How to Prepare a Cash Flow Statement: Building a Model That Actually Balances

When a cash flow statement doesn’t balance, it can cause frustration and waste time. In this article, a Toptal management consultant with experience at PwC describes how to prepare a statement that always tallies correctly.

When a cash flow statement doesn’t balance, it can cause frustration and waste time. In this article, a Toptal management consultant with experience at PwC describes how to prepare a statement that always tallies correctly.

Pierre is a corporate finance, PE, and FP&A expert with extensive experience in complex financial modeling, translating entrepreneurs’ ideas into robust business plans, and leading in-depth financial due diligence. He has assisted with more than 60 transactions globally, mainly in the retail, SaaS, and technology spaces.

Previously At

To create a cash flow statement that always balances, you need consistent data. Your financial model must correctly link to the income statement, balance sheet, and profit and loss statement (P&L), and discrepancies among data sources that feed the model must be found and fixed.

For example, inconsistencies commonly arise across CRM systems, ERP platforms, CapEx schedules, or inventory reporting metrics, which can cause significant imbalances in your model.

I have worked on several financial due diligence projects for M&A deals where data provenance was a problem. These inconsistencies create doubt about the soundness of the transaction, and rectifying them adds unnecessary costs and labor to the deal. While many finance teams use cloud-based accounting systems and automated reconciliation tools to help identify these issues earlier, the underlying principles behind preparing and validating a balanced cash flow statement remain the same.

In this article, I share my step-by-step method for how to prepare a cash flow statement that always balances and tallies, and demonstrate the central role balance sheet accounts and net working capital (NWC) play.

For reference, here is a sample cash flow statement model that demonstrates the required interconnectivity.

What’s the Best Way to Prepare a Cash Flow Statement?

The most popular way to prepare a cash flow statement is from the balance sheet and P&L. This is known as the indirect method of cash flow, and is simpler and more widely used than the direct method, which relies on actual cash inflows and outflows from the company’s operations.

Cash Flow Statement Preparation in 4 Steps

As I take you through each step, I’ll explain the interconnectivity between the different lines of the cash flow statement and demonstrate the central role balance sheet accounts and net working capital play.

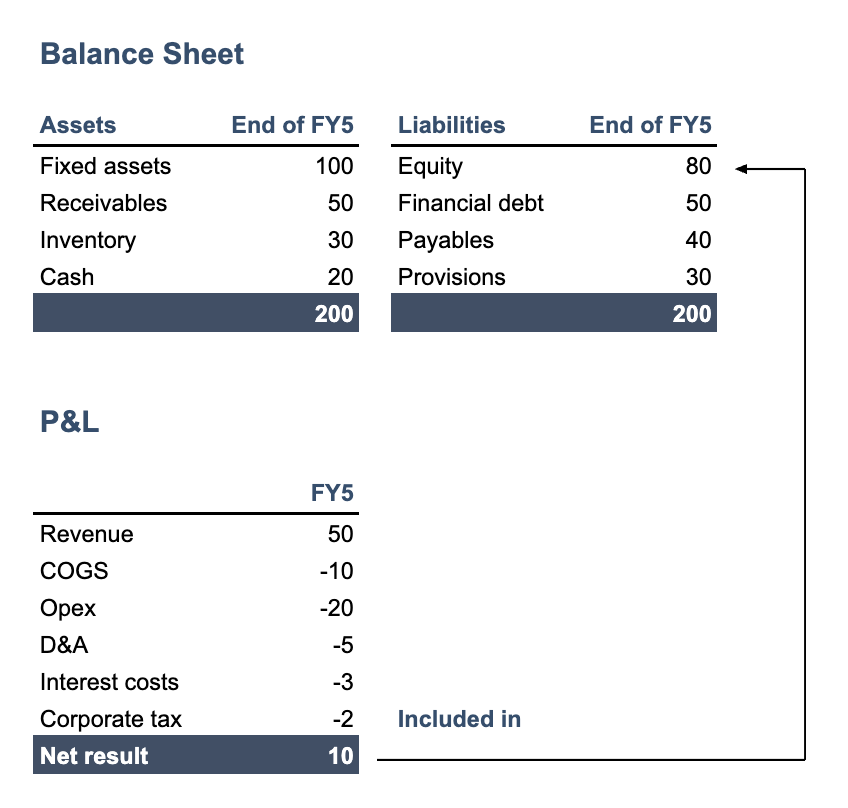

Step 1: Link the P&L and Balance Sheet

The P&L and balance sheet are connected via the equity account in the balance sheet. Total assets must always equal total liabilities (and equity). Any debit or credit to a P&L account will instantly impact the balance sheet through being booked on the retained earnings line.

