Name Your Price: 4 Counterintuitive Pricing Strategy Tips

High inflation means it’s crucial for managers to pay closer attention to pricing. Toptal management consultant Kalil Rodrigues shares four outside-the-box tips for optimizing your pricing strategy.

High inflation means it’s crucial for managers to pay closer attention to pricing. Toptal management consultant Kalil Rodrigues shares four outside-the-box tips for optimizing your pricing strategy.

Kalil is a corporate strategist, management consultant, and business consultant. An alum of Bain & Company and global aerospace firm Embraer, he has also led strategic initiatives at Nubank, a Latin American fintech leader with more than 50 million customers across Brazil, Mexico, and Colombia. Kalil is an expert in pricing models, revenue and expense projections, forecasting, financial modeling, and mergers and acquisitions.

Expertise

Previously At

Pricing strategy is always a critical component of business strategy, but it’s even more important in a volatile economy. Thanks to exploding consumer demand, supply chain disruptions, and easy monetary policy, inflation is rising rapidly around the globe. According to the latest data from the US Bureau of Labor Statistics, the US Consumer Price Index rose 9.1% from June 2021 to June 2022—the highest year-over-year increase of the last 40 years.

Experts disagree about how long global inflation will last, making it especially difficult to price products competitively today without undermining profits. If there was ever a time to thoroughly examine your pricing techniques, it’s now.

I started my career as a consultant at Bain & Company, where I worked on pricing projects for companies of all sizes and scales across many geographies and a wide range of industries. Later, when I became a freelancer, I chose to focus on pricing. And throughout, all too often what I’ve seen are thoughtfully developed, complex pricing models and pages of detailed data analysis that ultimately fail to create any real value.

Why? In many cases, it’s because people don’t actually understand the fundamental principles of pricing strategy or appreciate the complexity of the contextual variables that factor into it.

For example, many pricing models depend heavily on historical sales data and customer behavior. But these aren’t likely to be useful in new situations like a global pandemic or a war.

To create and maintain an effective pricing strategy, management teams need to continually adapt their models to better fit ever-evolving macroeconomic circumstances and consumer preferences. The projects that I see succeed and drive substantial margin gains for their companies are generally those where the team truly understands the underlying principles behind their pricing strategy as well as the psychology and behavior of their customer base, and pays ongoing attention to the interaction between those forces.

In this article, I’m going to share four types of pricing strategies to help your team accomplish this. They may appear counterintuitive, but they’re drawn from my experience, and supported by independent research. I think they’ll be helpful to any company looking to develop a functional and flexible pricing model and keep it up to date.

Pricing Strategy Tip No. 1: It’s Not Always About Being the Cheapest

Intuitively, you might think that the best way to beat your competitors is by undercutting their prices. That’s because the basic economic framework underlying any pricing strategy assumes a tradeoff between price level and sales volume. If there is consumer demand for your product, all other things being equal, decreasing its price should result in greater sales volume. But pricing isn’t necessarily that simple.

In 2021, the Boston Consulting Group’s Center for Consumer Insights conducted a study in which it asked 41,000 consumers around the world about their spending habits and found that, depending on the purchases they were asked about, 70% to 90% of those surveyed identify themselves as “value conscious” (defined as always carefully considering price before spending money). However, this self-designation didn’t always translate into their actual purchasing behavior. When asked about their most recent purchase in a wide range of consumer goods and service categories, only a small number of those surveyed had actually bought the lowest-priced item—in most cases, less than 15%.

The key takeaway I want to highlight here is that the amount of value that individual consumers attribute to a product is subjective. Consumers are often willing to pay a slightly higher price for a product that they perceive as more valuable. To many shoppers, price can serve as an indicator of quality or confer a certain status. One person might be happy to pay a few dollars extra to enjoy a morning cup of premium Starbucks coffee, while another might be just as pleased drinking Nescafé and saving a few bucks. Context and conditions are crucial factors to consider when developing a pricing strategy for products.

Case in point: In my early years at Bain, I conducted pricing research for a large retailer in Brazil. One of our most interesting findings was that there were large offer gaps in many segments of the cosmetics market—meaning most available products were clustered either at the high or low end of the price spectrum, with relatively few offerings in between.

