Raising Venture Capital in Down Markets: A Guide to Early-stage Funding

In tough financial times, VCs often focus on shoring up portfolio companies rather than investing in new opportunities. But it’s still possible to raise capital—if you refine your approach.

In tough financial times, VCs often focus on shoring up portfolio companies rather than investing in new opportunities. But it’s still possible to raise capital—if you refine your approach.

Erik is a co-founder of a global venture capital fund that has invested in 50 startups (raising more than $500 million) and has realized six exits. He serves as Toptal’s Chief Economist and holds an MBA from Harvard.

Expertise

Previously At

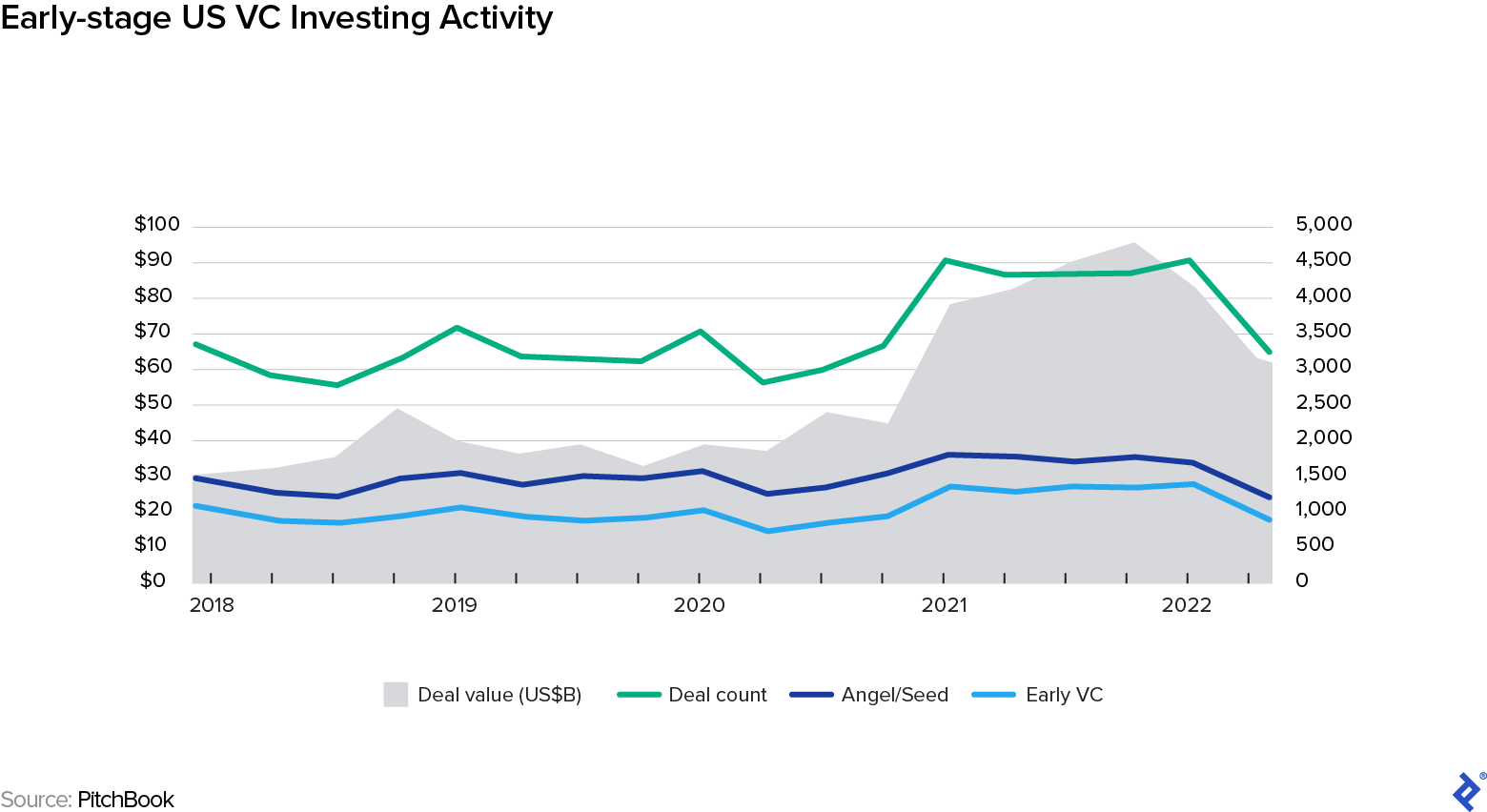

In a bull market, startup founders have many forces at their backs—including an investor outlook that is optimistic and risk tolerant. But when financial conditions get more challenging, as they have in 2022, those tailwinds become headwinds, and raising capital becomes harder. Investors shift their focus to battening down their portfolios’ hatches—typically by directing more funds to their current companies—rather than seeking new opportunities. That means that to get investor attention in a down market, startups looking for early-stage funding need to adapt their tactics.

Regardless of the economy’s direction in coming months, the volatility we’ve experienced in 2022 will most likely affect fundraising dynamics well into 2023 and potentially beyond. While capital raising and startup investing activity has proved resilient so far, the rules for successfully closing a funding round are changing.

Over more than a decade, I’ve helped hundreds of founders with early-stage funding, including the traditionally underrepresented founders my fund works with, who often face additional challenges. As a result, I’ve learned a lot about raising venture capital when that capital is less than forthcoming.

Much of my advice in this article also applies during favorable markets, but during uncertain times, the steps I outline become all the more important as emphases shift. Understanding these nuances will help you get the funding you need, no matter what the economic climate.

Focus on Active Investors, Not Perfect Investors

Many times, I’ve seen new CEOs burn precious time and resources identifying what they perceive as their ideal investor—one whose interests and priorities mesh perfectly with their goals—before making an approach. Although it’s wonderful to find that kind of match, this strategy can often lead to analysis paralysis, which is not something a startup can afford in a down market.