Step 2: Express Cash As a Sum and Subtraction of All Other Accounts

Because total assets always equal total equity and liabilities, we know:

Fixed Assets + Receivables + Inventory + Cash = Equity + Financial Debt + Payables + Provisions

Basic arithmetic then allows us to deduce:

Cash = Equity + Financial Debt + Payables + Provisions - Fixed Assets - Receivables - Inventory

This also means that the movement of cash (i.e., net cash flow) between two dates will be equal to the sum and subtraction of the movement (the delta) of all other accounts:

Net Cash Flow = Δ Cash = Δ Equity + Δ Financial Debt + Δ Payables + Δ Provisions – Δ Fixed Assets – Δ Receivables – Δ Inventory

Step 3: Break Down and Rearrange the Accounts

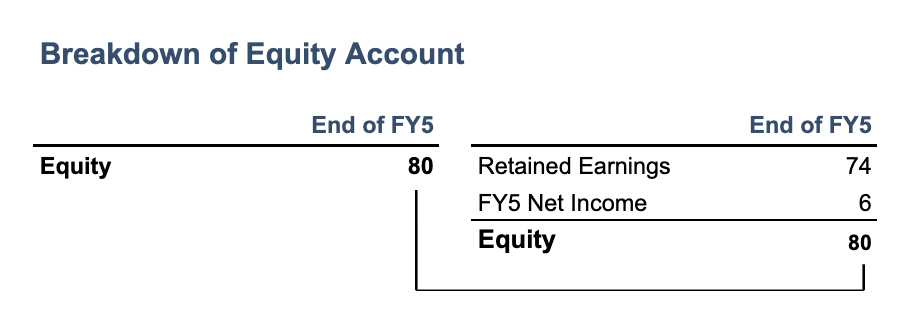

First, break down the equity account to find net income. Assuming we’re looking at a balance sheet before any dividend payments, the equity account will include the current year’s net income. We’ll have to break down the account more granularly to make the current year’s net income appear clearer.

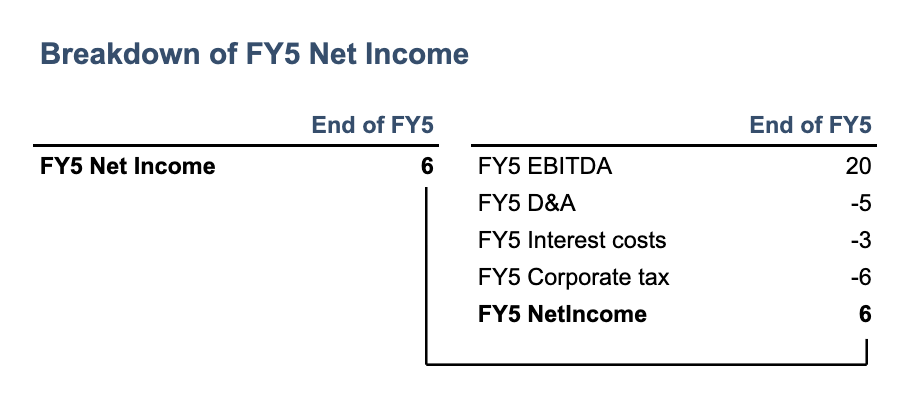

Break down net income. The line item of net income is made of constituent parts: EBITDA minus depreciation and amortization (D&A), interest, and tax.

