Earnouts: Structures for Breaking Negotiation Deadlocks

The discipline of mergers and acquisitions is a complex and labyrinthine one, peppered with its share of false starts, thrilling chases, and heartbreaking shortfalls.

Toptal Management Consultant Javier Enrile explores the use and structuring of earnouts as one of the most effective tools for the M&A practitioner seeking to break negotiation deadlocks and mitigate risk.

The discipline of mergers and acquisitions is a complex and labyrinthine one, peppered with its share of false starts, thrilling chases, and heartbreaking shortfalls.

Toptal Management Consultant Javier Enrile explores the use and structuring of earnouts as one of the most effective tools for the M&A practitioner seeking to break negotiation deadlocks and mitigate risk.

Javier Enrile

Javier has 16 years of experience in mid-market M&A and VC, with 35 completed transactions and hundreds of others evaluated and negotiated.

Expertise

Executive Summary

Earnouts: What Are They, and How Are They Structured?

- An earnout is a contractual arrangement between a buyer and seller in which a portion or all of the purchase price is paid out contingent upon the target firm achieving predefined financial and/or operating milestones post transaction-close.

- Earnout structures involve seven key elements: (1) the total/headline purchase price, (2) the % of total purchase price paid up front, (3) the contingent payment, (4) the earnout period, (5) the performance metrics, targets, and thresholds, (6) the measurement and payment methodology, and (7) the target/threshold and contingent payment formula.

When Best to Use Earnouts

- Earnouts are best used to break purchase-price negotiation deadlocks during M&A transactions. These deadlocks occur most often when the buyer and seller's perceptions of value depart the zone of possible agreement.

- They are also used as effective alignment and incentive tools that keep surviving management teams and shareholders driving toward the same objective.

- Earnouts are also most effective when a given seller is demanding an ambitious purchase price and the buyer would like to allocate more of the performance risk implied by that purchase price to said seller.

The Reach of Earnouts

- In 2024, 41% of VC-backed company M&A transactions included an earnout, up from 27% in 2023, according to WilmerHale's 2025 M&A Report.

- Earnouts are much more common and far more valuable in sectors where future cash flows are inherently uncertain. These include biopharmaceutical and medical devices transactions, startups, and high upfront R&D product companies.

- Specifically, between 2012 and 2015, earnouts comprised 79% of all biopharmaceutical and 78% of all medical device transactions surveyed.

The Ugly Business of Negotiation Deadlocks

The process of buying and selling firms is, by nature, complex and lengthy. Whether its part of a growth-through-acquisition strategy or the case of a founder seeking to raise capital via a part-divestiture, M&A can be distilled into two components: valuation and risk allocation. In my many years as an M&A practitioner and expert, I have witnessed many an occasion where strategically accretive transactions to both parties fail to be consummated for differences in ascribed valuation or for an inability of the buyer to mitigate risk. In other instances, clever structuring has bridged differences between two divergent parties to great result, such as in Extreme Network’s acquisition of Broadcom’s Data Center Business, which leveraged various forms of deferred and contingent payments.

As abstract concepts, both valuation and risk are rooted in the future free cash flows of the target enterprise. Specifically, valuation, often represented as the enterprise value, is the present value of a company’s future cash flows discounted to present day at its weighted average cost of capital. The implied risk is embedded within the relative uncertainty of these future cash flows.

Unfortunately but oftentimes, exogenous factors in a dynamic marketplace increase the relative uncertainty around future cash flows so as to push both buyer and seller views on valuation outside the zones of agreement. When this occurs, contingent forms of payment, which include earnouts, escrows, holdbacks, and clawbacks, often represent the only available tools to break the negotiations deadlock.

This article explores the structuring and use of earnouts, specifically, as one such tool for bridging valuation deadlocks in M&A deal-making. As part of this process, I will seek to arm both buyers and sellers with (1) an understanding of the benefits and risks to earnouts; (2) insight into when earnouts are best used and are most effective; (3) an analytical framework for understanding earnouts’ constituent/structural elements; and (4) empirical evidence that earnout structures do also serve as effective downside/risk mitigation tools.