Large-scale producers often focus on being the cheapest in an effort to capture a greater share of the market, and this is exactly what we found. Most of the larger players had positioned their prices too low—to the point that their products were perceived as cheap and poor quality. At the same time, many of the smaller niche players had set prices so high that they were simply out of budget for the middle class, who comprised the vast majority of the market.

This indicated a previously untapped opportunity with huge revenue potential for our client—targeting this “masstige” segment. We could develop products that had similar production costs to the lower-priced offerings, and we would increase sales simply by pricing them a little higher so that they were perceived as higher quality. Discovered through what started as a simple benchmarking effort, this product development insight led to significant increases in margin.

I would argue that the same concept holds true for almost any product—from B2B software to manufactured goods. Because pricing has such a significant effect on consumer perception, it’s necessary to strike the right balance between appealing to cost-conscious consumers and to those who prioritize quality.

Pricing Strategy Tip No. 2: Don’t Assume Promotions Equal Profits

Done properly, promotions can be a great way to boost revenue. Many consumers have even come to expect sales and discounts at certain times of the year. However, I’ve seen firsthand that companies can easily become too reliant on promotions, which can ultimately destroy value.

In 2018, one of the largest premium furniture retailers in Brazil brought me on as a pricing manager to help it find ways to increase revenue. With this aim in mind, the company had already created a promotional calendar that initially increased revenue without cutting into overall margins. But as the revenue goals became more aggressive, so did the promotions, and I noticed a troubling pattern emerge in the data. The company was experiencing a noticeable drop in sales numbers after each promotion.

The business tried to compensate for this “hangover effect” by adding even more promotions to the calendar, a tactic that led to a vicious year-round promotional cycle. These promotions were tarnishing the brand’s image with its primary customer base, undermining the value of the product, and effectively training consumers to postpone purchases until the next sale.

After hearing our findings and recommendations, a courageous executive decided to put an end to the cycle. Some promotions were kept but many were scrapped, and the company directed greater effort toward creating more personalized offers based on customer segmentation, which generally has less of a negative effect on margins.

Research also supports the need to handle promotions with care. After surveying more than 1,000 leading consumer companies about their pricing practices in 2019, Bain found that most of the top performers in terms of market share growth had a few tactics in common. Among these were using data to continually fine-tune their strategies and quickly finding and killing the “bad promotions”—defined as those that hurt profitability, damage the brand, or fail to significantly increase sales. These findings reinforce my point that promotions should be approached scientifically, not treated as an easy way to create a quick bump in sales.

