Modeling an Asset Class: Why Wall Street May Be in the Single-family Rental Market for Keeps

Wall Street has its eye on the single-family rental market. A convergence of rising home prices, changing rental preferences, and advancing technology is fueling the boom.

Wall Street has its eye on the single-family rental market. A convergence of rising home prices, changing rental preferences, and advancing technology is fueling the boom.

Hudson is a management consultant with a decade of experience organizing and investing in single-family housing funds. He has worked as a hedge fund equity analyst, portfolio manager, and startup advisor, and has deep expertise in financial modeling and forecasting.

Expertise

Previously At

Prior to 2010, the single-family rental market was largely ignored by big institutional investors, which preferred easy-to-scale multifamily properties. But since the financial crisis—and especially since 2019—that’s changed. Financial heavyweights like J.P. Morgan Asset Management, Blackstone, and Goldman Sachs Asset Management have helped bankroll an industry of more than two dozen single-family home rental companies that are snapping up existing properties—and building new ones too.

Residential real estate acquired by companies or institutions soared to 90,215 homes in the third quarter of 2021, as investors, both large and small, accounted for 18% of single-family home sales. That’s up 80.2% from the year prior, according to the online real estate firm Redfin. Nearly three-quarters of residential purchases by investors were single-family homes, while multifamily homes—a market in which investors have been significant players for decades—accounted for just a quarter of sales.

The influx of this institutional capital is one element driving the surge in single-family housing prices and rents across the US today, and despite negative media scrutiny, rising rents are attracting even more investors. While profit is clearly the investors’ goal, the evolving circumstances that now make single-family homes a desirable holding have implications for both the models used to make investment decisions and the way assets are allocated across their portfolios.

There are a number of reasons why institutional investors are buying single-family homes, including the Federal Reserve’s sustained monetary easing, which contributed to inflated real estate prices. However, having once managed a fund that invested heavily in single-family real estate, I believe the most consequential factor is an advance in big data, which significantly improves the ability of investors to conduct due diligence and forecast trends.

The dramatic increase in computing power is enabling these new home-rental firms to scale and manage their portfolios more efficiently, not only enhancing the ability to analyze the market, speed up research, and make smart decisions more quickly, but also streamlining costs associated with property management. This convergence of market conditions and increased analytic power means these investors are likely here to stay.

The Birth of a New Investment Class

This push into single-family homes initially began as an arbitrage opportunity after the global financial crisis in 2008 but has morphed into something more permanent. The real estate bust lowered the perceived risk of single-family housing relative to returns. Today, real estate investment trusts, private equity firms, insurance companies, and pension funds view rentals, which were spared the impact of pandemic-related lockdowns on offices and shops, as a relatively high-yielding hedge against inflation.

I witnessed the initial opportunity in real time. In 2010, I helped create a fund that bought a few hundred in-foreclosure single-family homes in Atlanta for between $50,000 and $60,000 each, and invested as much as $10,000 per home for upgrades before renting them. By acting quickly, we were able to earn double-digit returns from near the bottom of the cycle as valuations reverted back to the mean. We had no evictions and sold the last of the houses in 2020.

Institutional investors did much the same, pouring money into broken markets and reaping huge gains before realizing they could make single-family rentals a permanent part of their portfolios. In 2012, Blackstone, one of the world’s largest alternative asset managers, acquired Invitation Homes, which controls more than 80,000 rentals. Blackstone cashed out in 2019 after Invitation Homes went public. In 2021, Blackstone acquired Home Partners of America, a company with more than 17,000 rent-to-own units across the US, for $6 billion.

In 2020, J.P. Morgan Asset Management entered into a joint venture with a single-family rental company, American Homes 4 Rent, and is now building thousands of homes. Goldman Sachs has deployed capital in residential markets both in the US and in England. Other money managers that have jumped in include Invesco, which in 2021 announced it was backing a plan by Mynd Management to spend as much as $5 billion purchasing 20,000 single-family rental homes over the next three years.

This influx of capital is motivated, at least in part, by the returns this sector is generating. The COVID-19 pandemic led to a shift of preferences away from apartments in cities toward houses with more space. As a result, since 2019 single-family rentals have been the best-performing property class, gaining about 40% in 2021, according to the Connecticut-based firm Hoya Capital Real Estate. The three publicly traded real estate investment trusts the firm tracks—Invitation Homes, American Homes 4 Rent, and Tricon Residential—have reported double-digit rent growth and record occupancy rates in 2021, driven by historically low supply and strong demographic- and pandemic-driven demand.

How Tech Is Boosting the Single-family Rental Market

Wall Street is not new to the real estate game. Multifamily rental properties have long been considered a core portfolio holding for institutional investors, along with other scalable commercial properties like office, retail, and industrial buildings. All of these can absorb the sizable capital outlays these firms deploy to acquire them. But single-family rentals were traditionally classified as non-core—grouped with other specialty properties such as data centers, medical offices, hotels, and senior housing—because they were more difficult to scale. Thanks to technology, that’s no longer the case.

