Forensic Accounting: Due Diligence’s Secret Weapon

More than just a way to investigate financial crimes, forensic accounting is the most in-depth form of due diligence and compliance. But smaller firms often overlook its value. Here’s why that’s risky.

More than just a way to investigate financial crimes, forensic accounting is the most in-depth form of due diligence and compliance. But smaller firms often overlook its value. Here’s why that’s risky.

Ryan Zanoni

Ryan is a Senior Editor at Toptal. He has more than 11 years of experience as a writer and editor covering business and technology.

Expertise

Featured Experts

The term “forensic accounting” may conjure up images of detectivelike professionals scouring files, conducting interviews, and running background checks to crack cases of financial crime. While that is part of the job, forensic accountants are also needed to investigate legitimate financial activity and perform due diligence reviews to evaluate potential investments, mergers, and acquisitions.

But while many organizations need to do due diligence regularly, it’s not that common for them to employ these specialized accountants to assist with the task, says management consultant Margaryta Pugachova, a member of the Toptal network since 2020. This is particularly true of small and midsize businesses. “They don’t place a high enough value on the practice, which is quite expensive, so they try to get by just having their in-house team handle it,” she explains. “But those internal teams largely lack the expertise, qualifications, and broad outlook to do this work properly. This leads to errors and poor investment decisions that are often more costly than the capital outlay for investigative due diligence.”

A forensic investigation can easily cost thousands of dollars, but due diligence plays a critical role in verifying how much a business is worth and whether its financial activities are in accordance with the law. Accounting experts perform this kind of investigation on businesses their clients are thinking of investing in, merging with, or acquiring, but will also conduct internal investigations for clients that want deeper insight into their own operations.

After an investment, merger, or acquisition, forensic accountants perform compliance reviews to verify whether all parties are honoring the terms of their agreements and abiding by regulations. The two processes involve similar—sometimes identical—actions, but compliance reviews are typically less structured than due diligence checks. And when neither reveals the financial truth, the consequences can be catastrophic.

How Does Forensic Accounting Work?

Forensic accounting differs significantly from general accounting. Whereas the latter is concerned with whether financial statements adhere to rules known as the Generally Accepted Accounting Principles (GAAP), the former examines whether the story being told by those financials makes sense and is likely to be true.

Professionals who specialize in this type of accounting don’t just examine financial statements: They take a holistic approach, incorporating statistical analysis, big data and machine learning, interviews, and physical observation to arrive at the truth—which is just as crucial for due diligence as it is for criminal cases.

Whether the investigation is for due diligence or compliance, a forensic accountant typically begins by studying the business’s balance sheet, income statement, and cash flow statement. They compare the numbers on these documents over time and against those of competitors, looking at the business’s self-reported valuation and ensuring it makes sense, checking transactions against counterparties’ records, and examining share ownership. The forensic accountant may also use tactics like validating and interviewing customers; talking to suppliers, industry peers, and the investor relations team; visiting offices and warehouses; and sometimes even reviewing camera surveillance footage to confirm the existence of production facilities and work activity, Pugachova says. They might use AI software to determine whether electronic documents have been altered or falsified and check databases to find out if executives have been investigated for fraud. All of this work is done to corroborate or refute the companies’ claims.

To evaluate these claims, forensic accountants typically have expertise in advanced valuation practices—particularly for high-tech, highly cyclical, and distressed assets, as well as other nontraditional assets like derivatives and those in emerging markets.

