Latin America M&A Best Practices

Latin America boasts great investment opportunities with attractive risk levels, higher returns than home markets, and access to a large population base with growing income. However, Latin American acquisitions require special attention and include a number of difficulties unique to the region.

This article provides insights gleaned from Management Consultant Emilio Labrador’s 15 years of experience in Latin American oil and gas M&A. It provides practical tips for foreign acquirers considering investments in Latin America, on topics ranging from risk premiums in valuation, accounting due diligence, and legal considerations.

Latin America boasts great investment opportunities with attractive risk levels, higher returns than home markets, and access to a large population base with growing income. However, Latin American acquisitions require special attention and include a number of difficulties unique to the region.

This article provides insights gleaned from Management Consultant Emilio Labrador’s 15 years of experience in Latin American oil and gas M&A. It provides practical tips for foreign acquirers considering investments in Latin America, on topics ranging from risk premiums in valuation, accounting due diligence, and legal considerations.

Emilio has 25 years of CFO experience in Europe and LatAm. An expert in M&A, he has executed two $300m+ acquisitions and a $400m+ disposal.

Expertise

Previously At

Executive Summary

Difficulties When Evaluating Acquisitions in Latin America

- Access to Accurate Information Is a Challenge. Despite progress with information access, transparency remains limited, with fragmented information making decision-making difficult. Generally speaking, in all of Latin America, property titles are public but availability is an issue, public credit rating of companies is not easy to obtain, company accounts are an issue to obtain too, and other difficulties abound, including permits, sales by sector, labor, business environment, etc.

- Intense Bureaucracy Can Reduce Efficiency. Processes, governance, and controls can be manual and inefficient, which can slow down acquisition progress and even discourage customers or decrease employee morale for target companies. Due to increasingly stringent anti-corruption regulations, government decision-making can be protracted since public servants are fearful of breaking these complex laws. On a similar note, red tape and compliance with government requirements are notoriously burdensome. According to a recent global study conducted by the TMF Group, Brazil was rated the most financially complex jurisdiction in the Americas and second in the world due to its 90+ taxes, duties, and contributions as well as aggressive federal tax enforcement via SPED, its digital bookkeeping system.

- Language and Cultural Differences. A lot can be lost in translation between the acquisition target employees and foreign managers sent to a Latin American company for due diligence or to run the acquired operation. Since cultural differences can serve as unforeseen obstacles, the transition period after an acquisition is a sensitive time, especially if the acquired operation is a formerly family-run business.

Special Considerations When Valuing a Latin American M&A

- Consider Incorporating a Risk Premium. Valuation methods utilized in Latin America might incorporate a country risk premium in the valuation to reflect the incertitude of the particular country. When the discount rate increases, the calculated acquisition price decreases. The DCF discount rate might be increased based on items such as the country's risk, history of contract enforcement, changes in tax rates, and legal stability.

- Due Diligence – Accounting and Financials. Beware of audited financial statements; locally-audited financial statements can be unreliable and should be verified. When the deal is structured as base consideration plus working capital consideration, exclude non-value items from working capital not adequately provided for in the financial statements. And lastly, make sure that local currency can be converted into USD and funds can be remitted offshore easily. If conversion or offshore remittance isn't possible, your investment might be lost.

- Due Diligence – Taxes. Always consider whether tax rates are constantly changed, whether deductions in tax law are accepted by the tax authority, whether the authorities effectively reimburse tax credits, whether tax audit risks are reflected in company accounts, and whether dividend repatriation has been accounted for.

- Due Diligence – Human Resources. It's important to understand the impact of trade unions' negotiation power in the country and in the acquired company. In some cases, trade unions are so powerful that they jeopardize operations by paralyzing the company with strikes or simply making life difficult for company leadership. It's also crucial to determine whether salaries are automatically adjusted to the foreign exchange USD variation with respect to local currency and if salaries are paid in local currency or in USD. If the target company revenues are based in USD, it would make sense to tie local salaries to USD. If not, local currency is preferable.

- Due Diligence – Legal. Always consider bribery and anti-corruption investigations, corporate governance among partners, foreign exchange variation in contracts, enforceability of client contracts, the possibility of a bilateral investment treaty between acquirer and acquisition countries, and avoidance—if possible—of litigation in courts.

