given their high fixed costs (shift to online hurts 4-wall margins) and easily price checked branded items. Yet, both Kohl’s and Macy’s noted that they saw business pick up in the back half of October after the negative impacts of hurricanes and unusually warm weather lessened. Kohl’s noted, “We’re super confident as we go into the fourth quarter.” Ross beat both sales and earnings forecasts and raised its forecast for the fourth quarter.

On its earnings call, Target seemed more upbeat on Holiday Sales 2017 than they had been in a while, “While Q4 is always intensely competitive, we are entering this holiday season with lots of confidence.” From its earnings call last week, it was clear that Walmart was seeing improved traction as well. Walmart’s domestic comparable-store sales increased 3%; even foot traffic was up and they noted “good momentum in sales growth across the business.

Additionally, many states noted an improvement in the October Beige Book: “All responding retailers reported that sales improved over the last six weeks. Whereas previous reports sometimes cited flat or negative year-over-year results, contacts this round reported year-over-year comparable store gains in the 2 percent to 4 percent range. Consumers reportedly spent on clothing, furniture, and home improvement items. Contacts were generally optimistic that the recent positive sales trend would continue through the end of the year”

2. Cooler Weather Bodes Well for Multiple Retail Sectors

Year-to-date, the weather has not been cooperating. According to the National Centers for Environmental Information, the October national average was 55.7°F, 1.6°F above the 20th-century average, and in the warmest third of the historical record.

Following last year’s unseasonably warm winter, the U.S. appears to be set up for a cold burst this holiday season. The National Science Foundation recently forecast an exceptionally cold winter with a polar vortex expected to return. Even if temperatures are modestly lower versus last year, this should help seasonal categories and auto parts retailers as there is likely pent-up demand from lack of purchases last year. Cooler weather provides an impetus for shoppers to get new items, whether it be apparel to keep warm or new auto parts that get worn out more easily in harsh weather.

Weather Trends International (WTI) also forecasts a relatively positive retail scenario for this holiday spending season with November expected to be significantly cooler y/y. Already, the first week of November was significantly cooler versus the prior two years and marked the snowiest start to the month in six years. The second week of November was also cooler year-over-year with the Northeast receiving an arctic blast and minimal precipitation—a favorable setup for shopping for seasonal winter categories. Retailers already appear to be feeling the benefit as Macy’s noted in mid-November at the Morgan Stanley Global Consumer & Retail Conference, “Obviously a few weeks does not make a fourth quarter, but this weather is clearly quite positive for the business.”

3. Inventory Levels Are Low

Given declining foot traffic and in an effort to avoid last year’s overstocked inventory situation, many retailers are being extremely cautious on inventory heading into the holiday season with some still in the process of placing new orders. According to dozens of sources that spoke to Reuters, this includes Macy’s, J.C. Penney, Kohl’s, Nordstrom, Dillard’s, and Hudson Bay’s Lord & Taylor, among others.

Recent earnings calls echo this message as many have reported very clean inventories and noted that they are managing inventory for the back half very cautiously. This should bode well for markdowns and gross margins as retailers will be less likely to slash prices to move excess inventory. According to Morgan Stanley, inventory coming out of 2Q was 210 basis points below 3Q expected revenue growth—a clear indication that inventory levels are in good shape. J.C. Penney was one of the most significant clearers of inventory as they took aggressive actions mid-quarter to clear stagnant inventory to make room for an “improved apparel assortment heading into the holiday season” according to CEO Marvin Ellison.