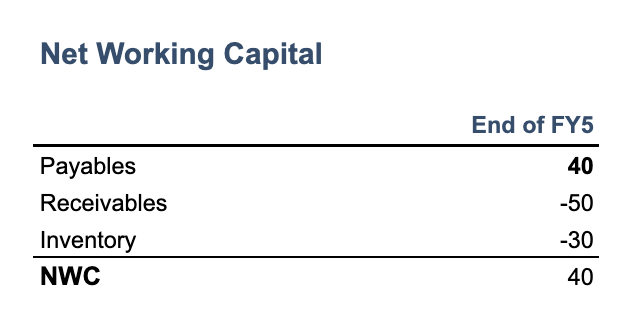

Calculate NWC movements. NWC consists of three elements: inventory (on the asset side), receivables (on the asset side), and payables (on the liability side). When netted off against one another, they equal the net working capital position, which is the day-to-day capital balance required for running the business. An increased balance movement on a working capital asset constitutes an outflow of cash, while the inverse applies to their liability counterparts.

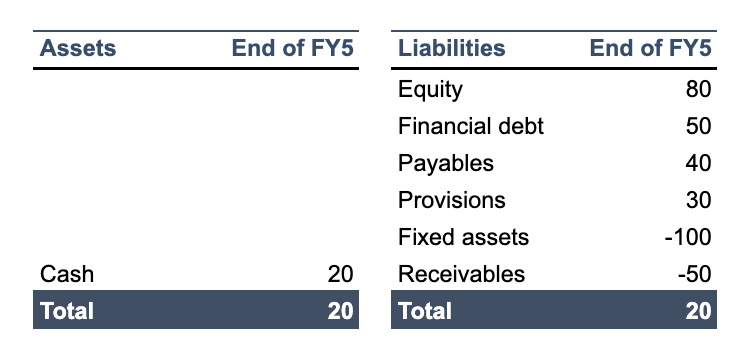

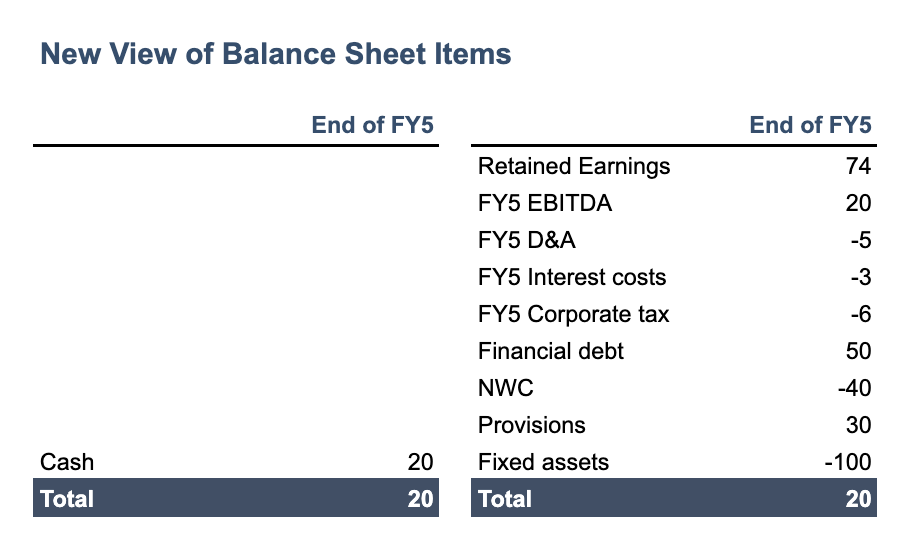

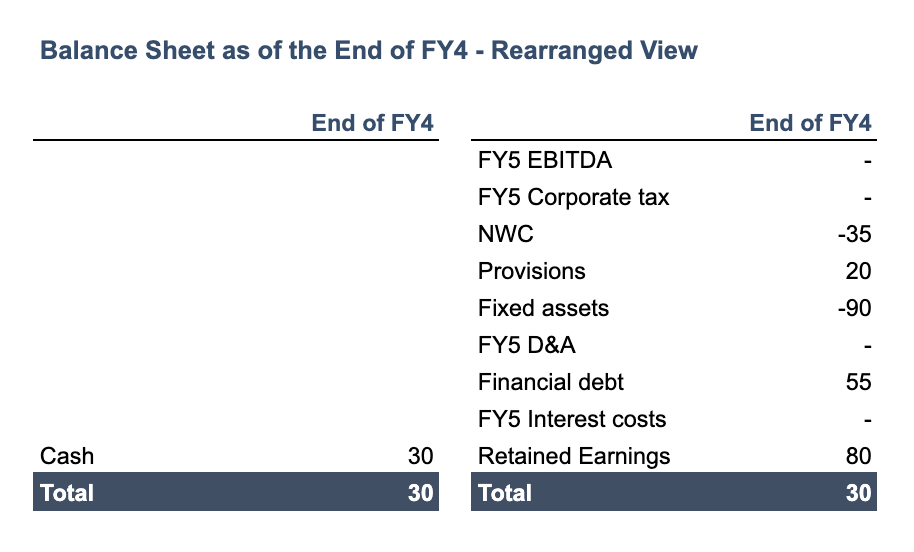