Integration Planning

- Effective integration planning needs to be established as early as possible. Due diligence and integration actions can be prepared simultaneously. In fact, it's ideal if the experts participating in the due diligence process are also the ones conducting the integration planning. Effective integration planning includes everything from integrating IT and identifying key sources of value to choosing and cultivating one company culture, to carefully selecting leadership. Ideally, new management will include those who understand the local culture and language and can keep up morale among legacy employees.

Why Latin America M&A Best Practices Are Important

- Latin America boasts great investment opportunities with attractive risk levels, higher returns than home markets, and access to a large population base with growing income.

- Foreign investors are no longer pursuing deals in Latin America because of a dearth of investment opportunity in their home country—now, it's because the region is experiencing rapid consumer growth, urbanization, and digitization. In fact, returns from Latin American investments as measured by the MSCI Emerging Markets Index have long outperformed returns from emerging markets as a whole.

- However, Latin American acquisitions do require special attention and come with a number of difficulties unique to the region.

Introduction

Latin America boasts great investment opportunities with attractive risk levels, higher returns than home markets, and access to a large population base with growing income. Foreign investors are no longer pursuing deals in Latin America because of a dearth of investment opportunity in their home country—now, it’s because the region is experiencing rapid consumer growth, urbanization, and digitization. In fact, returns from Latin American investments as measured by the MSCI Emerging Markets Index have long outperformed returns from emerging markets as a whole. However, Latin American acquisitions do require special attention and come with a number of difficulties unique to the region.

This article provides insights gleaned from over 15 years of my own experience in Latin America oil and gas M&A. The acquisitions were worth an average of $250 million and were based in countries ranging from Peru, Brazil, Guatemala, Venezuela, and Ecuador to Trinidad, Mexico, and Colombia. Below, you will find practical tips for foreign acquirers considering investments in Latin America. It is my hope that reading this article can help readers prevent or navigate a potential misstep.

Difficulties When Evaluating Acquisitions in Latin America

Let’s begin with some potential difficulties encountered within the region, including access to accurate information, bureaucracy, and cultural differences. Many of these issues stem from the fact that Latin America is still an emerging market and there are associated issues with national governance, social instability, and risk of fiscal crises such as the Latin American debt crisis of the 1980s.

Access to Accurate Information Is a Challenge

In recent years, the Latin American region has made progress with regards to information access, including the enacting of the Freedom of Information Act (FOIA) in 65% of LatAm countries. Since FOIA was enacted, countries have also been building infrastructure for managing information requests, with the Mexican and Chilean electronic platforms as models of doing so. The Mexican platform Infomex allows citizens to place information requests to federal and local agencies through this one platform.

However, transparency remains limited, with fragmented information making decision-making difficult. Generally speaking, in all of Latin America, property titles are public but availability is an issue, public credit rating of companies is not easy to obtain, and company accounts are an issue to obtain too, as are land and permits, sales by sector, labor, business environment, etc.

Intense Bureaucracy Can Reduce Efficiency

Processes, governance, and controls can be manual and inefficient, which can slow down acquisition progress and even discourage customers or decrease employee morale for target companies. For example, official government responses and negotiation with public servants can drag if there is no political will to accelerate progress. Due to increasingly stringent anti-corruption regulations, government decision-making can be protracted since public servants are fearful of breaking these complex laws.

Once, in Ecuador, I acted as a representative of a company looking to strike new licensing contracts with national oil company Petroamazonas. However, even the simplest of clauses (terms of payment, unit service prices, etc.) could not be agreed upon. The public servants exhibited strong hesitance to take the risk of agreeing to the most minimal of details. This reluctance eventually meant that the contracts were not signed with Petroamazonas and the projected increase in oil production was not achieved. Below is a chart from the World Bank Group indicating the relative ease of running and doing business in a country while complying with relevant regulations.