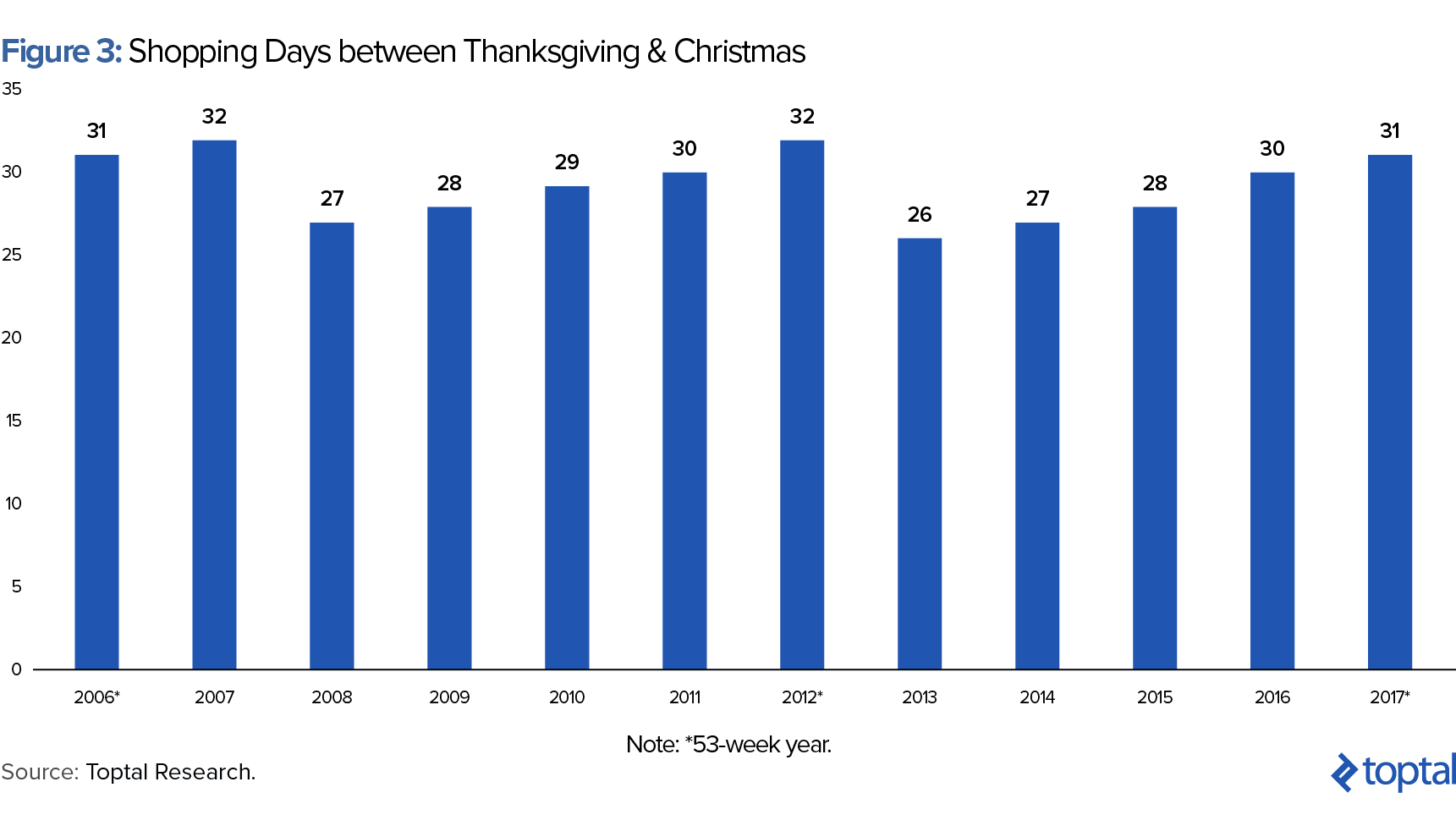

4. 2017 Holiday Calendar Shifts Are Favorable

-

Sheer number of shopping days is higher. In 2017, we will see one additional shopping day between Thanksgiving and Christmas (31 days versus 30 last year). Fewer shopping days tends to put more pressure on retailers to promote early and turn up the volume as Christmas approaches. While clearly some retailers still started their promotions early according to Abha Bhattarai of the Washington Post, a more forgiving calendar relieves some of the pressure to promote early and deep.