The Basics: The What and the Why

Our first question must be, what is an earnout? An earnout is a contractual arrangement between a buyer and seller in which a portion or all of the purchase price is paid out contingent upon the target firm achieving predefined financial and/or operating milestones post transaction-close. Earnouts confer a range of benefits to those who utilize them.

Benefits to both parties:

- Break purchase-price deadlocks between buyers and sellers;

- Force difficult conversations between the selling or surviving management team and the buyer around how the asset will be operated post-acquisition.

Benefits to buyers:

- Reduce the quantum of capital that must be put at risk at the point of transaction-close;

- Afford the buyer the opportunity to anchor the fair market value of the target on its performance and not sentiment;

- Shift the risk of post-merger/acquisition underperformance from the buyer to the seller;

- Create a source of alignment and retention for the target firm’s surviving management team by affording them attractive, milestone-based time and performance incentive packages tethered to post-acquisition outcomes;

- Provide an effective deferred financing mechanism that may afford undercapitalized buyers the opportunity to still acquire an attractive target with time to bridge the remaining capital requirement. In most cases, the buyer is actually able to partially pay for the acquisition from earnings from the target firm;

- Exist as a self-selection mechanism—low-quality target firms are generally reluctant to accept this type of structure given that the target firm’s management knows the earnout has a low probability of success; and

- Let the target asset prove its worth.

Benefits to sellers:

- Afford the opportunity for an ambitious sale price, should said seller be willing to earn it—a purchase price that would ordinarily be unattainable at the then current discounted cash flow valuation assessed by the buyer.

The Downside to Earnouts

As with most structured finance solutions, there also exist some clear disadvantages to earnouts. The greatest of these is the potential for litigation in the period between transaction-close and the earnout’s expiration. Although in theory, earnouts align the interests of both buyer and seller to post-acquisition financial and operating success, there are several areas where interests, plans, and preferences still diverge.

The most common of these is how the target firm will be run en route to achieving the mutually agreed-upon targets. This challenge is most common where the acquired firm becomes part of a larger business and strategy and is thus expected to operate differently from how it did as a standalone entity. Though the scope of this article doesn’t extend as far as exploring litigation issues, contractual provisions should be put in place that protect buyers against potential litigation from sellers.

These contractual provisions typically fall into two categories. The first is to negate any and all implied obligation on the part of the buyer to achieve the earnout such that unsatisfied sellers cannot invoke covenants of good faith and fair dealing that claim the buyer operated the target firm in a manner that frustrated the company’s achievement. And the second provision should stipulate that the buyer has absolute discretion over the operation of the target firm post-acquisition.

The Zone of Possible Agreement

As previously mentioned, during a negotiation, buyers and sellers will usually have differing views on valuation. This is no cause for concern so long as their views fall within the zone of possible agreement (ZOPA). However, and as previously alluded to, circumstances do arise whereby the degree of uncertainty surrounding the target firm’s future cash flows is so high as to push both parties’ views outside of the ZOPA. These circumstances typically fall into one or more of the following categories:

- Lack of operating and financial track record

- Recently restructured organizations—specifically, organizations that have recently undergone such dramatic internal changes that their financial and operating track records, and thus projections, are no longer credible predictors of the future

- Major shifts in strategic direction coming in the form of new business units, major new product lines, or major new geographical bets, which again make past performances inaccurate guides of the future

- Concentration and key-man risk that range from customer concentration, supplier concentration, and capital source concentration to key man risk, especially where founders are still active at the point of sale

- Heuristics and personal biases, which are typically driven by either past personal or professional experiences or cultural affectations (where cross-border transactions are concerned) that can drive sometimes insurmountable divergences in expectations

Beyond these, other variables do exist that also push up or down ascribed value during M&A negotiations. One such example is the sellers’ sentimental attachments that drive up price. This most often occurs when founders choose to sell their companies (i.e., their “life’s work” or “baby”). Buyers also have their set of emotional drivers. One such common example is buyers who undervalue a target as a fear-induced knee-jerk reaction to a past experience gone bad.