On a similar note, red tape and compliance with government requirements are notoriously burdensome, especially where tax, legal matters, permits, and environmental regulations are concerned. Operations might even be halted due to compliance issues. Once, we suffered in Peru when an oil company I was representing experienced delayed commencement of drilling for over three years because it required approvals from 15 Peruvian environmental regulatory government agencies. While these compliance requirements certainly improve safety and sustainability, they are often inflexible and difficult to navigate. According to a recent global study conducted by the TMF Group, Brazil was rated the most financially complex jurisdiction in the Americas and second in the world due to its 90+ taxes, duties, and contributions based on different federal, state and municipal taxes, as well as aggressive federal tax enforcement via SPED, its digital bookkeeping system. Similarly, Colombia is ranked as the second most complex in the Americas and sixth in the world. Colombia’s most recent tax reform of 2016 introduced a new withholding tax on dividends, increased the corporate tax rate, eliminated the income tax for equality, and added new measures to prevent tax evasion and tax avoidance. Colombian GAAP also transitioned to IFRS, which also adds to the complexity.

Language and Cultural Differences

A lot can be lost in translation between the acquisition target employees and foreign managers sent to a Latin American company for due diligence or to run the acquired operation. For example, in Guatemala, a general manager sent from US headquarters perpetuated severe miscommunication issues and eventually laid off the original legal representative in a combative manner. The former legal representative ended up pursuing multi-million-dollar litigation claims against the acquired company, which endangered operations for the following three years. I was appointed legal representative of the Guatemalan subsidiary and managed to resolve these claims by reaching an amicable settlement with the previous legal representative for 1% of the total claimed amount. Since cultural differences can serve as unforeseen obstacles, the transition period after an acquisition is a sensitive time, especially if the acquired operation is a formerly family-run business.

Special Considerations When Valuing a Latin American M&A

In Valuation, Consider Incorporating a Risk Premium

Valuation methods utilized in Latin America M&A, including DCF, multiples on sales, and EBITDA multiples might need to incorporate a country risk premium in the valuation to reflect the incertitude of the particular country. When the discount rate increases, the calculated acquisition price decreases. It’s important to note that different countries within the region have unique attributes and their associated discount rates need to be adapted accordingly.

The DCF discount rate might be increased based on items such as the country’s risk, history of contract enforcement, changes in tax rates, and legal stability. It’s possible that the risk perception of the country is outweighed by the target country’s higher returns and the buyer might decide against penalizing the Latin American acquisition. Thus, it is recommended that a valuation expert make a checklist and weight each parameter of risk and positive competitive advantages of entering the country and assign an overall discount/premium to the Latin-American acquisition compared to home markets. The input for this valuation should derive from experts in their respective functions (operations, finance, tax, etc.) to determine the ultimate discount/premium. The overall risk perception and the final decision of the adjusted DCF discount rate also needs to have strong management support. The biggest concerns when investing in Latin America are indicated below, from a recent World Economic Forum study. Of course, however, Latin American countries each have their own idiosyncrasies and risks must be evaluated country by country.

For example, we were once evaluating Peru as a target country for an acquisition. The parent company used a 10% base rate to discount future cash flows generated by the target acquisition, political instability added 2%, and non-enforceability of contracts added 1%. We are at a 13% discount rate with respect to an acquisition in the home country. The risk of tax rate changes added 2.5% and the difficulty of managing operations in Peru added 2%, yielding a discount rate of 18%. However, management of the acquirer company evaluated that the high growth prospects of the Peruvian market deserved a reduction in the discount rate of 9%. Thus, the final discount rate of the acquisition to be applied would be 8.5%.

Multiples on sales and EBITDA multiples adjusted to different target countries’ acquisitions can follow the same logic to adjust the DCF discount rate. In the following chart, we break down the final DCF discount rate in the Peruvian acquisition into the risks and premiums of each parameter.

Due Diligence

The key areas in the due diligence process are summarized below, including accounting and finances, taxes, operations, human resources, and legal considerations.

