Valuation Ratios: The Key Metrics Management Consultants Need to Know

Not sure when to use which valuation ratio for which situation? In this article, we’ll delve into the must-know metrics and provide heuristics of when to use which measure.

Not sure when to use which valuation ratio for which situation? In this article, we’ll delve into the must-know metrics and provide heuristics of when to use which measure.

Elizabeth was an equity research analyst on both the buyside and sellside before transitioning to freelancing where she specializes in market research and valuation.

Expertise

Previously At

If I offered to sell you my company for $5, would you buy it? Is it worth it? Even though it seems cheap at just $5, if I’m currently a loss-making business, you’re actually paying to lose money. Maybe not a great deal.

That’s why valuation ratios are so important in determining a company’s worth. A valuation ratio formula measures the relationship between the market value of a company or its equity and some fundamental financial metric (e.g., earnings). The point of a valuation analysis is to show the price you are paying for some stream of earnings, revenue, or cash flow (or other financial metric). So if I pay $10 for a company that expects to earn $20 every year for the next 10 years, that’s empirically a pretty good deal. Side note: This is an insanely cheap company and likely has never existed—this would imply a P/E ratio of 0.5x (10/20) versus the current S&P 500 forward P/E of roughly 20x.

Considerations like time value of money are important as well—a dollar today is worth more than one 10 years from now. So generally, investors look at valuation ratios based on estimates of future earnings (or cash flow or revenue or community adjusted magic).

There are zillions of valuation ratios out there. Weird ones that subtract all sorts of issues. There are also the broader commonplace ratios that help you speak the same language as other investors. I will first mention the five “must-know” ratios that will help you speak the native tongue, and then I’ll touch upon a few esoteric gems in a follow-up post.

A quick data note before we dive in. Valuation metrics are most useful when thinking about the future, and therefore, the metrics we choose for financial valuation should be based on what the consensus expects in terms of earnings, cash flow, etc. While your view of earnings potential may differ, it’s good to know what the market expects so you can understand what is built into the price. Those expectations shift with the broader economic environment, particularly interest rates, which also influence the valuation multiples investors are willing to pay.

If you don’t have access to a $50k Bloomberg terminal, you can find consensus estimates at Yahoo Finance, Zacks (for revenue and earnings at least), and Koyfin (revenue, earnings, and EBITDA). AI-assisted research tools such as AlphaSense have also made it much easier to find analyst consensus estimates.

Price-to-Earnings

The price-to-earnings ratio shows the relationship between the price per share and the earnings (also known as the net income or profit, essentially the revenue minus cost of sales, operating expenses, and taxes) per share. This is the amount a common stock investor pays for a single dollar of earnings.

When To Use P/E

- Starting off point for valuing nearly all companies

- When you want to quickly perform a relative valuation analysis of multiple companies to see what others are seeing

Pros

- Widely used. The fact that P/E ratios are so widely used means you can quickly compare and contrast with other stocks. You can also quickly communicate with other investors as everyone has some of their own P/E heuristics in mind.

- Easy to use. Both sides of the ratio are somewhat easy to find, assuming you don’t want to adjust the earnings number. Current prices can always be found on Yahoo Finance, and earnings estimates remain among the easiest consensus metrics to obtain.

Cons

- Easily manipulated. Earnings are calculated with accrual accounting and are subject to a lot of company massaging. Nothing fraudulent, but companies have more discretion on this number versus something like cash flow.

- It doesn’t incorporate the balance sheet. P/E ratios don’t consider debt.

Price-to-Cash Flow

The price-to-cash flow (P/CF) ratio measures how much cash a company is generating relative to its market value.

Price-to-cash-flow (P/CF) is a good alternative to P/E as cash flows are less susceptible to manipulation than earnings. Cash flow does not incorporate non-cash expense items like depreciation or amortization (income statement metrics), which can be subject to various accounting rules.

A company with a share price of $20 and cash flow per share of $5 equates to a P/CF of $4 ($20/5). In other words, investors currently pay $4 for every future dollar of expected cash flow.

When To Use P/CF

- Particularly useful for stocks that have positive cash flow but are not profitable

Pros

- Not easily manipulated. Cash flow is more difficult to manipulate than earnings, as it is not based on accrual accounting. The cash is what it is.