Structuring Earnouts – A Simulated Case Study

Based on my many past experiences, I have constructed a case study that will help simulate and explain how to structure earnouts. It is as follows:

Firm A (buyer) has conducted an internal strategic review and concluded that it suffers an important product gap. Its competitive landscape has evolved such that its customers now prefer one-stop-shop solutions that include Product X, which it does not currently produce. Given that speed to market is critical in Firm A’s arena and it has great knowledge of its competitive landscape, it opts to acquire a startup, Firm B, which specializes in Product X. NDAs and financial and operating data begin to be exchanged in a data room.

Firm B conducts its internal discounted cash flow analysis (DCF) that yields an Enterprise Value (“EV”) of $16 million, below:

Firm A conducts its DCF analysis that yields a materially lower EV of $4 million, below:

The Negotiation

Firm A puts forward an offer of $4 million and Firm B counters with an ask of $16 million, pursuant to which both firms meet and negotiate face-to-face. Firm A explains that Firm B has only one year (2025) of financial history and that, though profitable, they are yet to prove that they can capture market share from other competitors.

Conversely, Firm B explains that Product X is powered by patented, proprietary technology (lower cost) and is sufficiently differentiated from other products in the market to not only capture share but create new demand. Firm B’s view is that this will drive revenue growth at rates well in excess of industry averages.

After days of negotiations, both firms find themselves in a purchase price deadlock and depart without an agreement.