Accounting and Finances

Due diligence in Latin America M&A needs to consider that risks are higher with respect to transactions in the USA or Western Europe. We list some points of attention in this area:

- Beware of audited financial statements. In my experience, locally audited financial statements can be unreliable and should be verified. There are often adjustments not provided for in the financial statements, which can be substantially material for the target company and significant in the final acquisition price. In an acquisition I was involved with, external auditors determined that the target company’s working capital was $3.7 million. But when due diligence was performed, it turned out that working capital should have been negative $10.5 million, as there were missing short-term liabilities not recorded. Fortunately, due to the verification, we correctly reduced the acquisition price by more than $14.2 million. When working with external auditors, ensure that there is a leader within your organization or for hire with previous exposure to Latin America who can effectively communicate and supervise their work. I suggest that you verify all figures, even if financial statements are audited by external auditors, as risk perception of an external auditor is completely different than risk perception when valuing a business for acquisition purposes.

- When the deal is structured as base consideration plus working capital consideration, exclude non-value items from working capital not adequately provided for in the financial statements. It’s very possible that short-term assets will be overstated and that short-term liabilities will be understated—both of which would significantly impact the final acquisition price. Take it upon yourself to perform your own evaluation of the working capital; do not assume that audited working capital by external auditors is completely reliable.

- Conduct a full financial audit yourself or with external advisors. Once in the energy sector, I came across a case in which the decommissioning costs were not fully accrued—which resulted in an acquisition value $100 million below what it should have been worth. In another instance with a joint venture (JV), the accounting records of the target company indicated billing to the JV partners on items that were actually still in dispute and should not have been recorded on the balance sheet. Since the acquisition process is confidential, there should be protections written into the sale and purchase agreements prior to final closing.

- Make sure that local currency can be converted into USD and funds can be remitted offshore easily. Most of the Latin American countries offer free convertibility of the local currency; however, in some cases, it is difficult to make the funds available offshore or, in certain countries, additional taxes to remittances offshore apply. For example, Ecuador has a 5% tax on payments made offshore. If conversion or offshore remittance isn’t possible, your investment might be lost and it might not be advisable to invest.

Taxes

Latin America is a region with unusually cumbersome taxation and tax procedures. A high level of complexity can result from multiple tax laws overlapping on the same tax base. Tax risks for buyers entering Latin America can be from multiple sources, so the following questions should be considered:

- Are tax rates constantly changed? Obviously it is preferable that tax rate changes be anticipated and stable, but if they are likely subject to change, it’s advisable to incorporate a discount in your valuation acquisition model to account for this. It’s not uncommon for sweeping policy changes to occur—in 2007, the Uruguayan Tax Reform introduced a progressive tax on labor income of rates ranging from 0 to 30% and a flat rate on capital income of 12%; in 2008, the Ecuadorian government introduced tax reform aimed at increasing the progressivity of personal income taxes.

- Are deductions in the tax law accepted by the tax authority? Are financing structure of the company and deductions of interest accepted? In a number of countries, the tax law indicates deductions for which, when a tax audit arrives, the tax deduction is not fully accepted by the tax authority. The non-deductibility of interest in corporate loans to subsidiary is one example in Ecuador. In these cases, consider the financial impact in your acquisition valuation model of the target.

- Do tax authorities effectively reimburse tax credits, including VAT or corporate income tax credits? There might be a gap between tax law and what happens in actuality. If the country has a reputation or history of not reimbursing tax credits, you can consider incorporating into the acquisition valuation model.

- Are all tax audit risks reflected in the company accounts? Some companies decide not to include tax liabilities audit risk in the company accounts to avoid attracting attention from the tax authorities.

- Has dividend repatriation taxation been considered? Dividend repatriation is the return of earnings from offshore subsidiaries to their parent companies in the home country. The withholding tax applied to dividend repatriation when dividends are paid in the local country could result in hidden costs which can substantially reduce the investment’s net profitability. The ideal situation is to find a parent company jurisdiction in a country where there is a tax treaty signed to avoid double taxation with the country where the investment is located. This way, you can avoid the withholding taxes. Alternatively, the home country can use the tax credit of the withholding tax applied locally.

- Have you defined the optimal tax exit strategy in case of disposal? Always plan for the worst-case scenario, considering the tax implications of using offshore vehicles in the acquisition or if the VAT equivalent applicable tax is levied on exit.

- If you have other companies in the country, can tax consolidation be used? The profits of one subsidiary could be combined with losses of another subsidiary in the local country. This can reduce the global tax liability of the acquirer in the country. It can also increase the acquisition price; the acquirer is ready to bid if already-incurred tax losses in the local country can be utilized.