Instead, your search should be an ongoing process of active discovery as you build a strong pipeline of a hundred or more high-quality prospects and begin to systematically reach out and have exploratory conversations. The only way to find the best investor is through discussions with many qualified possibilities.

In a market that’s less than flush, your first question shouldn’t be, “Who is the perfect match for my vision?” but rather, “Who is a good match and still actively deploying capital?”

Watch investor news. You can find lists of the most active investors in your region or sector through sources like AngelList. You can also identify potential investors by looking at new funds that recently closed. These funds need to start deploying their capital. The smart ones will understand that down markets offer them the potential for more favorable deals and final terms as other investors become unable or unwilling to invest in new companies. Pay close attention to the news, LinkedIn, and Twitter, and consider setting Google alerts to stay informed.

Look for recent liquidity events. Likewise, review sources such as PitchBook, consulting and banking firms, and independent research firms for any recent payouts in your market, geography, sector, or type of technology. These investors will soon have dry powder available (and presumably be in a good mood as well).

Start local. As you start to identify potential investors, you’ll want to focus your attention locally. Many early-stage investors tend to be biased toward companies located in the same city or region. In a down market, when investors are holding on more tightly to their cash, founders can waste a lot of time looking too far afield. That said, sometimes geographical proximity is impossible: If you are an international founder looking to fundraise in the United States—which is by far the largest provider of startup capital, typically at more attractive terms—you can create a proximity to VC hotbeds like New York City or San Francisco by connecting with your country’s consulate and expat organizations in those cities. They may be able to introduce you to business and investment leaders who can facilitate further introductions or even invest themselves.

Network, Network, Network

In a difficult market, scoring an initial meeting becomes even more challenging, which means it’s essential to leverage the network of the investor’s portfolio and partners to your advantage.