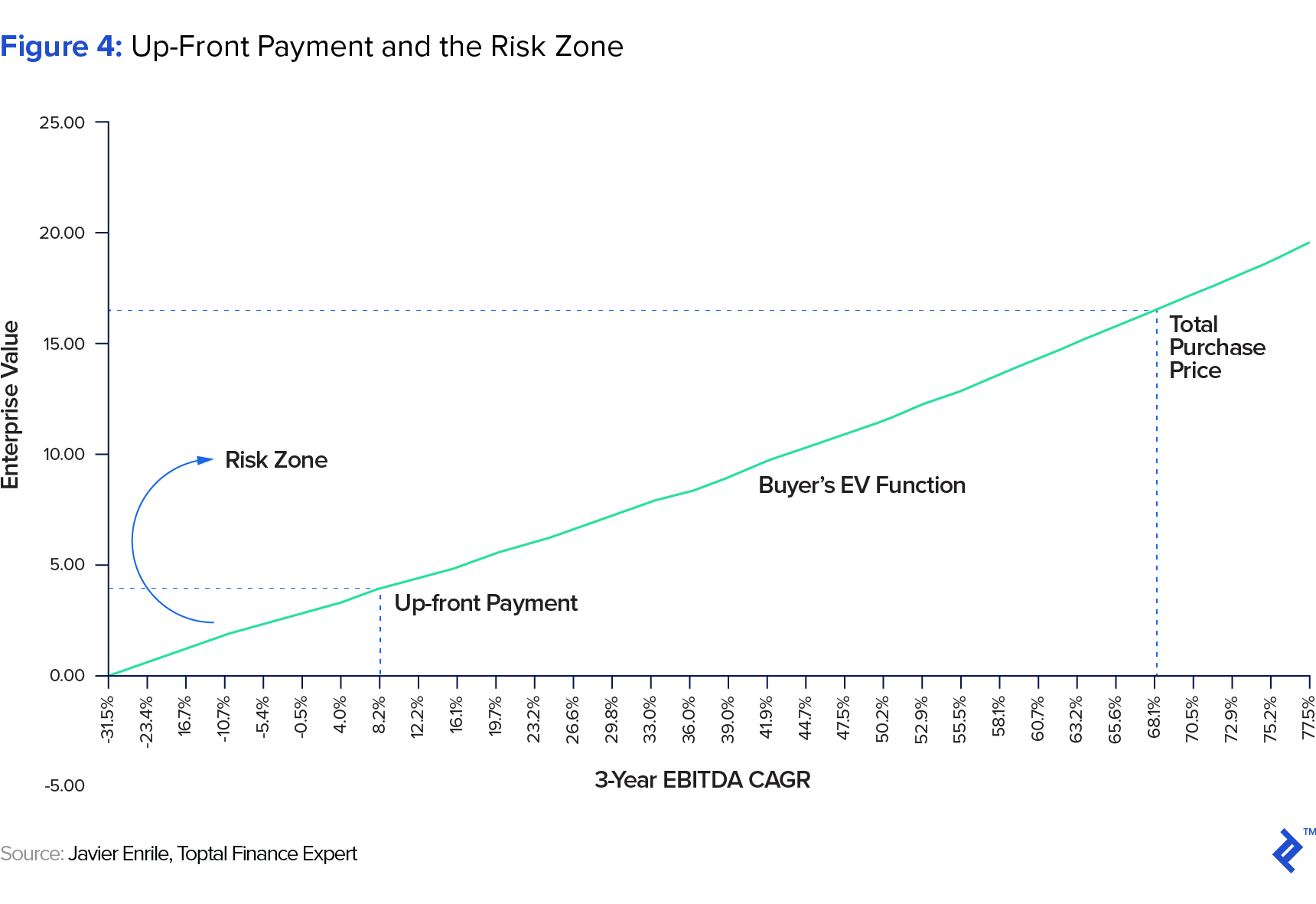

Figure 3, above, illustrates/reflects the buyer’s model and assumptions—the x-axis shows Firm B’s EBITDA 3-year CAGR and the y-axis shows the implied enterprise values. The buyer’s EV function reflects the range of implied EV possibilities for Firm B as a function of the discount rate, revenue growth, and cost basis assumptions it assumed during its analysis.

Given that Firm A understands the strategic value to acquiring the capability to manufacture Product X as soon as possible, it opts to design an earnout structure that bridges the valuation gap, driven by its future cash flow concerns and thus breaking the negotiation deadlock.

Earnout Structuring

The following section looks at each of the key elements to consider when structuring an effective earnout arrangement, of which there are seven: (1) total/headline purchase price, (2) up-front payment, (3) contingent payment, (4) earnout period, (5) performance metrics, (6) measurement and payment methodology, and (7) target/threshold and contingent payment formula. These elements are best explained and understood sequentially, with each element building on the next.

-

Total purchase price (or headline purchase price): The first step is to determine what the total amount is that will be received by the seller. If the buyer knows the seller’s ask and wants to maintain a strong negotiating position, then most often the buyer sets the total purchase price equal to the seller’s ask.

This signals to the seller that the buyer is willing to bridge the entire valuation gap and affords the seller the opportunity to earn the purchase price asked. However, at other times, the buyer may not be willing to bridge the entire valuation gap and will instead set the total purchase price at 70% to 80% of the seller’s ask.

Our simulated case study assumes a total purchase price of $16 million, given the strategic value of the target and how competitive the acquisition landscape might become if others get wind of the transaction.