- Is an asset deal or equity deal more favorable from a tax standpoint? If it is structured as an asset deal, evaluate whether the asset value can be used for depreciation purposes in the country. The savings derived from the corporate income tax shield in the asset depreciation can significantly change the acquisition price that the acquirer company is ready to pay. A similar concept applies for goodwill.

Mitigating Tax Risk

Some actions for tax risk mitigation for the purchaser include guarantees, until the end of a statute of limitation, the use of escrow accounts to pass any cost incurred after the acquisition date to the seller, or simply factor the risk into the acquisition price. Another option is for the seller to be made responsible for the existing tax liabilities of the acquired company. In these situations, which apply in more than 50% of the cases I have participated in, legacy tax liabilities can last more than 15 years. On the flip side, if you’re the seller, you might want to lower your price and get rid of a potentially long-lasting issue.

In Ecuador, I once witnessed an M&A agreement indicate that all past tax liabilities would belong to the seller for 20 years. The seller eventually left Ecuador and lost contact with Ecuadorian tax law developments during these 20 years, leaving the local lawyers to take care of the tax court processes. It would have been simpler and less expensive to reduce the acquisition price rather than remain with the administrative burden to manage the tax appeals in court for 20 years.

In general, it’s helpful to consult at least two different external tax advisors. For example, in Ecuador and Guatemala, there isn’t much clarity around the deductibility of interests related to home office financing in the local subsidiary or the non-realized foreign exchange differences on the home offices financing when financing is made in a foreign currency. Though local tax legislation was not explicit, tax auditors were able to identify that the potential tax liability was huge. For particularly sensitive or complex tax issues, I’ve sought counsel from three external tax advisors.

Human Resources and Labor

When it comes to labor-related issues, there are a couple factors to be considered. For one, it’s important to understand the impact of trade unions’ negotiation power in the country and in the acquired company. In some cases, trade unions are so powerful that they jeopardize operations by paralyzing the company with strikes or simply making life difficult for company leadership. It’s also crucial to determine whether salaries are automatically adjusted to the foreign exchange USD variation with respect to local currency and if salaries are paid in local currency or in USD. If the target company’s revenues are based in USD, it would make sense to tie local salaries to USD. If not, local currency is preferable. However, we had one case in Peru, where salaries were originally in USD and changed to PEN local currency, as the PEN was appreciating, but revenues were based in USD. This led to losses due to the foreign exchange appreciation of PEN against USD of 20% of the total payroll costs of the company, (i.e., over $10 million).

Legal

Due to the political instability and changing regulation, legal, and compliance issues, doing business in Latin America M&A can easily become complex. Below are specific points to consider:

-

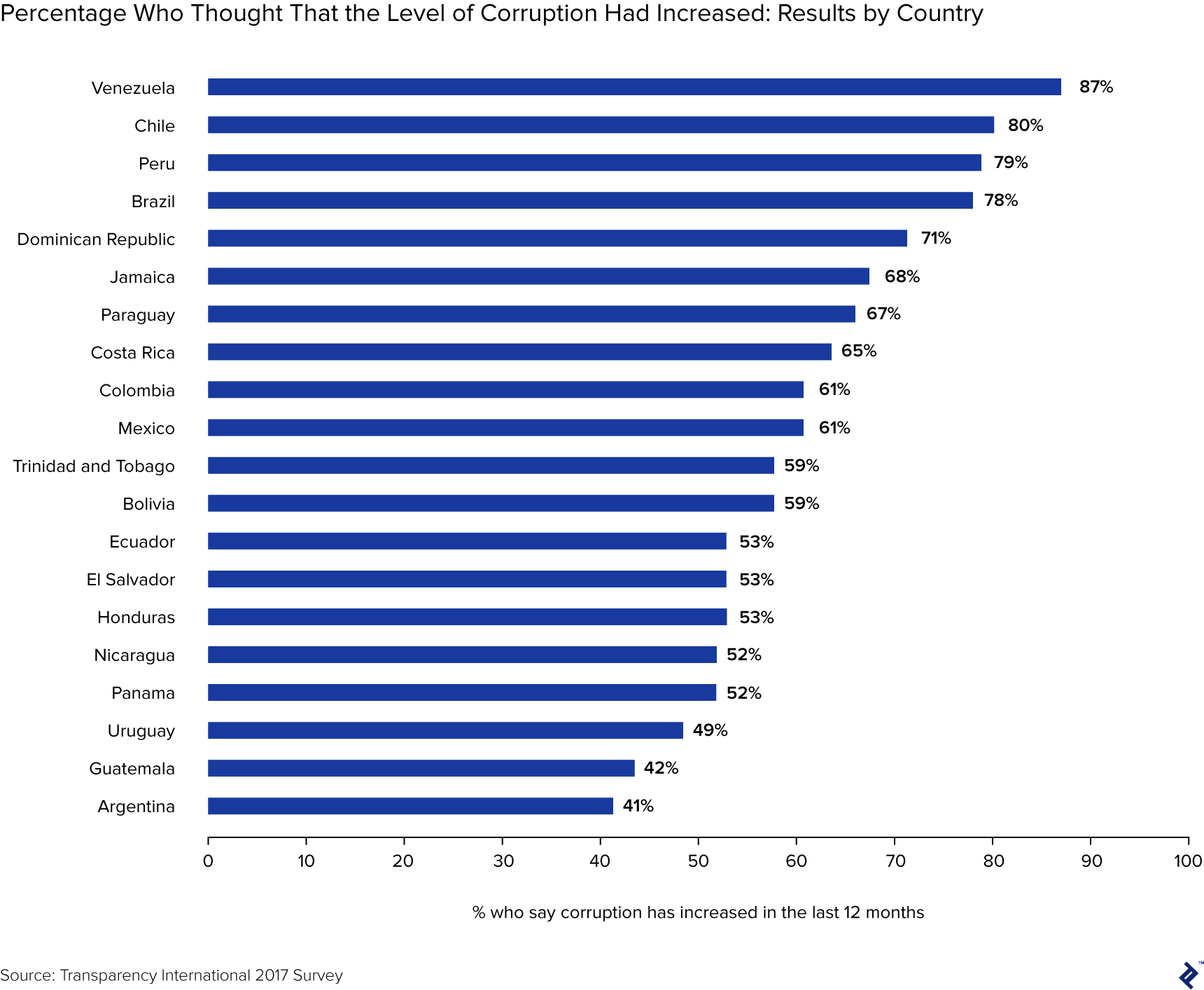

Bribery and anti-corruption are sensitive subjects in Latin America. In most cases, nothing arises from an audit, but the remaining instances could jeopardize the entire acquisition or even lead to penalties or pollution of the parent company’s reputation. Due diligence needs to be carried out on the full ownership and management of the seller, including all beneficial owners. Key customers and third-party intermediates also need to be identified and due diligence carried out on them and their relationships with government officials. Always request full disclosure of past or ongoing civil, criminal, and regulatory matters. According to the Transparency International’s 2017 survey of over 22,000 citizens in 20 Latin American and Caribbean countries, those in Venezuela, Chile, and Peru most believed that corruption had increased in their country.

- Corporate governance among partners. In the case of partnerships and joint ventures, analyze and scrutinize all meeting minutes, as claims from partners might not be adequately provided for in the financial statements, and the profitability of the contract might be dependent on this point. In a Brazilian deal I was involved in, the joint venture partner went bankrupt and the other partners had to face all liabilities of the loss-making contract.

- Foreign exchange variation in contracts. If contracts are denominated in local currency, make sure that, in the case of devaluation, exchange rate variations can be passed onto the client as a cost they bear. If there are government restrictions in regulated sectors, ensure that there is flexibility to change tariffs and prices applied to clients.

- Are client contracts enforceable? Contract enforceability is a key issue to consider, though in most cases it should not be an issue. However, if the contract is with the government as a client, this is an important point of consideration—even if legally the contract is enforceable, enforceability can be difficult in practice. In this case, a discount to the valuation of your acquisition should be applied. Sometimes, contracts in the utilities space can also be difficult to enforce.