Create a new view of the balance sheet items. If we aggregate all of the changes we have just made, they will come together in the following order:

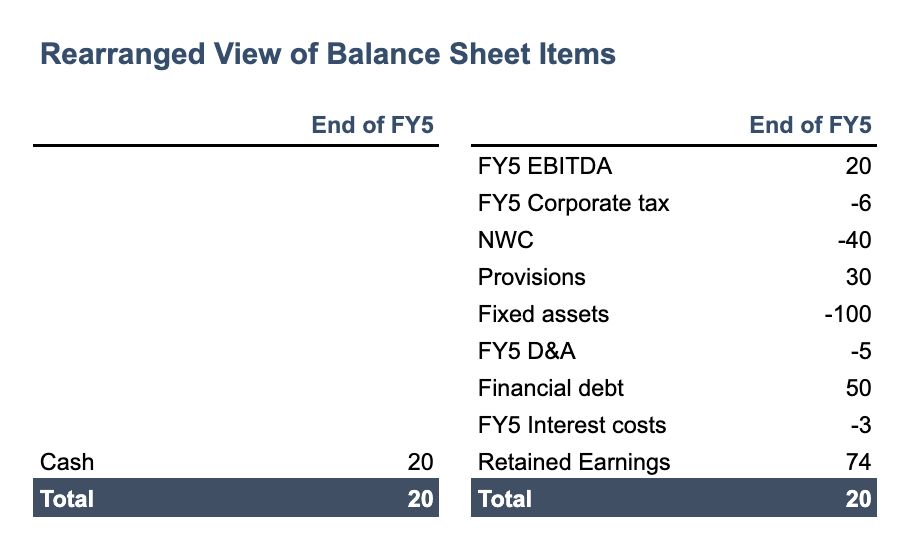

This looks a bit haphazard, so re-order these lines to mirror a traditional cash flow statement format for easier reference:

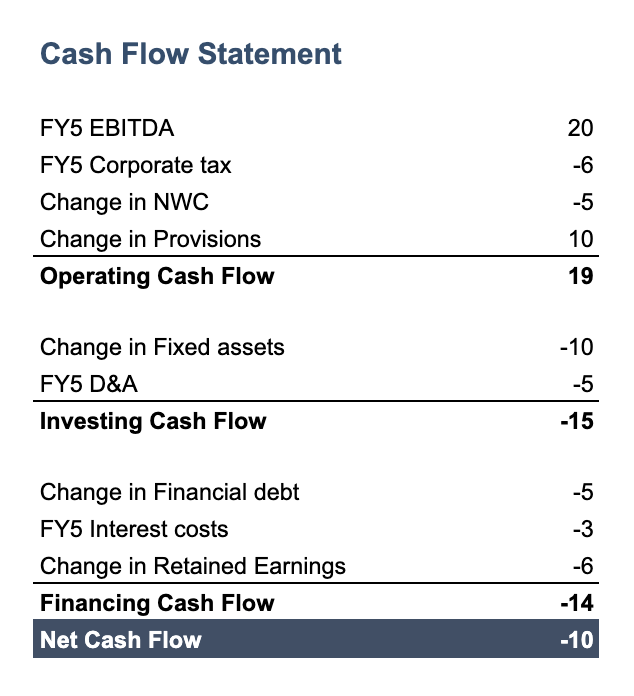

Step 4: Convert the Rearranged Balance Sheet Into a Cash Flow Statement

We have been using just one balance sheet position: the balance sheet as of the end of FY5 in our example. To calculate cash flow over a period of time, we need a second balance sheet from an earlier date. I’ve chosen a balance sheet from the end of FY4, before the distribution of that year’s dividends.