-

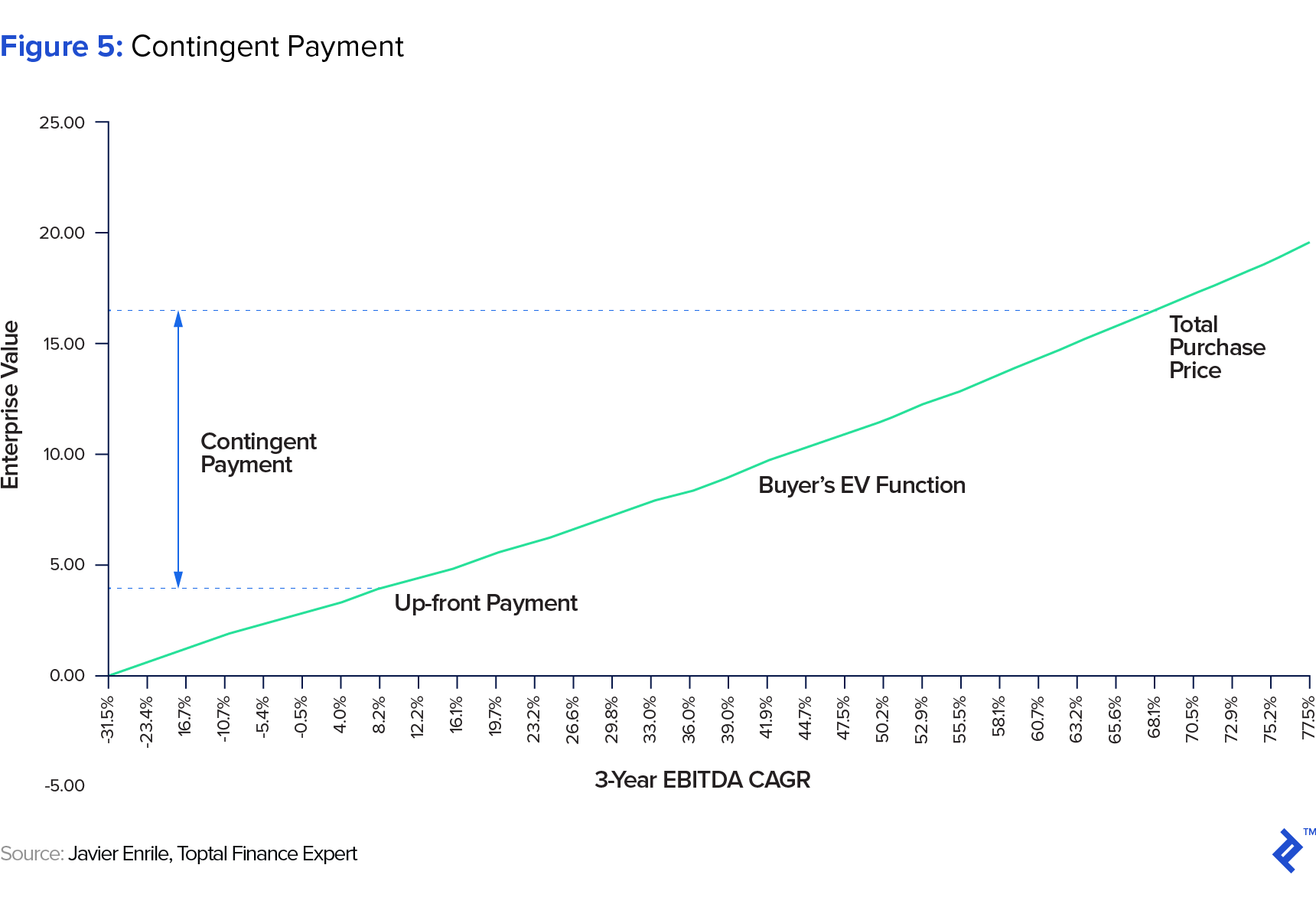

Up-front payment: The second step is to determine what portion of the total purchase price will be paid at the transaction closing. From a buyer’s perspective, the maximum amount of the up-front payment should equal his calculation of EV and is a variable of utmost importance given it represents the buyer’s capital-at-risk—i.e., the capital in the risk zone (see Figure 4 below) that will be written off should the target underperform so significantly that its EV comes in lower than the upfront payment. Often, buyers want to further derisk the transaction by lowering the up-front payment below their calculation of enterprise value, shrinking the risk zone.

This case study assumes an upfront payment of $4 million, as Firm A has a high degree of confidence in its projections and analysis of Firm B’s cash flows.