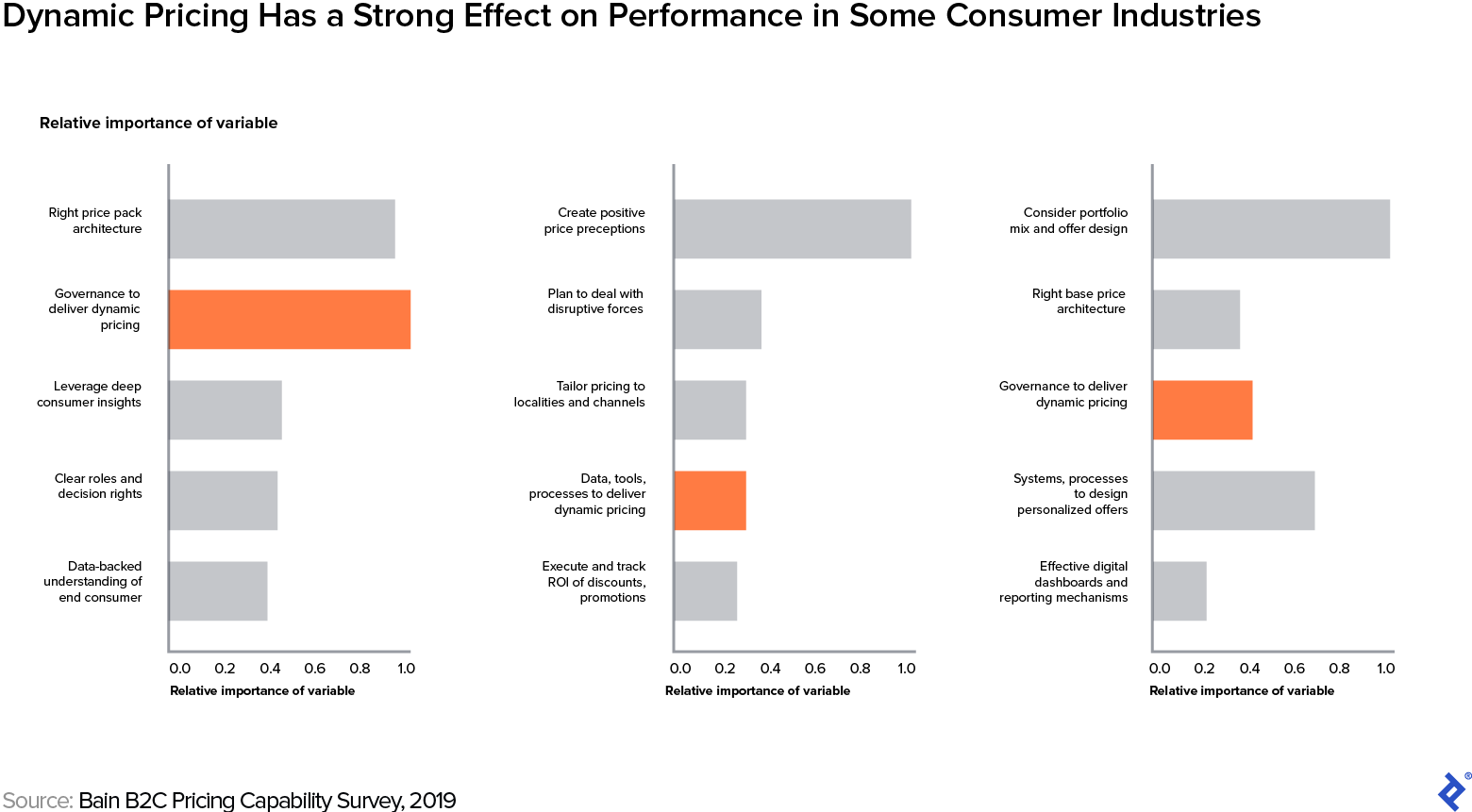

Pricing Strategy Tip No. 3: Dynamic Pricing Isn’t Just for Airlines

You might think that dynamic pricing is limited to the travel and e-commerce industries, but it’s also gaining footholds elsewhere. For instance, the producers of The Lion King effectively used dynamic pricing strategies to make it the highest-grossing show on Broadway in 2013, and many ride-hailing companies today use “surge” or “demand” pricing to increase profits during rush hours.

Although it’s probably not a great idea to change the prices of your B2B SaaS platform every time a client logs in to your website, a wide range of industries can incorporate some principles of dynamic pricing into their approach.

Service providers like consulting firms and enterprise software companies already use dynamic pricing practices, but they don’t call them that. These businesses generally rely on proposal-based pricing—a form of value-based pricing in which the price quote for providing a particular product or service is tailored to a customer’s needs and their perceived value of that product or service. This may not be a textbook definition of dynamic pricing, but the spirit and the effect are similar.

Brick-and-mortar retail businesses can also take advantage of dynamic pricing principles—as long as they do so carefully. For example, a customer might be turned off by price changes for staple items, but not mind them as much when it comes to trendy or one-off purchases. And as with any pricing experiment, retail businesses must test and refine their strategies to ensure the optimal outcome.

By reconsidering the pricing question frequently and with some scientific rigor, you can manage it in a more dynamic way—potentially generating meaningful margin increases regardless of the size and scope of your company.

Pricing Strategy Tip No. 4: The Most Valuable Thing You Can Get From a Price Change Is Information

This last tip can go against the grain of companies that view maximizing short-term profit as the only objective of pricing strategy. But a well-structured price change can generate more than just margin gains. It can translate into actionable insights and valuable market knowledge that are vital components of profitability and competitive success over the long term.