Property technology is transforming more than just single-family rentals, but the impact in that sector is particularly profound. Whereas the due diligence for multifamily properties is, by definition, already scaled, single-family properties are more idiosyncratic, making the process for potential buyers more costly per unit. What is changing is that investors are deploying big data technology that lets them filter diligence information much more quickly, making otherwise fractured markets more efficient and accessible.

Niche players like the firm Entera—backed by Goldman Sachs—have emerged, using technology to analyze property records and other data to help investors quickly identify real estate listings that match their buying criteria and help them calculate the right bids. These capabilities are enabling institutions to obtain more accurate return forecasts for their models and to scale their property holdings.

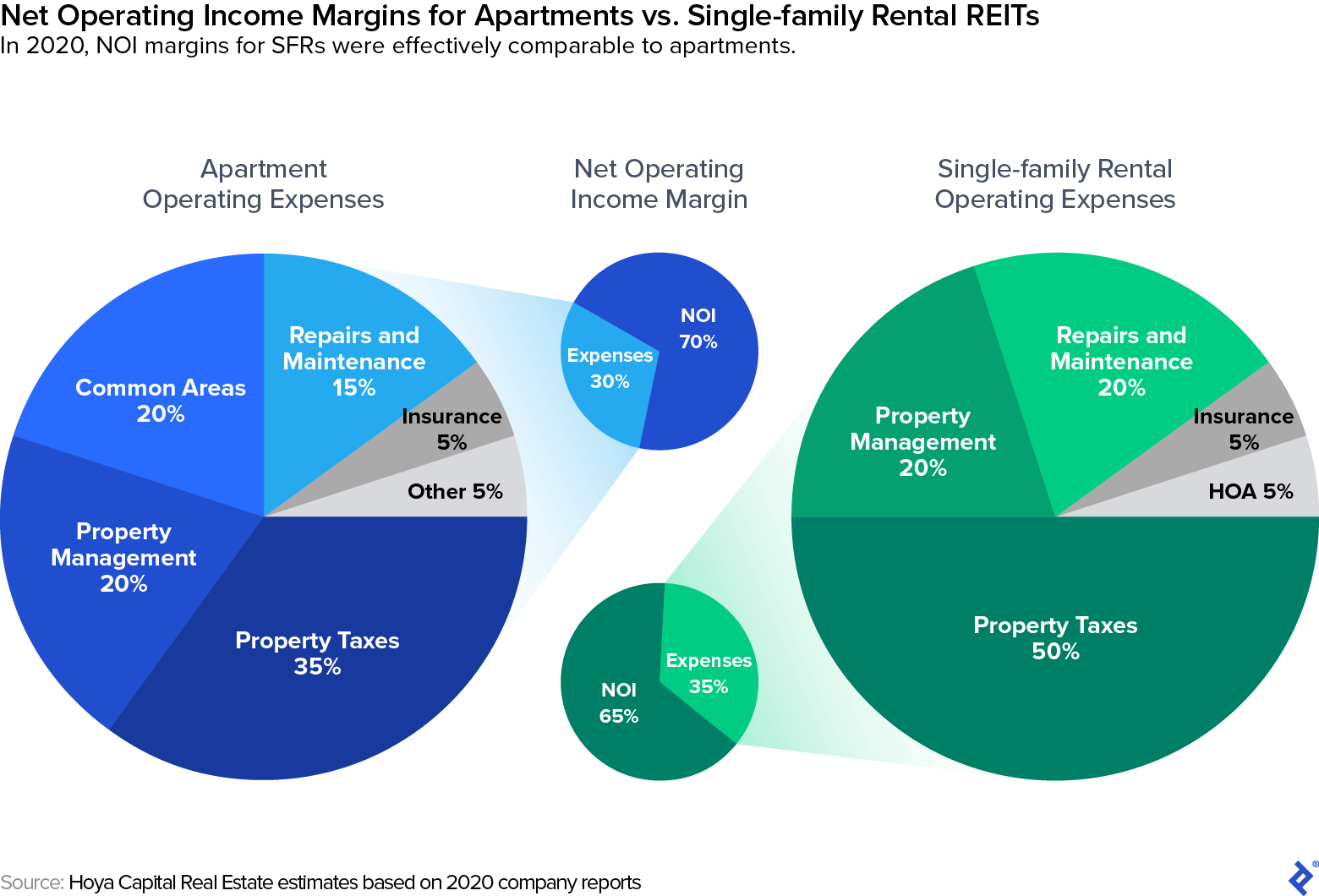

The transformation extends through single-family portfolios, with many landlords using fully digital relationships with tenants to facilitate everything from payments to maintenance requests in an effort to reduce costs, improve renter satisfaction, and fuel growth, according to Hoya Capital. The result is that institutions can achieve net operating income margins nearly on par with multifamily real estate investment trusts, the firm reports.