-

Contingent payment: The third step is to determine the contingent payment, where the contingent payment is defined as the total purchase price less the up-front payment. The implied contingent payment for purposes of this simulation is $12 million ($12,000,000 = $16,000,000 – $4,000,000).

- Earnout period: The fourth step is to determine the earnout period. Earnout periods typically have a duration of between one to five years. SRS Acquiom’s 2026 M&A Deal Terms Study reports a 24-month median for non-life-sciences earnouts, with no deals in their sample exceeding four years, marking a continuing shift toward shorter performance periods. In my experience, the earnout period should be long enough to provide the surviving management team sufficient time to achieve their goals but not so long as to induce “goal fatigue.” Our case study assumes an earnout period of three years, which sits at the longer end of current market practice.

-

Performance metrics: The fifth step is to determine the performance metric which will be used, above all others, to evaluate the target firm’s performance. Such metrics should be mutually agreed upon, well understood, clearly defined, and easily measured.

There are two categories of performance metrics, financial and operational. Financial metrics are typically revenue or profits based, e.g., revenues or EBITDA. Revenues is used when the target firm is fully integrated into the buyer, making it very difficult to measure the stand-alone profit profile post-assimilation. And profit-based metrics such as EBITDA are used when the target firm will continue to be operated as a stand-alone subsidiary with its own set of discrete financials. Operational metrics are typically measured via milestones and are most common in technology companies or pharmaceutical firms where new product development can greatly increase the EV of the target firm.

For purposes of our case study, EBITDA is selected as we are assuming the acquired company will continue to be operated independently into perpetuity.

-

Measurement/payment frequency and methodology: The sixth step is to determine the measurement and payment frequency. There are two general options in this regard: (1) multiple, staged measurements and payments, executed annually or more often; and (2) a single measurement and bullet payment, typically at the end of the earnout period.

As a long-tenured M&A practitioner, I will always advise against the multiple measurements/payments methodology because its process often comes with substantial tension, noise, and distraction for management. That said, and for obvious reasons, it is common for the seller to prefer smaller and more frequent milestones and payments, in order to stage and mitigate the adverse consequences to their operating risk.

In addition to frequency of payments, the measurement methodology must also be determined. Two general methodologies exist: (1) a financial performance growth rate between the acquisition date and earnout maturation date, e.g., revenue or EBITDA compounded annual growth rates (CAGR), or (2) absolute value target, achievable between the acquisition date and earnout maturation date, e.g., cumulative EBITDA.

Our case study assumes a single measurement and payment in December 2028 based on a 3-year EBITDA CAGR from 2025-2028.

- Target metric and contingent payment formula: The seventh and final step is to determine the target metric (i.e., the level of performance) and the corresponding amount of earnout payments for such level of performance. To balance risk and reward, the structure should provide rewards for partial performance by the target firm, even if it does not completely meet its performance goals—in other words, a binary, all-or-nothing approach is rarely seen in or by the market.

Figure 6 above illustrates a contingent payment function and associated payments under different 3-year EBITDA CAGR realizations. We will use our model to illustrate how to determine the three components of the contingent payment function:

-

Higher end of the contingent payment function: Shown as ① above, this is the target metric at which the full contingent payment is paid, typically set according to the performance forecasts submitted by the target firm’s management. This puts the buyer in a strong negotiating position as the seller must simply deliver on their forecast to receive their asking price. Note that, as a general rule, the higher end of the contingent payment should not exceed the buyer’s EV function.

The case study assumes a target metric at the 3-year EBITDA CAGR of 68% to receive the full contingent payment of $12 million.