Cons

- Difficult to acquire future cash flow estimates. While earnings and revenue forecasts can easily be pulled for free from websites like Zacks, cash flow estimates remain less widely available, even though AI-assisted research tools have made them easier to access. The most comprehensive data still requires premium platforms such as Bloomberg or FactSet.

- Varying ways to calculate cash flow measures. This can create comparisons that are not apples-to-apples.

Price-to-Sales

Price-to-Sales or P/S is the stock price divided by sales per share. While earnings and book value ratios are generally more appropriate for large companies with positive earnings, the price-to-sales valuation ratio is often used as a comparative price metric for companies that don’t have positive net income—often young companies or those in trouble. Revenue relies less heavily on accounting practices than earnings and book value measures.

When To Use P/S

- Used for companies that don’t have earnings—fledgling companies that have yet to turn a profit as they are still in investment mode and cyclical companies like railroads or airlines, which may go through periods of unprofitable times.

Pros

- Less susceptible to accounting shenanigans. A metric like a book value requires accounting methods of depreciation and inventory valuation be considered (sometimes difficult to create an apples-to-apples comparison). Price-to-sales, on the other hand, is more difficult to fudge.

- Relatively stable metric. Revenue is (generally) more stable than something like earnings, which can be more volatile.

Cons

- It doesn’t take profitability into account.

EV-to-EBITDA

EV-to-EBITDA is the ratio of enterprise value to earnings before interest, taxes, depreciation, and amortization. Enterprise value (EV) is market capitalization + preferred shares + minority interest + debt—total cash. Essentially, the ratio tells you how many multiples of EBITDA (generally considered to be an easy-to-obtain proxy for cash flow, although there is some debate on that) someone needs to pay to acquire the business (EV is essentially equity value plus its debt less cash).

When To Use EV/EBITDA

- Good for capital-intensive industries where balance sheets hide a lot of the funding—airlines, railroads, etc.

Pros

- Incorporates the balance sheet.

Cons

- More difficult to compute. It takes more work to get to EBITDA (earnings before interest, taxes, depreciation, and amortization), and consensus estimates are still not as widely available as earnings or revenue forecasts.

Price-to-Book

Price-to-book or P/B is the ratio of price to book value per share. Book value is the value of an asset according to its balance sheet account—in other words, it is a company’s value if it liquidated its assets and paid back all its liabilities.

P/B is an indicator of market sentiment regarding the relationship between a company’s required rate of return and its actual rate of return. A ratio >1 means that the market thinks that future profitability will be greater than the required rate of return—assuming that book value reflects the fair values of the asset.

When To Use P/B

- Best for banks. Book value has less volatility than earnings, which can cause huge volatility in ratios.

- It can also be used during periods of negative earnings. If a company has several periods of negative earnings, they likely still have a positive book value.

Pros

- Stable metric. Given the relative stability of the base metric (book value), this ratio doesn’t fluctuate as much as others, such as P/E.

Cons

- Accounting differences can make it hard to compare. It becomes less useful when companies classify items on their balance sheet differently due to different interpretations of accounting rules. You want to be careful to compare firms with similar business models as it doesn’t make much sense to value firms with little tangible assets (tech firms, service providers) against those with lots of inventory or equipment (retailers, equipment sellers).

Which Valuation Ratio Is the “Right” One?

Valuation ratios can tell us so much about stocks, especially when you start comparing across companies, industries, and ratios. There isn’t necessarily one that can unlock the key. Take all of the puzzle pieces together, though, and you can uncover some interesting business drivers.