There are two points to consider here:

- As of the end of FY4, FY5 had not yet begun—therefore, all FY5 P&L-related accounts will be equal to zero.

- The retained earnings figure here will include the FY4 net income.

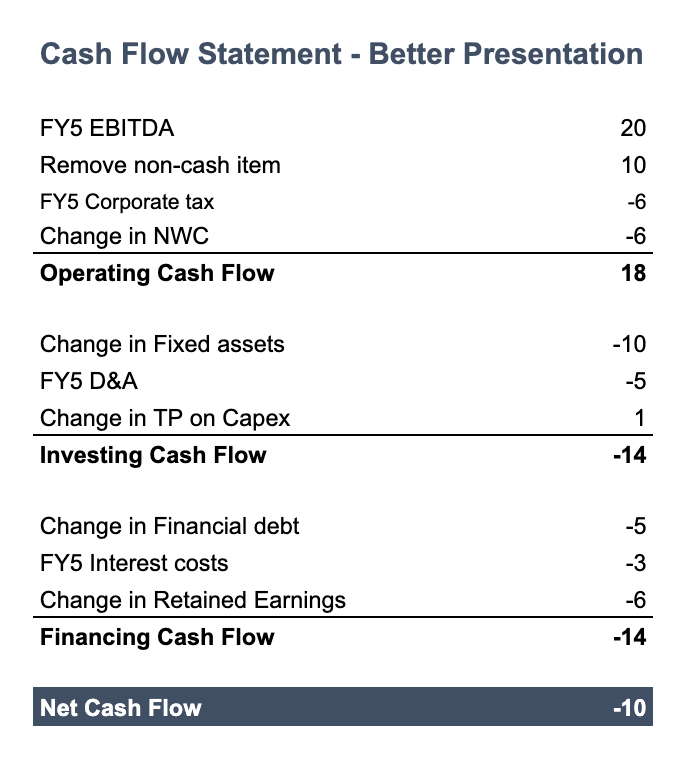

In order to calculate a statement of cash flows, we will need to look at the movements between the end of FY4 and the end of FY5. Thanks to the equality that we demonstrated in Step 2, we already know that the net cash flow will be equal to 20 - 30 = -10.

By taking the movement between the two balance sheets’ positions and adding subtotals for clarity of presentation, we have now created a dynamic and balanced cash flow statement:

How Can You Make Sure a Cash Flow Statement Is Correct?

To ensure a cash flow statement is accurate, all accounts must be correctly categorized, and net working capital and EBITDA must be analyzed together.

Correctly Categorize Accounts

This is a forensic exercise that will require you to look over every line account used in your accounting software. Once you’ve analyzed them, discuss with the financial controller or CFO any discrepancies of opinion over the correct classification of items.