-

Lower end of the contingent payment function: Shown as ③ above, this is the threshold outcome at which some level of contingent payment begins to be paid. There are two components that need to be determined ahead of this juncture: (A) the threshold outcome; and (B) the starting quantum of contingent payment assuming the realization of said outcome. It is important to note that the target metric (i.e., threshold outcome) should always be higher than (or to the right of) where the buyer’s EV function crosses the contingent payment function shown (shown as ② above). The logic is that having set the up-front payment, the buyer should only pay any contingent payment when the target firm’s enterprise Value is at least equal or greater than the up-front payment, i.e., the break-even point. Most often, the starting payment is set at zero; however, depending on where the lower end is set, the seller may require some level of contingent payment. Note that, as a general rule, the starting contingent payment for a given target metric should not exceed the buyer’s EV function.

The case study assumes the threshold outcome at a 3-year EBITDA CAGR of 19.7% and the starting quantum of $0. For purposes of the case study, we assume that the buyer wants to financially engineer a gain by setting a combination of the threshold outcome and the starting quantum which results in a gap between the contingent payment function and the buyer’s EV function (shown as ④).

-

Contingent payment function—payments between the lower and higher end: This is typically calculated using linear or exponential interpolation—i.e., in an exponential function such that, as the rate of growth becomes higher, the contingent payments are also higher.

The case study assumes a linear interpolation between the lower and higher end of the contingent payment function.

Mitigating the Downside Risk

Often buyers and sellers agree on price; however, buyers perceive exogenous risks which could put downward pressure on the target firm’s performance and look to structure earnouts to shift the risk of underperformance to the seller. The most typical exogenous risks I have seen in my practice today are uncertainty around the Fed’s rate-cut path, tariff and trade policy volatility, geopolitical risk, and client concentration.

We use the same case study to illustrate how earnouts mitigate the downside risk. Assume that there are two buyers for Firm B. Buyer A believes in Firm’s B three-year forecast at a 68% 3-year EBITDA CAGR and therefore he is comfortable paying $16 million all upfront (no earnout). Buyer B also believes in Firm’s B forecast but expects with a high level of confidence that the combination of an uncertain rate-cut path, tariff-driven cost pressures, and persistent valuation gaps will weigh on near-term cash flow growth; therefore, puts in place the earnout (same structure as described above) to mitigate the downside risks of Firm B’s underperformance stemming from his macro views.

Figure 7 below shows the IRR for both Buyer A and B as Firm B underperforms its growth expectation and provides empirical evidence that earnout structures mitigate downside risk. The IRRs with an earnout structure remain positive and much higher than that without an earnout structure in a scenario where Firm B underperforms by growing at a rate less than the 3-Year CAGR of 68%.

The Bottom Line

In conclusion, the discipline of mergers and acquisitions is a complex and labyrinthine one, peppered with its share of false starts, thrilling chases, and heartbreaking shortfalls. The failures to consummate transactions, despite months of diligence and prep, courting on both sides, and an equal willingness to create value often spring from irreconcilable differences around valuation or from the inability of one or both sides to effectively mitigate risk.

Earnouts, though oftentimes trying and challenging to negotiate, are one of M&A’s all-time great tools to both break purchase-price deadlocks and reallocate risk. I encourage aspiring and experienced M&A practitioners alike to study up on earnout structures and add these arrangements to their toolkit and skillset.

Understanding the basics

An earnout is a contractual arrangement between a buyer and seller in which a portion or all of the purchase price is paid out contingent upon the target firm achieving pre-defined financial thresholds and/or operating milestones post-transaction.

Earnout agreements are legal and binding contracts which legislate and detail the structure of an earnout. They detail the seven key elements to earnouts: (1) total purchase price (2) up-front portion (3) contingent payment (4) duration (5) metrics (6) measurement/payment method, and (7) payment formula.

An earnout structure is the sum-total of all the elements which aggregate to a negotiated earnout. These elements include the purchase price, including financial and/or operating thresholds/milestones, up-front payment, and contingent payment.

An earnout model shows the relationship between the purchase price payments (both up-front and contingent) and the value of the firm. It is, in effect, the representation of the earnout’s payment formula, detailed in with great specificity in the earnout agreement.

An earnout clause is a specific provision or section within the earnout agreement or merger agreement that details in great detail the nature and purpose of an earnout structure.