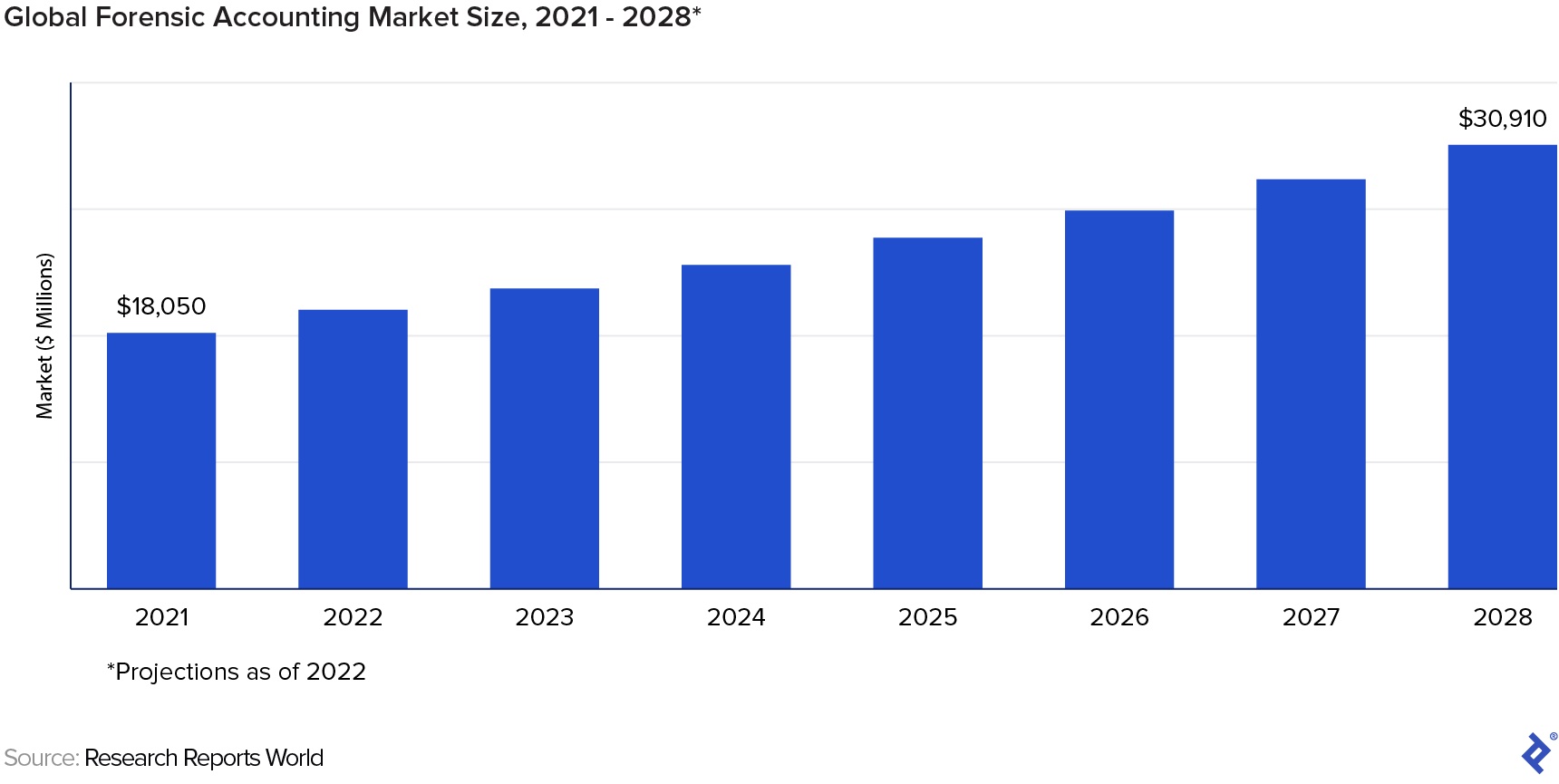

The forensic accounting field has been steadily growing, largely driven by the increased incidence of fraud and finance-related cyber crimes, such as ransomware attacks. However, forensic accounting is also more in demand because of stricter financial regulations, as well as the fact that most regulations predate alternative assets like crypto and haven’t been updated to address the related tax and reporting liabilities and business practices.

The main uses of forensic accounting for due diligence and compliance include revealing poor investments, uncovering hidden value, and identifying the right moment to sell or buy stock. Let’s take a close look at real cases of how the practice works for each of these purposes.