The prices of seemingly everything, including basics like groceries and electricity, are rising right now, so it’s easy to see how a CEO might think the best course of action is increasing prices to pass these costs on to the consumer. But that would be wasting a valuable chance to develop a better understanding of your customers’ preferences and purchasing behaviors by taking a more disciplined, responsive approach to price setting.

Nowadays, many processes are “data-driven” or “evidence-based,” from marketing efforts to public policy decisions, and your pricing strategy probably is as well—but most likely not to the extent that it needs to be. The more information about your market, competitors, and customers you can acquire and use to continually update and optimize your strategy, the more effective your pricing will be. But the results of analytics are only as good as the data itself. Even the most sophisticated pricing models will fail if they’re fed garbage data. And unfortunately, there’s a lot of it out there.

Many traditional industries used to perceive data not as a valuable asset, but more as an afterthought—something kept primarily for regulatory purposes and stored as easily and inexpensively as possible. Unstructured data—qualitative and/or difficult to parse—and polluted data are still the sad reality for many companies. In my experience, although you need data to inform your strategy, you will almost never have all the right data exactly as you would like it. As a consultant and a freelancer, most of my time and my team’s has been spent “scrubbing” the data that we’ve been provided in order to be able to turn it into something that we could use to conduct any meaningful analysis.

Rather than getting overwhelmed, I recommend taking an 80-20 approach to cleaning the data you have before using it as the basis for price changes. Focus your efforts on cleaning the data sets that are likely to have the biggest impact on your company’s most profitable products or segments. If you wait for all the data to be thoroughly cleaned, you may be waiting forever.

The point I want to emphasize is that the best thing you can do is take advantage of every opportunity you have to collect good data. You’ve probably noticed that for all of these tips, I’ve emphasized the need to observe, evaluate, and refine. Like so many areas of business strategy, pricing strategy isn’t something you can think about once, set in motion, and leave to its own devices. As conditions change, so must your approach.

But those changes need to be strategic, based on the data you have and designed to get you still more valuable information about your market and your customer. Instead of just raising prices, consider segmenting your customer base and applying different raises to each segment so that you can compare how different customer types react. Or you could try applying the higher price to one customer group and monitoring the effect on churn.

In retail, applying a different approach to each product category will most likely deliver the most helpful insights. For enterprise software companies, breaking your product down into smaller component parts and conducting pricing experiments on individual features might increase your knowledge of customer preferences. For SaaS companies, usage-based pricing is the latest growth strategy. However you proceed, tracking how your customers respond to price changes in a structured and intentional way can give you the information you need to refine your strategy to effectively maximize revenue and retention.

During volatile economic times, all businesses need to take a closer look at their prices to maintain profitability. Setting prices too low or overusing promotions and sales can shift consumer perceptions and behavior in counterproductive ways, while raising prices willy-nilly can alienate customers and reduce sales volume. The most successful businesses constantly reevaluate their pricing strategies and thoughtfully experiment with price changes grounded in good data. Yours should do the same—and I hope these pricing strategy examples have helped show you how.

Further Reading on the Toptal Blog:

Understanding the basics

Pricing is a primary determinant of profitability and can affect consumers’ perception of your product and brand.

Developing a pricing strategy involves choosing a method—such as cost-plus pricing (pricing based on cost plus a markup)—and creating a model to determine the best price to charge for a product or service based on a variety of factors. These include your market, competitors, and customer base. Models should be continually refined using data-driven insights.

Pricing strategy is a science and an art. Among the many challenges involved are balancing healthy profit margins with sufficient sales volume and keeping pace with varied and ever-evolving consumer preferences.

Kalil Gebrim Rodrigues

São José dos Campos - State of São Paulo, Brazil

Member since January 13, 2022

About the author

Kalil is a corporate strategist, management consultant, and business consultant. An alum of Bain & Company and global aerospace firm Embraer, he has also led strategic initiatives at Nubank, a Latin American fintech leader with more than 50 million customers across Brazil, Mexico, and Colombia. Kalil is an expert in pricing models, revenue and expense projections, forecasting, financial modeling, and mergers and acquisitions.

Expertise

PREVIOUSLY AT