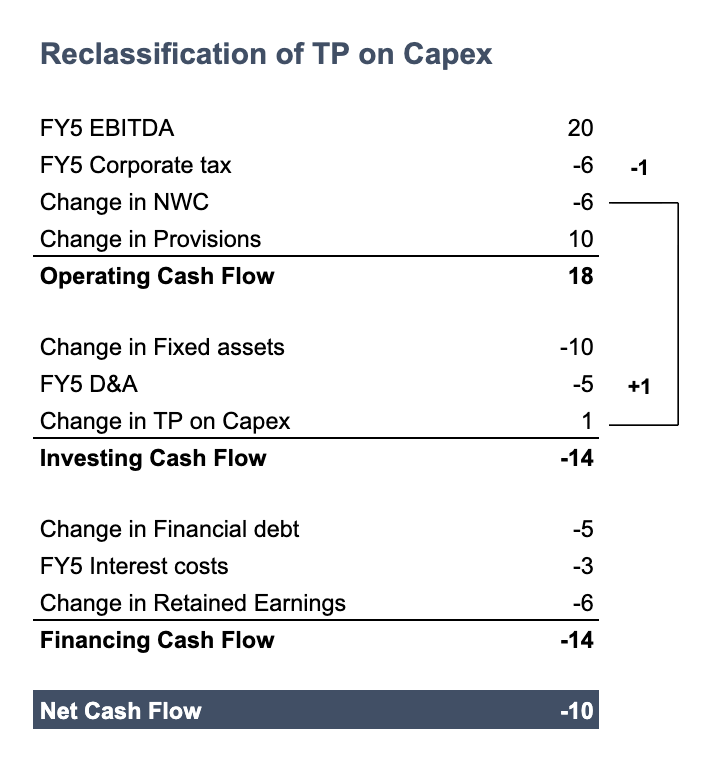

A common miscategorization is trade payables on CapEx (i.e., outstanding payments due to fixed asset providers). This account commonly gets included in the trade payables in current liabilities, and gets incorrectly classified as net working capital. If this is the case, you will need to remove it from NWC and add it to the investing section.

In our example, assuming a movement of trade payables on CapEx of +1 between FY4 and FY5, we would make the following changes to our cash flow statement:

Make Sure Your Statement Represents Actual Cash Inflows and Outflows

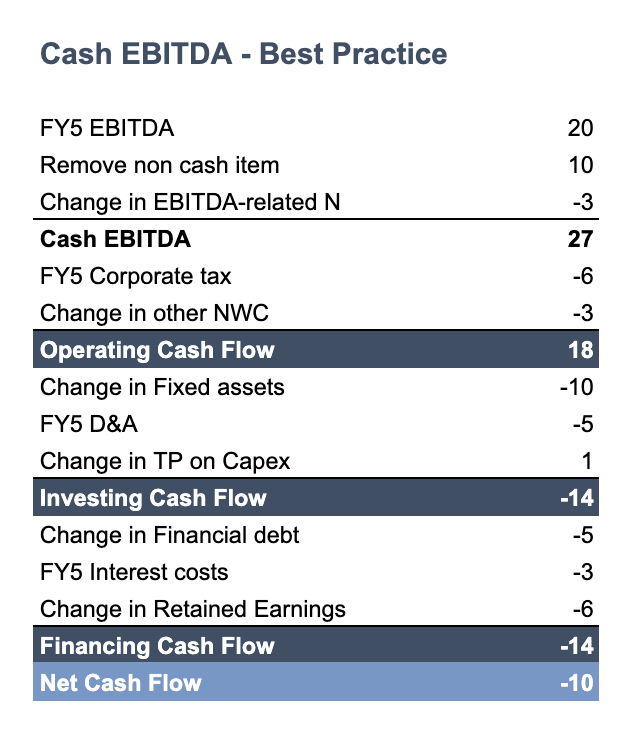

The notion of cash and non-cash can be confusing. For example, if Company A purchased an item for $10 last year and sold it for $40, but has still not received payment from the customer, what amount should you consider “cash EBITDA?” Should it be $30—revenue less cost of goods sold, assuming no other operational expenses? Or should it be $0, considering that the item purchased was paid for last year and no proceeds have been collected yet?

This is why NWC and EBITDA should be analyzed together when looking at cash generation. When EBITDA is impacted by a so-called “non-cash item,” there’s always a balance sheet account concomitantly impacted. Your responsibility when building a statement of cash flows is to understand which one. The answer often lies within the accounts included inside net working capital.