Revealing Poor Investments

Several years ago, management consultant Carlos Salas had a client who was considering investing in private mobile e-commerce brand Powa Technologies. In 2015, Powa said its business was worth $2.7 billion and that 1,200 companies had signed up to use its product. The client brought Salas and his team in to verify these and other claims, as well as to obtain an accurate overall view of the business’s financials.

“Our review of Powa encompassed fieldwork such as contacting suppliers, customers, and peers; visiting company headquarters; interviewing employees; and confirming international bank accounts,” says Salas, a member of the Toptal network since 2020. “We uncovered irregularities that included poor cost discipline, nonexistent clients, offshore shell firms generating fictitious revenue, and mischievous past behavior from the CEO.”

Salas and his team emailed more than 300 of the companies that had supposedly signed contracts to be Powa customers. About 20% replied and reported that they had not signed contracts. It was later revealed that the vast majority of the other businesses named also had no contracts with Powa.

Salas spotted another red flag when he found out Powa was operating out of lavish offices in major cities around the world. “As a startup, you cannot be paying such high amounts in rent when you haven’t broken even financially. When Google and Facebook started, they were in a basement,” he says. “That didn’t add up.” It looked like Powa was spending investors’ money on rent instead of growing the business.

By early 2016, Powa had gone bankrupt and collapsed. If Salas’s client had invested in the company, they would have lost as much as $25 million. “That’s why it’s very important to always run forensic accounting reviews, but especially when it comes to early-stage businesses in private equity,” Salas says. “If you don’t, and your clients end up investing in a fraud, they’ll lose everything.”

Uncovering Hidden Value

Averting disaster is probably the more compelling argument for investigative accounting, but the practice also plays a significant role in identifying diamonds in the rough. While income statements and balance sheets are integral to contextualizing reported revenue and asset pricing, a company may present them in ways that don’t reflect the company’s true value. Investigative accountants, however, have the skills to bring that to light.

For example, in 2019, Toptal management consultant Benjamin Ostrow was working as a senior associate for a family office, where he investigated new businesses that his firm was thinking of investing in or acquiring. Those companies’ financials, he discovered, sometimes obscured important information.

“Sometimes, because of the way people do bookkeeping, they end up underrepresenting their businesses. There was an industrial services company I was looking into for a current portfolio company that was interested in acquiring it. The target firm was expensing equipment purchases rather than capitalizing them,” Ostrow says. “I went into the field with the president of our operating company, and we found millions of dollars worth of hard assets just sitting around—not even on the firm’s balance sheets.”

The company was treating those purchases as an outlay, which was beneficial for short-term taxes. But to potential investors and buyers, it made the business appear to be less profitable, with fewer assets than it actually had. In reality, those “expenses” were capital expenditures that added substantial value.

“This discovery made the acquisition more attractive to us than it was at first glance,” says Ostrow. “Our work made us more comfortable with the deal and helped us complete the transaction more quickly and on favorable terms for the buyer.”

In other cases, a company’s financials might suggest that it’s engaged in fraud, but a deeper investigation reveals that it’s not. Back in 2012 and 2013, Ostrow was an investment analyst looking into Ubiquiti, a manufacturer of networking hardware, for his employer, a hedge fund. It had experienced a sudden deceleration in sales, a significant buildup in accounts receivables and inventories, and a big drop in stock price. The typical explanation in a case like this would be that the firm had been channel stuffing—inflating sales numbers by encouraging resellers to take on inventory without selling it to end users.

But Ostrow’s investigation revealed that the company was above board. “Through additional research, I was able to validate that a contract manufacturer they were using in China had completely copied what they were doing,” Ostrow says. “The problem wasn’t a lack of demand—there was an influx of counterfeit supply, and people couldn’t distinguish that from the authentic product.”