- Is there a bilateral investment treaty (BIT) between the acquirer country and the acquisition country? A BIT is an agreement between two countries that sets up “rules of the road” for foreign investment in each other’s countries, and it’s easier to do business with it already in place. However, in case of expropriation, the International Center for Settlement of Investment Disputes (ICSID), the Tribunal of the World Bank for arbitrations, or other international tribunals can be leveraged. In my experience, the ICSID protection is a helpful contractual inclusion, but in practice, it should be considered a last resort since international arbitration disputes can last eight years or longer.

- Does your deal follow an onshore or offshore structure? An offshore structure refers to when the acquired company shares are held outside the country. If you take, for example, a British company looking to invest or acquire assets in Colombia, the company shares would be located in a legal entity in (for instance) the US state of Delaware. The Delaware company’s shares would be held by the British company and the Colombian assets would be part of a branch of the Delaware company. However, with an onshore structure, the Colombian company shares would be located in a company domiciled and registered in Colombia, with the shares of the Colombian company held by the British parent company. From a legal point of view, offshore structures offer stronger protections with regards to company shares ownership, as offshore entities are located in countries offering absolute protection to foreign investment; the final decision will depend on the tax implications of the onshore and offshore structure.

- Local laws are usually subject to interpretation or in conflict with other laws. Governments’ and courts’ interpretations might be very different than the company legal advisors’ interpretation. In case of doubt, a second or a third opinion of external legal advisors is necessary. Take, for example, the tax deductibility for corporate income tax purposes of interest expenses for intercompany loans in Ecuador, or the tax deductibility for corporate income tax purposes of unrealized foreign exchange losses of financing facilities in Guatemala. Local advisors were convinced of the tax deductibility of these but, alas, they were not tax deductible according to the tax administration.

- Avoid litigation in local courts if possible. Claims can last several years and much longer than what international standards dictate. I have seen administrative tax court procedures last more than 10 years in Ecuador, Brazil, or Guatemala. Arbitration can also be a protracted process in local and international courts, so, oftentimes, it’s best to reach a settlement and avoid the courts completely.

Incorporating Due Diligence Findings Into the Financial Model

It should be clear by now that strong, detailed due diligence is a key success factor in a Latin American M&A. Results from the due diligence process should always be incorporated into the final acquisition valuation before the sale and purchase agreement is signed.

Integration Planning

Effective integration planning needs to be established as early as possible. And, the more detailed the integration planning is, the lower the risk that the acquisition ultimately becomes a failed operation. Due diligence and integration actions can be prepared simultaneously. In fact, it’s ideal if the experts participating in the due diligence process are also the ones conducting the integration planning. Effective integration planning includes everything from integrating IT and identifying key sources of value and choosing and cultivating one company culture to carefully selecting leadership. In Latin America M&A, this last point is especially crucial. Ideally, new management will include those who understand the local culture and language and can keep up morale amongst legacy employees.

Parting Thoughts

Latin America is a region where a lot of interesting opportunities to acquire companies and expand activities can be found. However, as described in the article, the market is completely different than in fully developed markets such as North America or Western Europe. When companies expand in this region, they need to be aware that both language and cultural differences need to be addressed. While Latin American countries may appear to be westernized in many ways, conducting business is still different. The aid of experts exposed to Latin America business in acquisition processes and integration in this region will surely add value to the acquisition.

Disclosure: The views expressed in the article are purely those of the author. The author has not received and will not receive direct or indirect compensation in exchange for expressing specific recommendations or views in this report. Research should not be used or relied upon as investment advice.

Understanding the basics

A possible takeover target is a company that another acquiring company is interested in pursuing. The interest could stem from a number of reasons, including proprietary technology, a lot of cash on its balance sheet, or potential synergies between the two firms.

When a company buys another company, it’s called an acquisition. A company will buy most if not all of another company’s ownership to assume control of it. The M&A process includes valuation, due diligence (on financials, taxes, labor and culture, and legal), as well as final negotiation and integration

Emilio Labrador

Paris, France

Member since January 4, 2018

About the author

Emilio has 25 years of CFO experience in Europe and LatAm. An expert in M&A, he has executed two $300m+ acquisitions and a $400m+ disposal.

Expertise

PREVIOUSLY AT