- Day of the week for Christmas is favorable. In 2017, Christmas will fall on a Monday versus a Sunday last year. This means an extra weekend day for shopping which will boost brick-and-mortar but not eCommerce as UPS and FedEx don’t deliver on Sundays.

- Lots of Saturdays in December. For the first time since 2012, there will be four Saturdays in December before Christmas Day. According to ShopperTrak, Saturdays in December are some of the busiest shopping days all year and they get busier week-over-week leading up to Christmas Day.

- The 53rd week. Every five years, retailers have a 53rd week in January. An entire extra week is a pretty big deal and can add 4-5% incremental revenue growth. While investors are supposed to take this into account, headline numbers can do a lot for momentum and sentiment. Since the XRT Retail ETF has been available, a 53rd week has occurred twice and, in both instances, the XRT outperformed the S&P 500 index by about 300 basis points from the beginning of the fourth quarter through the end of the first quarter.

5. Macro Factors Bode Well

Consumer confidence in October increased to its highest level since 2004. Director of Economic Indicators at The Conference Board, Lynn Franco, noted, “Consumers’ assessment of current conditions improved, boosted by the job market, which had not received such favorable ratings since the summer of 2001. Consumers were also considerably more upbeat about the short-term outlook, with the prospect of improving business conditions as the primary driver. Confidence remains high among consumers, and their expectations suggest the economy will continue expanding at a solid pace for the remainder of the year.” While consumer confidence recently has not been as highly correlated with retail sales as in the past, this has been attributed to low inflation and high savings rates. However, as shown in Figures 5 and 6, CPI has begun to tick up while the savings rates have steadily declined.

Disposable personal income last year grew 2% over the holiday spending season and, according to Deloitte, may rise to a range of 3.8% to 4.2% this season. Clearly, the more disposable income shoppers have, the better.

Furthermore, gas prices, while about 19% higher year-over-year (week of 11/6/17) at $2.56 remain extremely low relative to historical levels of $3.01 (2012-2016 average). Additionally, gas prices year-to-date through August, before Hurricane Irma and Hurricane Harvey hit, were running just 10% higher year-over-year and are expected to trend lower going forward.

6. Easy Comparisons

I really hate to talk about “easy comps”—an industry term that empirically feels meaningless. However, easier comps, for better or worse, tend to drive stocks. An unexpected acceleration in revenue (even when caused, in part, by easier comparisons) indicates an improving environment and this tends to lead to higher earnings estimates, higher valuations, and, therefore, higher stock prices. Psychologically, an investor seeing a company grow comparable store sales 10% may place a higher multiple on that stock versus a company that puts up 5% growth even if it’s simply a matter of easier y/y comparisons.

In this light, it’s important to note that last year’s holiday season was a nightmare for most retailers, and this means that year-over-year comparisons will be quite easy. Last year, comps decelerated from up 0.5% in 1Q16 to near flat in 2Q, to down 0.8% in 3Q and then down 1.1% in 4Q16 and down 2.3% in 1Q17 as the holiday hangover persisted (analysis based on Toptal Research of XRT ETF stocks excluding eCommerce only companies and including only companies with fiscal years ending December or January). Some fared even worse—Express’s comps declined 13% and Macy’s declined 5% y/y,

Last year, the start of the season coincided with the U.S. presidential election and shoppers seemed more apt to stay home and watch Trump and Hillary throw side eye at each other than to shop. Furthermore, retailers entered the season with bloated inventories which combined with a reticent shopper and an unseasonably warm winter, led to a pretty dismal performance. In fact, foot traffic declined 12% y/y, according to eMarketer, in November and December and retail stocks significantly underperformed as the S&P Retail ETF declined 3% versus the S&P 500 up 9% from the end of 3Q16 to the end of 1Q17.

7. Surveys Are Positive

Surveys and forecasts from the major retail agencies are relatively optimistic about the holiday season with all predicting revenue growth to increase about 4%, an acceleration versus last year’s +3.6%.