Ostrow was able to work out the real narrative in part by understanding the customer base. He went to industry conventions for wireless internet service providers and talked to more than 100 people. “I toured multiple networks. And I said, ‘The demand is here. Stuffing the channel implies there isn’t demand, so that’s not the issue.’” After that realization, he looked into the claims regarding counterfeit goods.

Uncovering the counterfeiting allowed Ostrow and his firm to make the decision to invest in the business, which made them millions of dollars—well worth the several months and several thousand dollars spent on forensic accounting research.

Identifying the Right Moment

Salas often uses his investigative accounting expertise in short-selling stock for clients. The practice is all about timing—if you don’t sell the stock and buy it back at the right times, you could lose out. A valuable way to get an edge is to perform extensive due diligence on the company you want to short in order to predict its stock performance.

In 2018, Salas looked into Wirecard, a German payments company. He first noted that the firm’s shares were overpriced and then discovered that its financials were not entirely legitimate. Wirecard’s stock became extremely volatile, presenting a tempting opportunity to short the stock. However, German regulators soon began an investigation and halted all short-selling for two months.

“If we had placed a short on that company at the very beginning of the investigation, we would’ve lost a lot of money because the stock was still rising. Wirecard was a tech darling favored by investors,” Salas says. “However, after the ban was lifted, evidence found by the regulators and authorities continued piling up against the company, and we could see that was a good time to short the stock, because its value was bound to fall soon. So, we borrowed and sold it at that point.” He was right: Wirecard’s stock price fell more than 80%—a plunge that began shortly before former CEO Markus Braun was arrested—resulting in a large profit for Salas’s client, who bought the stock back and returned it to the broker after the crash. Shortly thereafter, Wirecard became insolvent.

Salas’s forensic investigation couldn’t tell him when to short the stock, but it did help him identify the company as one to watch and be prepared to act when the time was right.

Using Investigative Accounting Judiciously

Because forensic accountants have specialized knowedge, even enterprise businesses with internal accounting teams can benefit from hiring them for high-stakes deals, Pugachova says. “These professionals also bring the context of operations from other companies, so they have a strong sense of the norms and can provide a broader, more holistic view of a business’s financials—increasing the chances of identifying issues that may have been missed in-house.”

She notes, however, that there are sometimes good reasons a company may not want to hire an investigative accountant. Forensic accounting is commonly associated with suspected wrongdoing, so it’s important to consider the potential effect on a business’s relationship with investees, fellow merger parties, or acquired partners. Given the expense and potential for reputational harm, she advises firms to have their finance teams consider the deals for which this detective work is necessary and discuss their options with a risk management specialist.

But the bottom line is that the benefits more often outweigh the risks, Pugachova says. “I haven’t come across any blunders made by organizations that dedicated the funds required to have this work done comprehensively by outside experts. But I do know of companies, including a private equity fund, that had to write off their whole business because they made bad investments as a result of neglecting to do full due diligence. Quality comes with the price.”

Further Reading on the Toptal Blog:

- Navigating the Nuances of Investment Due Diligence

- AI Investment Primer: A Practical Guide to Appraising Artificial Intelligence Dealflow (Part II)

- What Makes for a Successful Management Buyout Process?

- Raising Venture Capital in Down Markets: A Guide to Early-stage Funding

- Real Estate Financial Modeling: 3 Costly Mistakes to Avoid

Understanding the basics

Clients who are thinking of investing in, merging with, or acquiring a firm must conduct due diligence—the process of fact-checking that firm’s valuations, revenue, and activity. Forensic accounting is the most thorough approach to due diligence.

Investigative accounting, also called forensic accounting, is the in-depth examination of businesses’ finances using resources like financial statements; information from clients, peers, or suppliers; data from onsite observations or cameras; software that detects document falsification; and databases that reveal fraud investigations.

A management consultant for a firm performs a compliance review after an investment, merger, or acquisition to ensure that the counterparty is honoring the deal and abiding by laws. The work is similar to due diligence but less structured. Forensic accounting is the most in-depth form of compliance review.