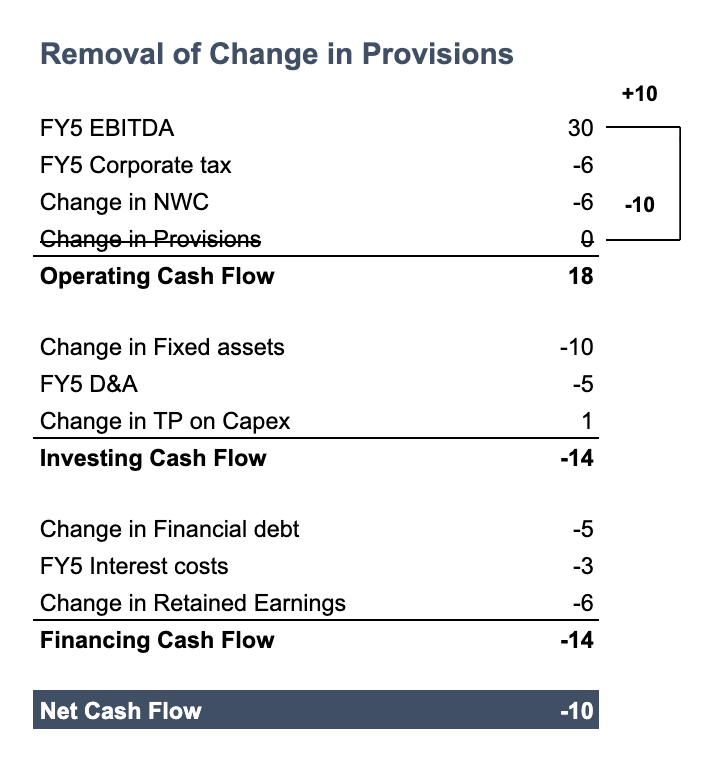

A common kind of non-cash item is provisions. Provisions impact today’s P&L in anticipation of a likely expense in the future. Based on that definition, it’s safe to say that such an item has not truly had any cash implication over the fiscal year, and it would make sense to remove it from our cash flow statement.

In the P&L example we’ve used so far, provisions were booked above EBITDA. If we want to remove the impact of a change in the provision, here’s how we could proceed:

However, the issue with this presentation is that we would like EBITDA for FY5 to reconcile to EBITDA as presented in the P&L. Instead, present the cash flow statement as follows:

I also recommend that you include a footnote explaining what the removed non-cash items were referring to. It may also be appropriate to showcase the “cash” EBITDA component of the business, which would comprise the following:

This demands some diligence, as it requires a correct match of all NWC accounts linked to EBITDA items. But it’s worthwhile. While this added complexity doesn’t offer a clearer view of the company’s cash-generative abilities, it will help your stakeholders understand the numbers better.

Applying the Rules

I hope that I’ve helped you understand how to prepare a cash flow statement more accurately, and why the interconnections between the P&L and balance sheet matter.

Real-life applications of this cash flow statement model may be slightly trickier due to the number of accounts in your trial balance, the complexity of accounting principles, and exceptional events like an M&A transaction. However, the underlying principles I’ve used in this cash flow statement model remain exactly the same. Following these guidelines will allow you to be proactive instead of reactive, and you won’t have to pour countless hours into a thankless balancing exercise once inconsistencies are found.

Further Reading on the Toptal Blog:

- Cash Flow Optimization: How Small and Medium Businesses Can Unlock Value and Manage Risk

- Advanced Financial Modeling Best Practices: Hacks for Intelligent, Error-free Modeling

- Forecast for Success: A Guide to Cash Management

- Financial Clarity at Last: How to Reboot Your Chart of Accounts Structure in 7 Steps

- Strategic Financial Leadership: 6 Skills CFOs Need Now

Understanding the basics

A cash flow statement is made up of three elements: cash flow from operations, such as accounts payable or receivable; cash flow from investing, which includes securities purchases, capital expenditures, and sales of equipment or property; and cash flow from financing, such as equity or debt repayment.

To prepare a cash flow statement from the balance sheet, start with the cash and cash equivalents at the start of your reporting period. Next, analyze changes in balance sheet accounts, such as accounts payable or receivable, to determine cash flow from operations. Then consider cash outflows and inflows from investing and financing activities. The result is the net cash flow from the reporting period.

Pierre-Alexandre Heurtebize

Nantes, France

Member since January 9, 2020

About the author

Pierre is a corporate finance, PE, and FP&A expert with extensive experience in complex financial modeling, translating entrepreneurs’ ideas into robust business plans, and leading in-depth financial due diligence. He has assisted with more than 60 transactions globally, mainly in the retail, SaaS, and technology spaces.

PREVIOUSLY AT