The National Retail Federation forecasts retail sales in November and December (including eCommerce and excluding automobiles, gasoline, and restaurants) will increase between 3.6% and 4.0% to $679 billion in 2017. This indicates growth will meet or exceed last year’s +3.6% and the five-year average of +3.5%. NRF Chief Economist Jack Kleinhenz notes, “Consumers continue to do the heavy lifting in supporting our economy, and all the fundamentals are aligned for them to continue doing so during the holidays…The combination of job creation, improved wages, tame inflation and an increase in net worth all provide the capacity and confidence to spend.”

NRF’s survey conducted in October found that only 27% of consumers believe their holiday spending will be impacted by concerns regarding the economy. This is down from 32% last year and is the lowest level since the NRF began asking the question during the Great Recession of 2009.

Deloitte, whose forecast is the most optimistic at 4.0-4.5%, believes four factors will drive the strong uptick: personal income growth, consumer confidence, strong labor market, and a low, stable personal savings rate. ICSC forecasts retail sales increase 3.8% y/y and believes that consumers are “very optimistic this holiday season and that physical retail remains a cornerstone of the holiday season.” ICSC excludes non-store vendors.

While some are predicting that Black Friday is dead, RetailMeNot’s survey of over 1,000 people found that the desire to shop the day after Thanksgiving remains about flat with 52% of respondents planning to shop on Black Friday versus 53% last year. As for Cyber Monday, the demand is increasing. Cyber Monday is the Monday after Thanksgiving and has seen increasing popularity as shoppers participate in easy-access, online deals. Last year, Cyber Monday hit a new all-time record as the largest online sales day with sales up 10% year-over-year, according to Adobe Digital Insights. For 2017, Adobe forecasts Cyber Monday sales will increase a whopping 16.5% to $6.6 billion.

Parting Thoughts

By no means should we expect a retail renaissance this holiday season. However, given some of the positive factors that retailers have at their backs, there’s reason to have hope that those with desirable product/defensive brand (e.g., Canada Goose)/eCommerce insulated model (e.g., off-price), a competitive omnichannel strategy, and clean inventories are set up for a pretty solid holiday shopping season. The combination of miserable sentiment and not-bad results has often proved itself to be a good time to invest. On November 9th, Macy’s reported its 11th consecutive same-store sales decline, sales were down more than consensus, but they beat on earnings and had clean inventories. Stock reaction to these so-so results? Up 11%. On November 14th, Advance Auto Parts reported a slight miss on comparable store sales but beat on earnings due to strong margins. The mixed quarter led to the stock being up 20%. With expectations this low and relative valuations in the dumps, it doesn’t take much to please a retail investor.

Disclosure: The views expressed in the article are purely those of the author. The author has not received and will not receive direct or indirect compensation in exchange for expressing specific recommendations or views in this report. Research should not be used or relied upon as investment advice.

The author has no investments or business relationships with any of the companies mentioned in this article.

Understanding the basics

The retail calendar is divided into 52 weeks of seven days, a total of 364 days. This leaves an extra day at the end of each year which culminates in an extra week being added to certain years. This occurs every five or six years. The last time this happened was in 2000, 2006, 2012 and it will occur in 2017.

An omnichannel brand serves its customer through multiple, well-integrated channels. This allows a customer to seamlessly move between modes of shopping like eCommerce, mobile, and brick-and-mortar. Many customers begin in one channel and move to others as they research and move through the buying cycle.

“Black Friday” is the name given to the day after Thanksgiving. Initially, the term Black Friday was created to describe the mayhem and congestion that ensued on this day. Retailers didn’t like this connotation and changed the meaning to reflect accountants’ terminology for profit, “in the black.”

Elizabeth J. Howell Hanano, CFA

Annapolis, MD, United States

Member since October 3, 2017

About the author

Elizabeth began her career as an equity analyst and brings a deep understanding of how to unlock value within companies, big and small.

PREVIOUSLY AT