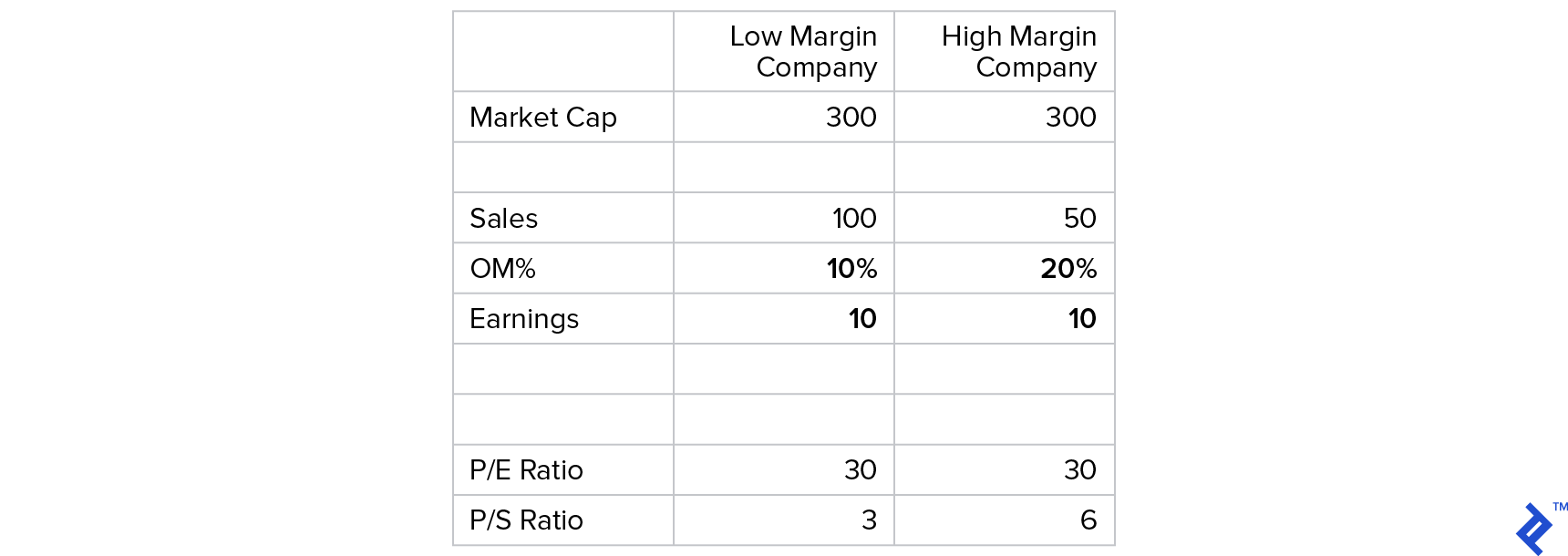

For example, imagine a home improvement retailer and a high-margin technology company trading at similar P/E multiples. However, on a price-to-sales basis, the retailer is quite a bit cheaper. What can we glean from this? What would the market be saying? Essentially, the market would be saying that each dollar of the technology company’s revenue is worth more because the company has a higher operating margin. If this weren’t the case, we could quickly spot a potential misstep in the market’s judgment.

You can see how the math works in the following table. While Low Margin Company and High Margin Company have the same market cap and P/E ratio, the High Margin Company has a significantly higher operating margin (20% versus Low Margin Company’s 10%).

So while there isn’t necessarily one “right” valuation ratio, taken together, with a little help from forensic valuation ratio analysis, we can learn a fair amount.

Further Reading on the Toptal Blog:

- C Corp, S Corp, LLC? Finding the Best Fit for Your New Business

- Unwrapping the Mysteries of Brand Valuation

- Fintech Valuation Methods for Money Transfer Disruptors

- How to Value a Fintech Startup

- Estimating WACC for Private Company Valuation: A Tutorial

- Equity Levels of Value: The Logic Behind Premiums and Discounts

Understanding the basics

Valuation analysis is the practice of determining an asset’s worth.

Generally, the most often used valuation ratios are P/E, P/CF, P/S, EV/ EBITDA, and P/B. A “good” ratio from an investor’s standpoint is usually one that is lower as it generally implies it is cheaper.

P/E ratio stands for price-to-earnings, meaning the market capitalization of an asset divided by its total earnings or net income. It is one of the most common market value ratios.

Elizabeth J. Howell Hanano, CFA

Annapolis, MD, United States

Member since October 3, 2017

About the author

Elizabeth was an equity research analyst on both the buyside and sellside before transitioning to freelancing where she specializes in market research and valuation.

Expertise

PREVIOUSLY AT