“We use technology in every aspect of our business, everything from acquisition all the way through maintenance and into the call center to improve our operating metrics and offer residents a much better experience,” Tricon Residential’s chief executive officer Gary Berman told the financial news service Seeking Alpha in October 2021. Tricon Residential manages 33,000 properties across North America.

Tech can’t solve every real estate problem, of course. A new class of so-called iBuyers pushed the role of automating decision making to the extreme, deploying computer algorithms to execute purchases and sales in order to flip single-family homes—a strategy that failed spectacularly for the firm Zillow. Best known for publishing real estate listings online and calculating estimated home values, Zillow was forced to shutter its new purchase-and-flip program and put 7,000 homes on the market in November 2021 after it found it had aggressively overpaid for properties.

By contrast, the fund I managed was able to sell off its properties in an orderly fashion at significant profit. At least for now, I believe some human perspective is still advisable.

Wall Street’s Real Estate Market Impact

How big an effect these Wall Street-backed firms will really have remains to be seen, however. They currently represent just 2% of the total residential market, according to analysts with broker-dealer Amherst Pierpont, which specializes in fixed-income capital markets. And there may be limitations built into this class. Single-family rental companies tend to focus primarily on faster-growing regions in Western, Southwestern, and Southeastern states, buying and building homes that target largely middle- and upper-middle-class families. Supply is a constraint too, so investors’ focus has begun shifting increasingly to build-to-rent.

Still, acquisitions by investors are continuing apace. The collective realization that due diligence efforts could scale has not only brought many financial institutions into the market, it’s also produced record issuance of debt secured by portfolios of single-family rentals, increasing liquidity for institutional financings by spreading the risks. The cumulative public issuance of so-called SFR debt reached a record $43 billion in 2021, according to Amherst Pierpont.

In addition to reduced diligence costs, there are other elements that have made these SFR deals attractive to lenders. Collateral value is a key component of any securitization model, and single-family securitizations are ultimately secured by the value of the homes, which are rising significantly in the wake of growing preferences by renters for houses.

Given all these factors, I expect SFR securitizations to accelerate. 2021 was the first full cycle for this particular surge in securitizations and the performance has been stellar, trading comparably with other structured debt. Wall Street is eager to originate as many securitizations as investors can digest, and the appetite is large right now because rents are going up and investors predict that risk and interest rates will stay low for the foreseeable future.

Nonetheless, there are risks to consider, interest rates looming large among them. Unlike owner-occupied homes, which are typically financed with 30-year loans, SFR portfolios are usually financed with shorter terms, similar to commercial real estate. In the event that interest rates rise considerably, the net rental yield might be completely erased when it’s time to sell or refinance. This is similar to the inherent risks of commercial mortgage-backed securities, which is why the industry views SFR debt similarly.

Another complicating factor is the variability of maintenance and upkeep of the homes, which could also potentially eat into cash flows. Should interest rates and maintenance costs rise considerably, there’s a risk that a wave of investors selling into an illiquid market could cause prices to fall and debt to be marked down, thus creating a negative feedback loop with forced sales, as we saw in 2008.

One additional risk that’s difficult to quantify is the growing scrutiny institutions are facing after initially flooding the single-family market. Several media outlets have painted Wall Street-backed landlords as inept or even villainous, accusing some of these investors of driving up home prices, jacking up rents, or doing a poor job with maintenance and upkeep. Suffice it to say, SFR is an enterprise that needs to be conducted with great care and professionalism because it touches people’s everyday lives so deeply.

Wall Street Landlords Are Here to Stay

Although Wall Street-backed firms only account for an estimated 300,000 of the more than 128 million single-family homes in the US, SFR looks like an asset class that’s poised not only to stay, but to grow.

Near-zero interest rates and current demand in the single-family rental market add fuel to the growth. Surveys show that an increasing percentage of millennials are planning to rent for the foreseeable future, with a growing proportion opting to lease single-family homes instead of apartments. Meanwhile, the robust growth of big data suggests it will be an increasingly powerful tool for investors in coming years.

Despite the controversy, Wall Street is likely to play buyer and builder for a long time to come.

Further Reading on the Toptal Blog:

Understanding the basics

Wall Street is buying more single-family rental homes because demand for houses is high, renters’ preferences are shifting away from apartments, interest rates are low, and big data is making it easier than ever for firms to conduct due diligence and manage these properties.

Invitation Homes is the largest single owner of single-family rental homes in the United States, managing more than 80,000 homes as of 2021.

A single-family home is a standalone residential structure that contains only one dwelling unit.

Hudson Cashdan

New York, NY, United States

Member since April 3, 2017

About the author

Hudson is a management consultant with a decade of experience organizing and investing in single-family housing funds. He has worked as a hedge fund equity analyst, portfolio manager, and startup advisor, and has deep expertise in financial modeling and forecasting.

Expertise

PREVIOUSLY AT