Get referrals. As frustrating as it may seem, especially for first-time founders, a warm introduction from someone the investor already knows is by far the best way to get their attention. This is admittedly an inevitable function of the insularity of the venture world and the sheer volume of cold calls that investors receive. But it also happens for another, more justifiable reason. One of the most important qualities investors look for in a founder is the ability to find and secure necessary resources—talent, clients, media attention, and financing. So the first part of the test is simply whether you can successfully find and get in touch with an investor that suits your business.

Research mutual relationships. Use LinkedIn to find connections you have in common with your target investor and ask them to facilitate an introduction. If you don’t have a connection to leverage, take a look at the investor’s portfolio holdings on their website, and then use LinkedIn to see if any of your connections work at those companies. Alumni networks and similar social, business, or philanthropic organizations that you belong to can be another valuable resource. And don’t forget to think beyond your immediate contacts to their contacts as well. I’ve noticed that most people underestimate the size of their second-degree networks. In a down market, you can’t afford to be shy about asking for introductions.

Talk to other founders. Your network of other startup leaders is another rich vein to mine, as they have already successfully navigated their investors’ vetting and due diligence. Whenever my fund finalized an investment in a new company, the first thing we would ask the founder for was the names of the three other founders they most respected. We sourced a number of excellent deals this way. If this isn’t your first capital raise, ask your existing investors if they will connect you with any of their other portfolio companies that have recently raised capital. Talking to these founders is a great way to learn more about their other investors and how best to approach them. For example, I once spent a year trying to help a portfolio company raise its Series A until we finally realized that it was tackling a market similar to that of another portfolio company that had successfully closed a round of similar size. We introduced the two founders, and weeks later the same group of investors executed that company’s round, too.

Don’t bother with a broker. You may be tempted to hire a finder to help you secure valuable introductions, but I generally don’t recommend this, especially for early-stage funding. Part of winning your investors’ confidence is showing that you can find your own way to the table and are commiting your own time to do so.

Tailor Your Pitch to the Investor’s State of Mind

Once you’ve secured an audience with an investor, it’s time to convince the people you’re meeting with that yours is the one out of 100 (or more) deals they’re considering that most warrants their capital.

In an up market, a good idea and strong growth potential may be enough for an eager investor. But in a tough market, investors tend to be less willing to take a chance, which means you can’t just polish your pitch and hope for the best. You have to tailor it to address VCs’ current attitude toward investing and thoroughly convince a potential investor of your company’s immediate economic viability.

Making the effort more difficult, investors tend to decide almost instantly. Starting strong is crucial when you make your pitch, and telling a good story is always important. These are the five main things your investor needs to believe:

The problem you’re solving is serious and urgent. In the spirit of getting to the point right away, you might be tempted to front-load your deck with the solution, but don’t forget to set up the problem first. This step is especially vital in difficult markets, in which I’ve seen rounds more likely to close based on the size and severity of the problem solved. That’s a change from the past few bullish years, which have shown how during stronger markets, rounds can often close based on the type of solution (like “Uber for X”) or simply the wow factor of the technology (such as the now-cooling enthusiasm for all things blockchain). The size, scope, and urgency of the problem you’re solving speaks to your target customers’ willingness to use—and pay for—that solution. Show rather than tell (to the extent possible), and paint a vivid picture of its consequences.

Your solution is transformative. Customers rarely trouble themselves with adapting to a new product that is only marginally better than the current offering. It’s not enough to say your product improves on efficiency, safety, or effectiveness. Especially when you’re facing risk-conscious investors, you have to prove it reimagines how the market will function.

You have validated the market. Demonstrating that customers are already using your product or have signed up to be among the first to do so significantly decreases the perceived risk for investors. Even if you haven’t opened the store, being able to show a line down the street outside is always highly effective, particularly during times of economic uncertainty. Wait lists, signed letters of intent, and locked-in distribution partners all validate market receptiveness.

Your idea is financially stable. Investors may sometimes overlook financial stability, but they suddenly rediscover it when the economy goes south. The four metrics you need to show VC investors to prove long-term profitability are: Customer lifetime value that exceeds acquisition cost; strong user retention; organic, rather than paid, growth; and a financial model that shows you have the flexibility to conserve capital when necessary and ramp up when economic circumstances allow.

The team has operational, and preferably startup, experience. Founders may be surprised to learn that the team is by far one of the top factors influencing the investment decision in a firm’s early stages. A great idea isn’t worth much if investors don’t have confidence in the team’s ability to execute. Put the team slide early in your deck, and include up to three bullet points that quantify each person’s relevant experience.

Create Urgency to Seal the Deal

Once you have an investor at the table, you still need to persuade them to write a check.

Make sure it’s a competition. Unfortunately, investors tend to want to see others commit before they do, which can lead to a maddening situation with many on the cusp of saying yes, but none willing to be the first. And an investor can often be more likely to request aggressive terms during a down market based on the assumption that it may be your only option. I advise startups to get multiple investors involved in discussions and negotiations—and to make sure each one knows you’re courting other funders as well. This should be conveyed diplomatically but firmly. This encourages prospective investors to make an offer, the best terms they’re willing to consider.

Remember that you have more options than you think. If you can’t make a deal you can live with, don’t panic. There are still trillions of dollars waiting to be invested out there, and most of it isn’t tied up in venture capital. An increasingly rich and diverse landscape of non-VC options can improve your chances of receiving the early-stage funding you need on the best terms possible. These include angel investors, private equity, family offices, debt financing, and even online crowdfunding. (The guidance I provided here will also serve you well with any of these types of investors.) And finally, you can always consider bootstrapping.

Always Come to the Table Yourself

If I can impart one last piece of advice, it’s this: As the founder/CEO, the responsibility to see fundraising through to completion rests with you—not your broker, your consultant, or even your other team members. Although you can and should include other company leaders at investor meetings, the biggest mistake you can make is to think that responsibility for the final outcome rests with anyone else.

From a pragmatic perspective, there are some questions that only the CEO can answer well. And the psychology behind the principle is important, too: Raising capital yourself sends a powerful signal to investors that you are committed to your venture and take their investments seriously.

One of the best founding CEOs I’ve known described his job as “setting the larger strategic vision and ensuring we never run out of cash.” I know it can be tempting to focus on the first part. But the second is just as important, and embracing that duty can go a long way toward making your startup a success, no matter what the economic climate.

Further Reading on the Toptal Blog:

Understanding the basics

There are typically five stages of funding. First is pre-seed funding, which helps company founders develop their idea. Next comes seed funding, which supports the transition from idea to business. Series B funding follows and funds growth beyond the development stage. The next step is Series C funding, which helps the business expand. That may be followed by Series D funding, which funds further growth in lieu of an IPO.

Early-stage startups are typically still getting off the ground. Their teams tend to be small, and they may still be developing their product and firming up their milestones. They may or may not have a prototype or customers at this stage.

Any type of startup funding comes at some kind of cost. It’s important to consider your appetite for taking on debt, sharing ownership in the company, putting your own money on the line, or rewarding crowdfunders. Financial modeling can help you determine which option works best for you.

There are a number of funding options available for startups. Venture capital, angel investors, private equity, and debt financing are all options for raising capital. Family offices and crowdfunding are increasingly common, too.

You should raise capital when it’s time to bring your company to the next inflection point in its growth. Typically this occurs once you’ve met the milestones from your previous funding round and are ready—and need more support—to implement the next level of your business plan.

Erik Stettler

New York, NY, United States

Member since March 15, 2018

About the author

Erik is a co-founder of a global venture capital fund that has invested in 50 startups (raising more than $500 million) and has realized six exits. He serves as Toptal’s Chief Economist and holds an MBA from Harvard.

Expertise

PREVIOUSLY AT